$20.5 Million in Premiums. $0 in Equity. That's the Deal You're In.

A 50-doctor independent practice will pay $20.5 million in insurance premiums over 20 years and build nothing from it.

$20.5 million.

That’s the total insurance premiums a 50-doctor independent practice pays over 20 years. Every dollar leaves your balance sheet. None of it builds equity. None of it comes back.

A health system paying for the exact same coverage pays 25 to 40 percent less. Over 20 years, that gap costs your practice $4 million to $6.5 million in excess premiums alone.

No one told you. Now someone is.

IN TODAY’S ARTICLE:

The structural disadvantage: 25-40% more expensive insurance for the exact same coverage. Not because you’re bad at medicine. Because you’re small at purchasing.

How that gap costs a 50-doctor practice $4 million to $6.5 million in excess premiums over 20 years while building zero equity

Why PE acquisition and health system employment both close the gap by taking your independence

The third path exists. But first you need to understand the trap.

Glossary at the bottom of today’s article.

THE INSURANCE TAX ON INDEPENDENCE

Every month, you cut a check for employee benefits. Another check for health insurance. Another for workers’ compensation. Another for malpractice coverage.

That money doesn’t just buy coverage. It leaves your balance sheet permanently. Your practice builds no equity from it. No float. No investment returns. No retained value. The carrier collects your premiums, invests them, pays claims, and keeps the remainder.

The system isn’t broken.

It’s working exactly as designed.

You built your practice to stay independent. That decision was right. It was clinically right. It was financially right in every way except one: scale.

Health systems pay less for the exact same insurance. Not because they negotiate better. Not because they have better claims experience. Because they’re large. They aggregate risk. They have purchasing power.

Independent practices pay 25 to 40 percent more for identical coverage.

That’s not a pricing difference.

That’s a tax on independence.

