$8.7 Billion in Revenue. Zero in Property Taxes. Negative $92 Million in Charity. Meet Michigan Medicine.

Let’s go inside the academic medical center that issued $2.1 billion in tax-free bonds, captured a slice of $1.1 billion in hidden Medicaid subsidies, and ran a $92 million deficit on the bargain, an arrangement that sets the stage for Michigan Medicine’s role in today’s discussion.

Your premium just went up.

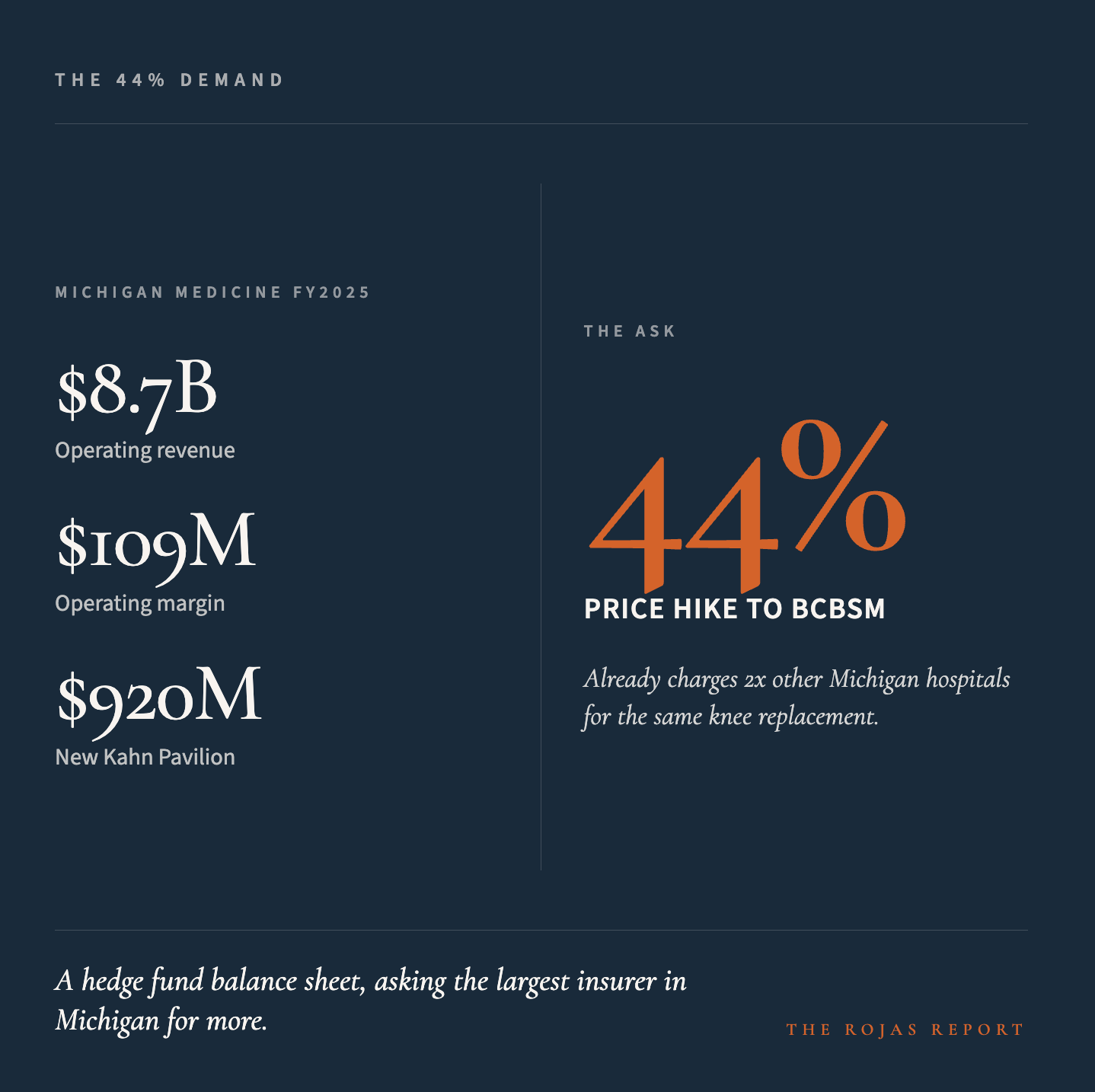

Michigan Medicine just asked for a 44% raise.

Same week.