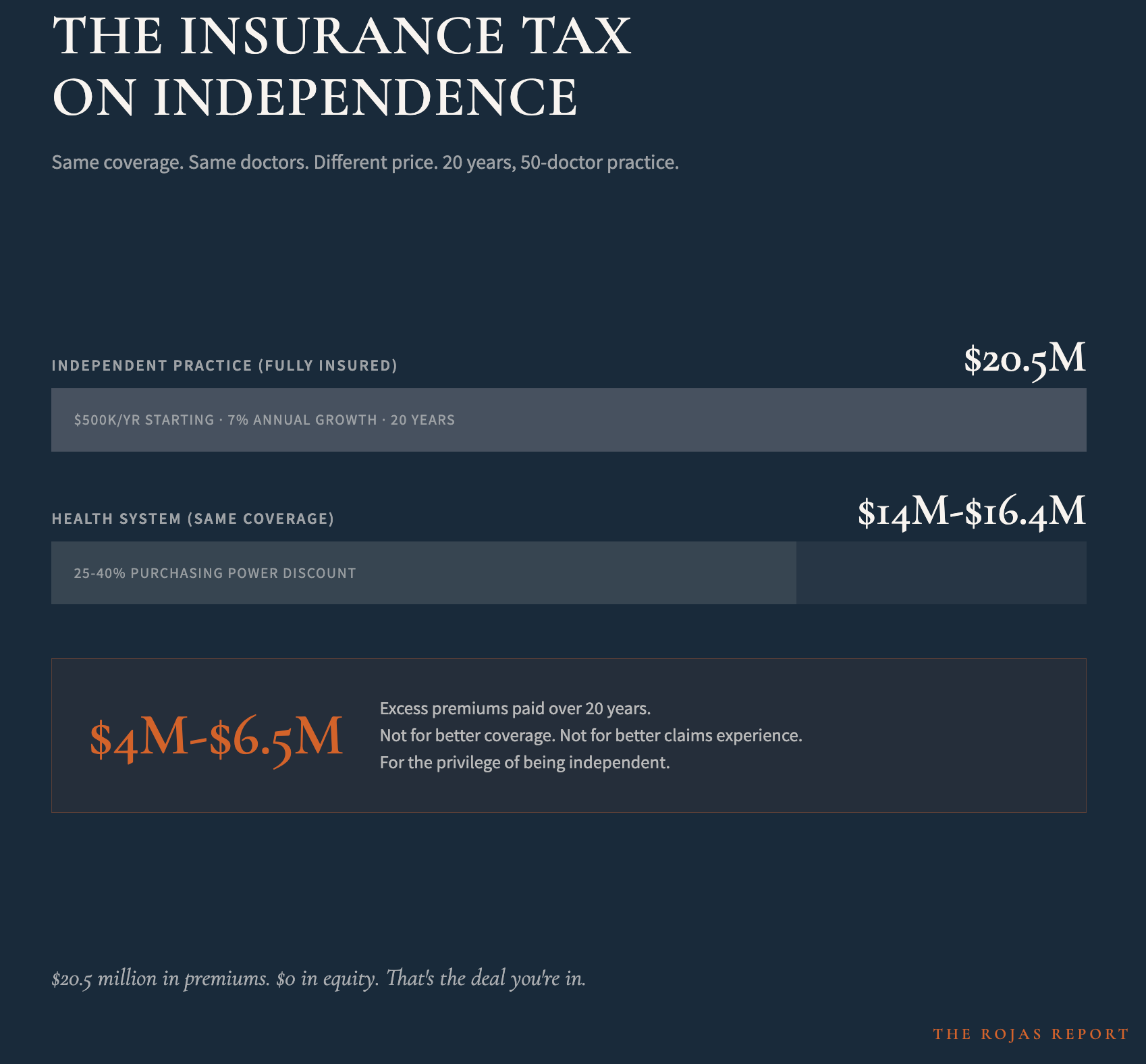

A 50-doctor practice paying $500,000 annually in fully-insured premiums will, with historical premium growth rates of 7-8% annually, pay approximately $20.5 million in total premiums over 20 years.

A health system insuring the same 50 doctors for the same coverage pays $14 million to $16.4 million over the same period, depending on the size of the purchasing power gap.

The difference: $4 million to $6.5 million.

Gone. Paid in excess premiums for the privilege of being independent.

And the worst part: this number never appears in your financial statements.

There’s no line item for “independence penalty.”

There’s no invoice that says “you overpaid by $250,000 this year compared to the hospital across town.” The cartel counts on complexity to hide in plain sight.

But it’s not the price of autonomy.

It’s a structural choice.

And choices can be different.

You’re overpaying for insurance by $4 million to $6.5 million over your career.

And no one told you until now. 60,000+ physicians stopped accepting that.

Subscribe now.