In today’s piece:

Why the most prestigious hospital in Michigan is also the most expensive

The 44% price demand exposed the cartel posture behind the institutional brand.

Why federal reductions to projected DSH growth are changing how Michigan Medicine negotiates with commercial insurers

What the receipts actually say about who Michigan Medicine serves

Glossary at the bottom of today’s article.

THE DEMAND

Michigan Medicine and Blue Cross Blue Shield of Michigan have a contract that expires June 30, 2026.

According to BCBSM, Michigan Medicine is demanding a 44% price hike over the term of a new contract. Michigan Medicine disputes this framing, stating that BCBSM initially proposed a 30% reduction in reimbursement. In response, Michigan Medicine says it has offered either single-digit annual increases or a contract extension tied to quality outcomes. Both sides publicly disagree on the core terms and claims.

The two sides are public and dueling, and 300,000 commercial BCBSM members across Michigan are caught in the middle. If the deadline passes without a deal, University Hospital, C.S. Mott Children’s Hospital, Von Voigtlander Women’s Hospital, the Frankel Cardiovascular Center, and the new Kahn Pavilion all go out-of-network on July 1.

Strip the spin off both press releases and look at the underlying setup.

Michigan Medicine is already the highest-paid health system in Michigan. BCBSM has stated publicly that Michigan Medicine charges roughly twice as much as other Michigan hospitals for procedures such as knee replacements. Same surgery. Same implant. Same recovery. Twice the price, because of the name on the building.

This is not a hospital fighting to keep the lights on. Michigan Medicine generated $8.7 billion in operating revenue in fiscal year 2025 and posted a $109 million operating margin while it was at it. The $920 million D. Dan and Betty Kahn Health Care Pavilion was scheduled to open in late 2025. The university’s total assets sit at $37.1 billion. Net position: $24.9 billion.

This all adds up to a system with a hedge fund balance sheet, now entrenched in a public negotiation with Michigan’s largest insurer. Every disagreement over dollars here inevitably influences employer premiums and employee paychecks statewide, tying hospital finances directly to public cost.

Michigan Medicine’s defense is that Michigan hospitals are reimbursed at the third-lowest rates in the country. That is true on average. It is also irrelevant when applied to the highest-paid system in the state, asking to be paid more.

A contract will be signed by June 30 that determines what every Michigan employer pays for health insurance next year.

You will not read it.

The Rojas Report will.

Support out work.