WHY PRIVATE EQUITY DOESN’T FIX THE PROBLEM

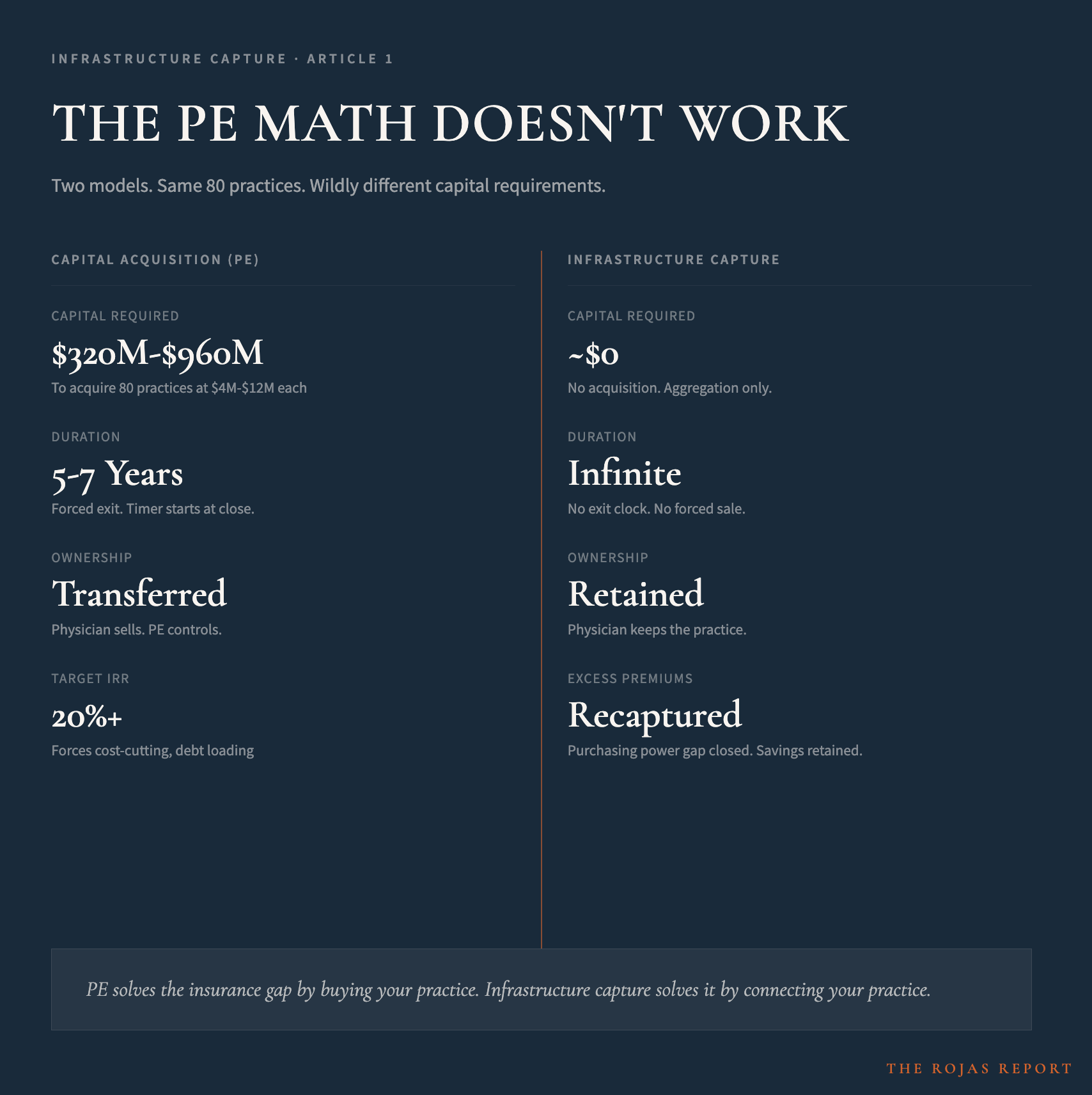

Private equity looked at this exact problem and understood it perfectly. PE saw fragmented independent practices paying too much for insurance. PE deployed over $1 trillion into healthcare acquisitions since 2000 with a simple solution: buy the practices, consolidate, negotiate better rates, extract a margin over 5 years, then sell.

The model works. PE-acquired practices do see insurance costs decrease. Purchasing power does increase.

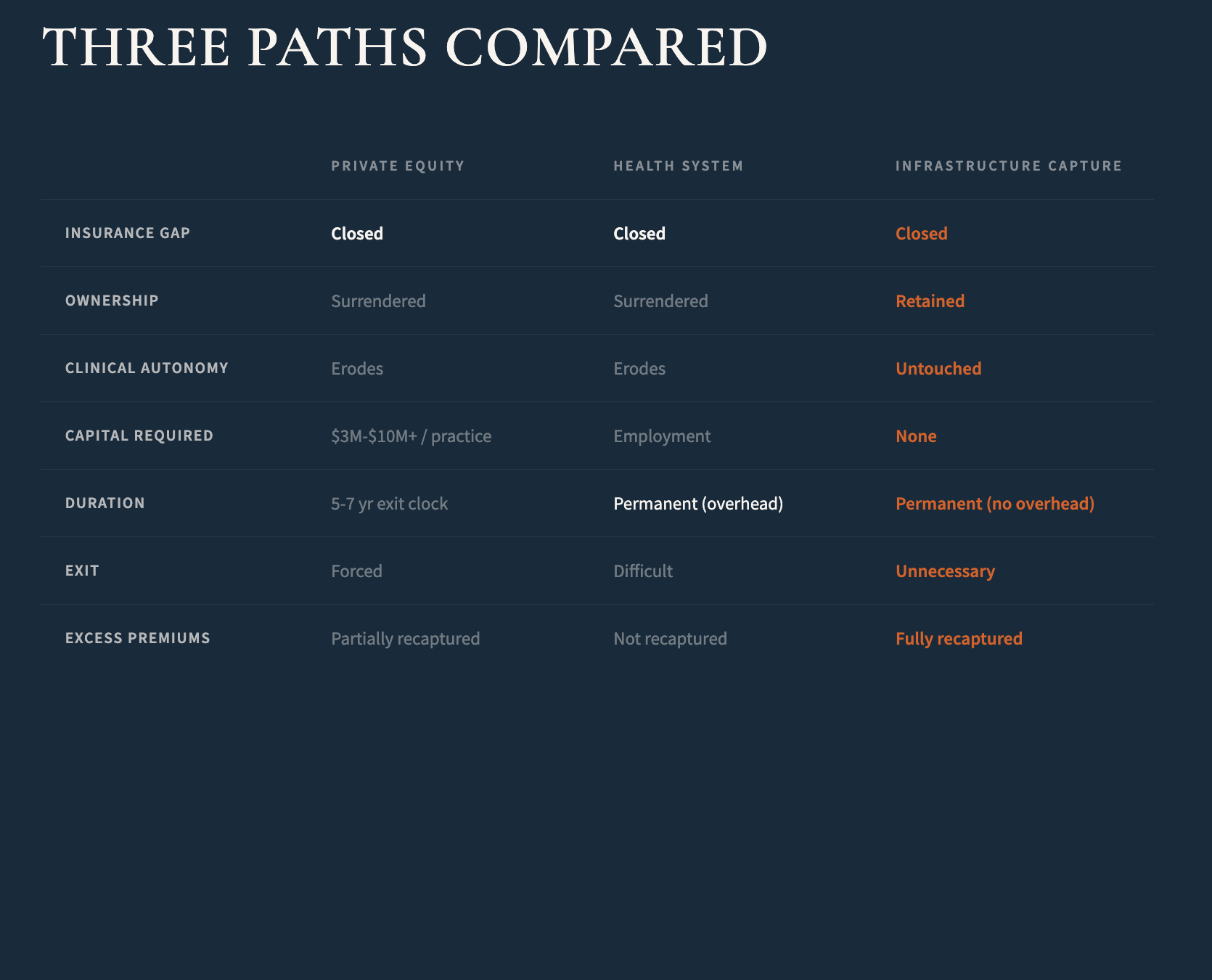

But PE solves the problem by requiring you to do the same: sell your practice.

THE DURATION PROBLEM

PE funds need to return capital and generate an IRR of 20%+ within 5-7 years.

Every dollar deployed carries a timer.

That timer forces behavior: cost-cutting, debt loading, margin extraction, and staff reduction. The actions that make PE’s timeline work destroy your practice’s long-term value.

PE solves the insurance problem by destroying the thing you fought to keep: independence.

You built independence to protect clinical autonomy. PE solves the economic problem by eliminating autonomy. They’re not solving the same problem you’re trying to solve. They’re trading one problem for another.

PE proved consolidation closes the gap.

But PE requires you to sell.

Health systems proved that scale works.

But health systems require you to surrender autonomy.

There’s a third option.

100,000 healthcare professionals are already reading it.

Subscribe

WHY HEALTH SYSTEM EMPLOYMENT DOESN’T FIX THE PROBLEM EITHER

Health systems avoid the duration problem by keeping assets permanently. They achieve the same purchasing power as PE. But they replace the clock with something else: organizational complexity.