THE 209-YEAR LOOPHOLE

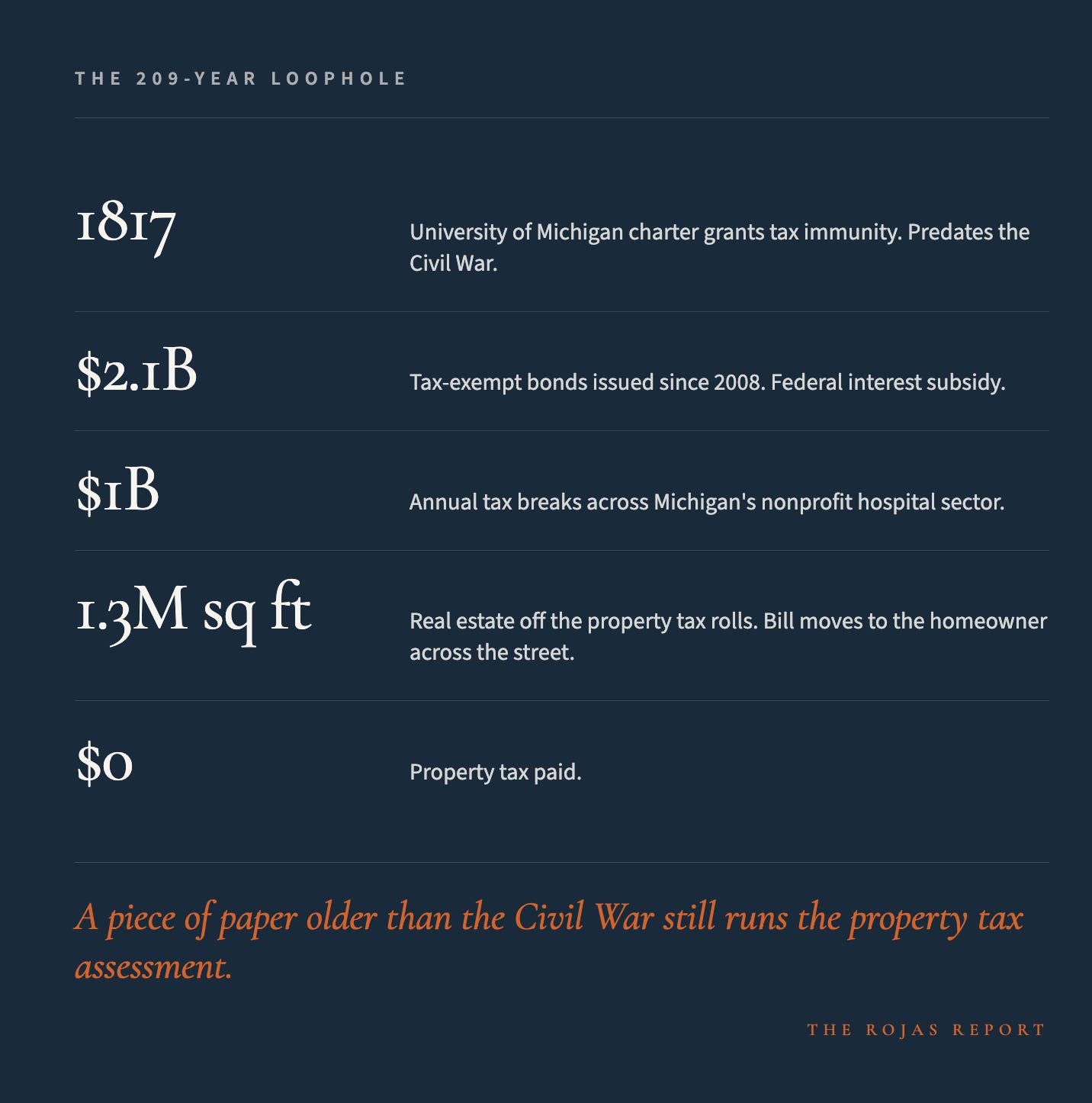

The University of Michigan was chartered in 1817. The charter granted the institution tax immunity. Every dollar that flows through the university and its hospital is protected by that immunity, shielded by a piece of paper older than the Civil War.

That immunity covers federal income tax. State income tax. Local property tax.

Every building Michigan Medicine operates out of, every parcel of land it leases or owns, every dollar of investment income that compounds inside its endowment, sits outside the tax base.

Michigan’s nonprofit hospital sector receives an estimated $1 billion in tax breaks annually. The average hospital exemption is $9.5 million. Michigan Medicine is the largest academic system in the state. The math from there is not subtle.

The real estate footprint magnifies this story. Michigan Medicine leases approximately 1.3 million square feet across roughly 60 locations and 120 leases. Yet this figure excludes university-owned buildings, which are also exempt from property taxes. Each parcel excluded from the tax base shifts the burden onto Ann Arbor homeowners, who cover the gap so the hospital pays none, another result of tax immunity.

Then there are the bonds.

Since 2008, the University of Michigan has issued more than $2.1 billion in tax-exempt bonds, much of it to finance health system expansion. Tax-exempt bonds carry interest rates significantly below what private companies pay. The interest savings are an additional federal subsidy, paid for by the Treasury, in service of an institution that already pays no taxes.

This is the architecture: a 209-year-old charter, a $1 billion sector-wide exemption, $2.1 billion in subsidized debt, and a real estate portfolio that passes its tax burden to Ann Arbor residents. Together, Such elements underpin Michigan Medicine’s financial structure.

The University of Michigan is not a hospital that is tax-exempt. It is a tax-exempt hospital.

THE CEO’s LILLY PROBLEM

In February 2026, The Michigan Daily published an investigation into former Michigan Medicine CEO Marschall Runge.

The reporting found that Runge failed to disclose his financial relationship with Eli Lilly in more than half of the research articles he authored while leading the system. Over his time on the Lilly board, he received more than $2 million from the company.

His base CEO compensation in 2023 was $1.64 million.

Stack the numbers. At Michigan Medicine, the CEO oversaw research priorities, formulary decisions, residency training, and clinical trial access, while simultaneously sitting on the board of a major pharmaceutical company. He collected checks and failed to disclose them in half of his papers—highlighting how leadership and financial incentives can intersect at the highest levels of academic medicine.

David C. Miller took over as CEO in July 2025. Whatever the new posture under Miller, the institutional question is the same. How did the disclosure gap survive that long, in that role, without internal compliance catching it?