A large health system requires a corporate apparatus. Legal. Compliance. Finance. Strategic planning. Governance. Committees. All of this overhead consumes much of the purchasing power benefit you’d expect.

Worse, employment erodes the thing you protected by staying independent: clinical autonomy. You become an employee. Decision-making centralizes. Compensation decisions are made by administrators. The practice of medicine changes. Your ability to run your practice independently disappears.

Health systems solve the insurance problem by eliminating the independence that made it worthwhile in the first place.

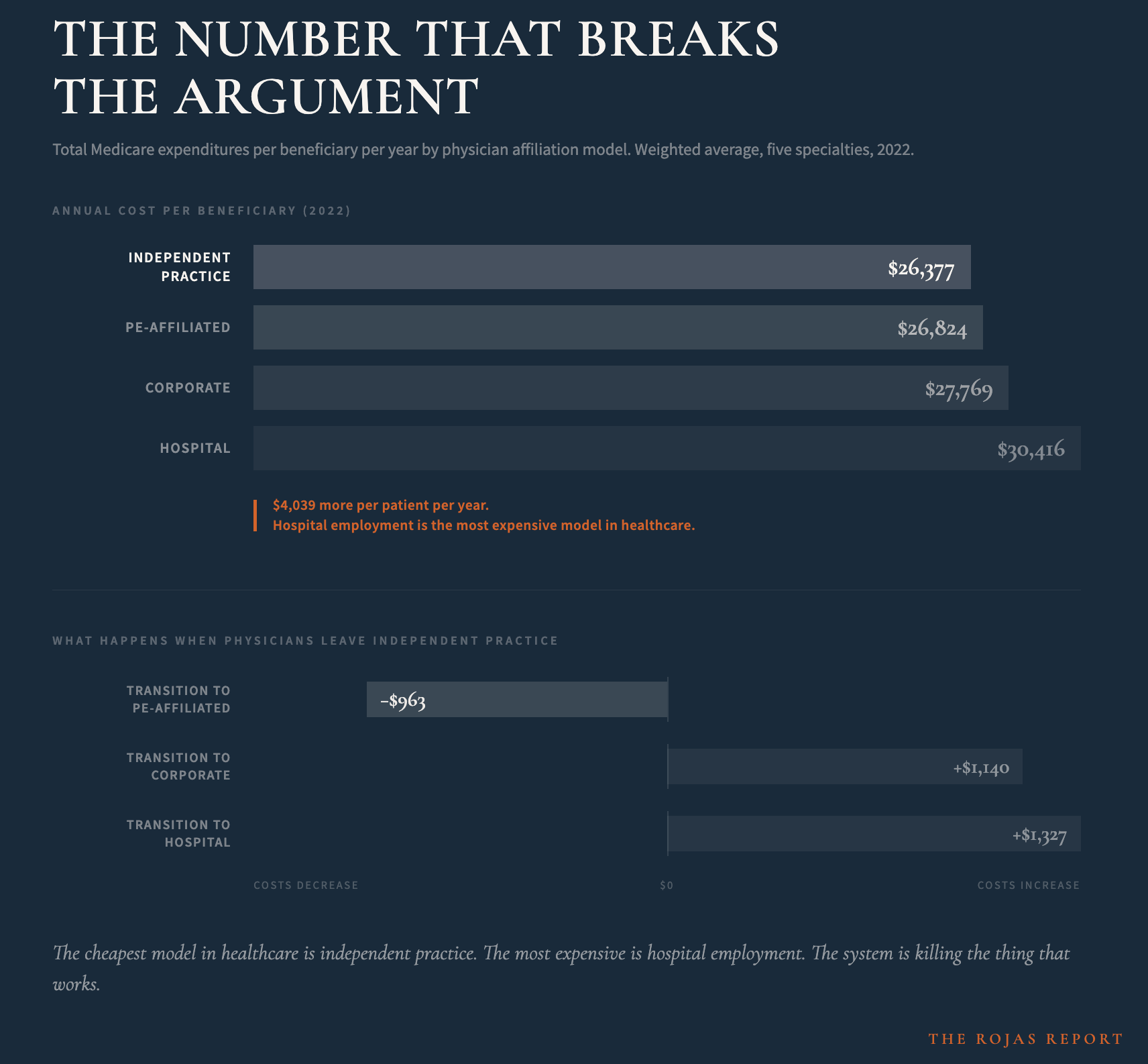

THE NUMBER THAT BREAKS THE ARGUMENT

Let’s skip the sugarcoating:

Avalere’s 2024 analysis of Medicare claims data tells you everything you need to know about which model actually delivers.

Independent private practice is the cheapest model in healthcare.

Across five specialties, beneficiaries attributed to independent physicians had the lowest total Medicare expenditures: $26,377 per beneficiary per year. PE-affiliated practices came in at $26,824. Corporate at $27,769. Hospital-affiliated physicians were the most expensive at $30,416 per beneficiary per year.

That’s a $4,039 difference per patient per year between independent practice and hospital employment. The model they’re telling you is unsustainable delivers the best cost outcomes in the system.

It gets worse for them.

When physicians transitioned from independent practice to PE affiliation, total Medicare expenditures decreased by a weighted average of $963 per beneficiary per year. When physicians transitioned to hospital employment, expenditures increased by $1,327 per year. Corporate affiliation increased expenditures by $1,140 per year.

Read that again.

The cheapest model in healthcare is independent practice. The most expensive is hospital employment. And every time an independent physician gets absorbed into a health system, costs go up. Every time.

This is the data the health systems don’t want in the same sentence as their recruitment pitch.

They’re not saving healthcare.

They’re making it more expensive.

And they’re doing it with your labor.

PE delivers better cost outcomes than hospital employment.

But PE requires you to sell. Hospital employment requires you to surrender. And independent practice, the model that already delivers the best economics, is being starved of the infrastructure it needs to survive.

Neither PE nor hospital employment solves your actual problem.

They solve the symptom by creating a different disease.

WHAT COMES NEXT

You now understand the structural disadvantage.

You understand why PE doesn’t fix it.

You understand why health system employment doesn’t fix it.

What you don’t yet understand is how to close the purchasing power gap without surrendering ownership, without taking on debt, and without surrendering clinical autonomy.

There is a model that does exactly that.

It’s not theoretical.

It’s operational in practices across the country right now.

But it requires understanding a completely different approach to consolidation.

One where infrastructure replaces capital, where aggregation replaces acquisition, and where you retain ownership while capturing hospital-system economics.

No one is coming to save independent medicine.

So we’re saving each other.

That framework is what we explore in Article 2.

-Rojas out.

GLOSSARY

Purchasing Power Gap: The difference in negotiating leverage between a single independent practice and a large aggregated group. Independent practices lack scale. Health systems have it. That gap drives the 25-40% premium difference.

Insurance Tax: The excess premium independent practices pay compared to health systems for identical coverage. Typically 25-40% higher due to subscale purchasing power. Over 20 years, this totals $4 million to $6.5 million for a 50-doctor practice.

Fully-Insured: An insurance model where a practice pays a carrier a fixed premium and the carrier bears all claims risk and retains all investment returns. This is the traditional model most independent practices use.

Captive Insurance: An insurance company formed by a group of practices to insure the group’s own risks. Instead of paying premiums to a commercial carrier, participants fund their own insurance vehicle and retain underwriting profits internally.

Float: The premium dollars that sit on an insurance company’s balance sheet between collection and claims payment. These dollars generate investment returns for the carrier. In traditional insurance, the carrier captures all float returns. In a captive, float returns go to the participating practices.

Self-Funding: An insurance model where a practice (or group of practices) pays claims directly from reserves rather than buying traditional insurance from a carrier. Requires captive insurance structure to be viable at scale.

SOURCES

Avalere Health. (2024). “Medicare Service Use and Expenditures Across Physician Practice Affiliation Models.” Physicians Advocacy Institute.

KFF. (2025). Health Insurance Premium Trends.

Bain & Company. Global Healthcare Private Equity Report.