A Drug Gets Discounted. The Patient Pays Full Price. Here’s Who Pockets the Difference.

The contract pharmacy is not a pharmacy. It’s a toll booth.

A federal program forces drugmakers to sell insulin to a clinic at a discount.

The clinic sends a patient to a Walgreens.

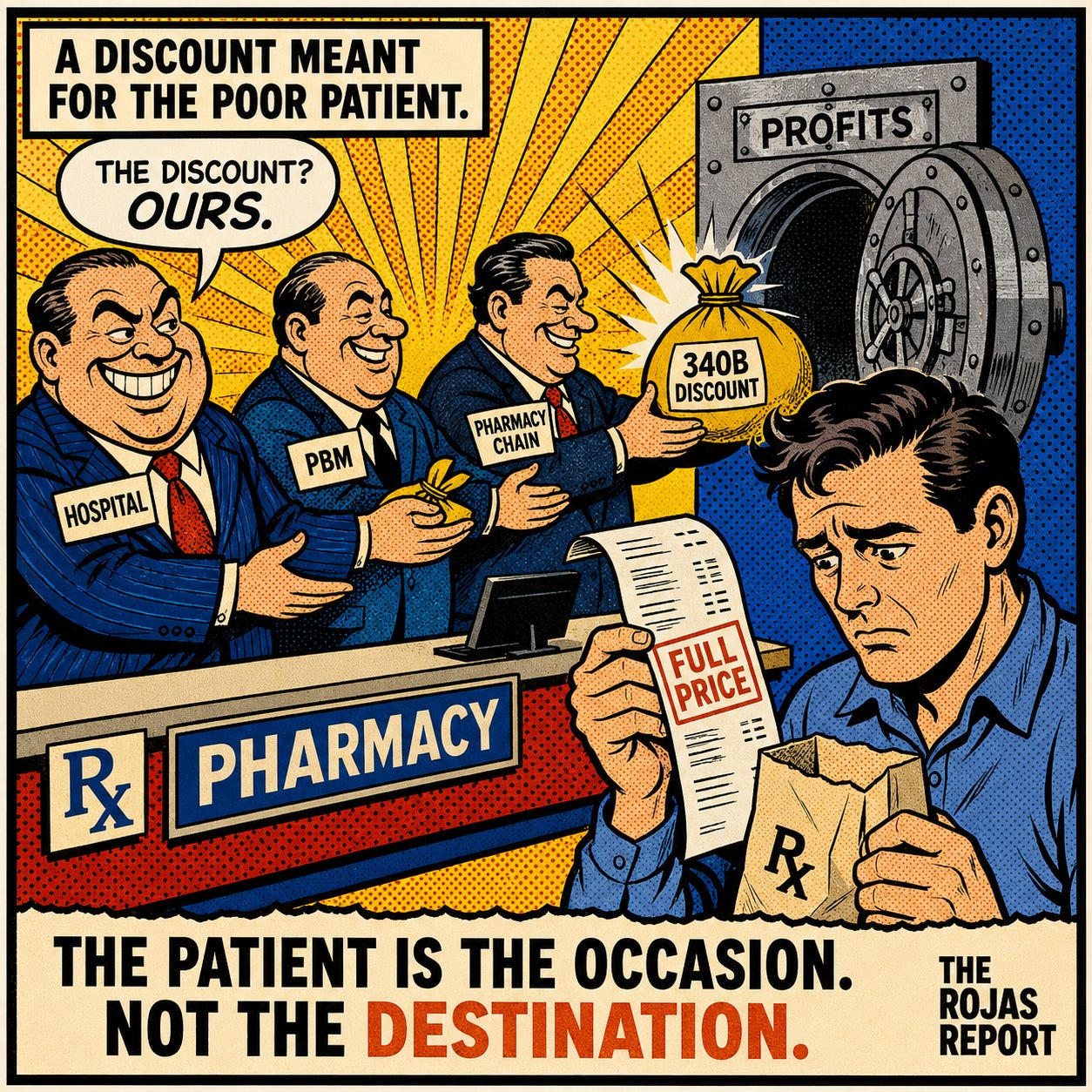

The patient pays the full retail price.The discount is split among the hospital, the PBM, and the pharmacy chain.

The patient gets nothing. Illinois calls this “patient access.”

IN TODAY’S ARTICLE:

How a discount meant for a poor patient becomes revenue for a billion-dollar system

Why the “contract pharmacy” is a billing arrangement, not a building

What Illinois SB2385 actually locks in, and who wrote it

The one distinction the bill refuses to make, and why that refusal is the whole game

Glossary at the bottom of today’s article.

THE DISCOUNT THAT NEVER ARRIVES

Congress built 340B in 1992 to do one thing. Force drug manufacturers to sell outpatient drugs at a steep discount to the clinics and hospitals that treat the poor. The theory was simple. The safety net buys low, treats the uninsured, and spreads funds to care for people who cannot pay.

That is not what happens anymore.

Today, a covered entity buys the drug at the 340B price.

It does not dispense the drug itself.

It routes the prescription through a “contract pharmacy,” a retail chain it pays to fill the script.

The patient walks into that pharmacy and pays their normal price.

Cash.

Copay.

Commercial insurance.

Full freight.

The discount does not move to the patient. It moves to the entity, the contract pharmacy, and the middleman who administers the arrangement. The patient is the occasion for the discount. The patient is not the destination.

A CONTRACT PHARMACY IS NOT A PHARMACY

Start with the language, because the language is doing work.

A “contract pharmacy” is not a special building for poor patients. It is a billing relationship. A CVS, a Walgreens, an Express Scripts mail operation, signs a contract with a covered entity to dispense 340B drugs on its behalf. The chain takes a dispensing fee. A third-party administrator, often owned by a PBM, sits in the middle and takes a cut for matching eligible prescriptions to 340B inventory.

In 2010, HRSA guidance opened the door for covered entities to use an unlimited number of contract pharmacies. The result was not more care for the poor. It was a land rush.

Contract pharmacy arrangements exploded into the tens of thousands. And the growth did not chase the patients the program names. An Avalere analysis found that 340B contract pharmacies are located in less diverse, higher-income ZIP codes than the hospitals that own them.

A separate study in the American Journal of Managed Care found that the pharmacy ZIP codes had incomes 25 to 30 percent higher than those of the entities they served. The poor patient was still the legal key that unlocked the discount. The poor patient was rarely the one who benefited from it.

Everyone in healthcare has a take on 340B.

Almost no one can show you where the dollar actually lands.

The Rojas Report, lead by accountants, follows the dollar.

That is the entire difference.Subscribe to learn.

THE TWENTY-SEVEN-FOLD TELL

Here is the number that ends the debate about intent.

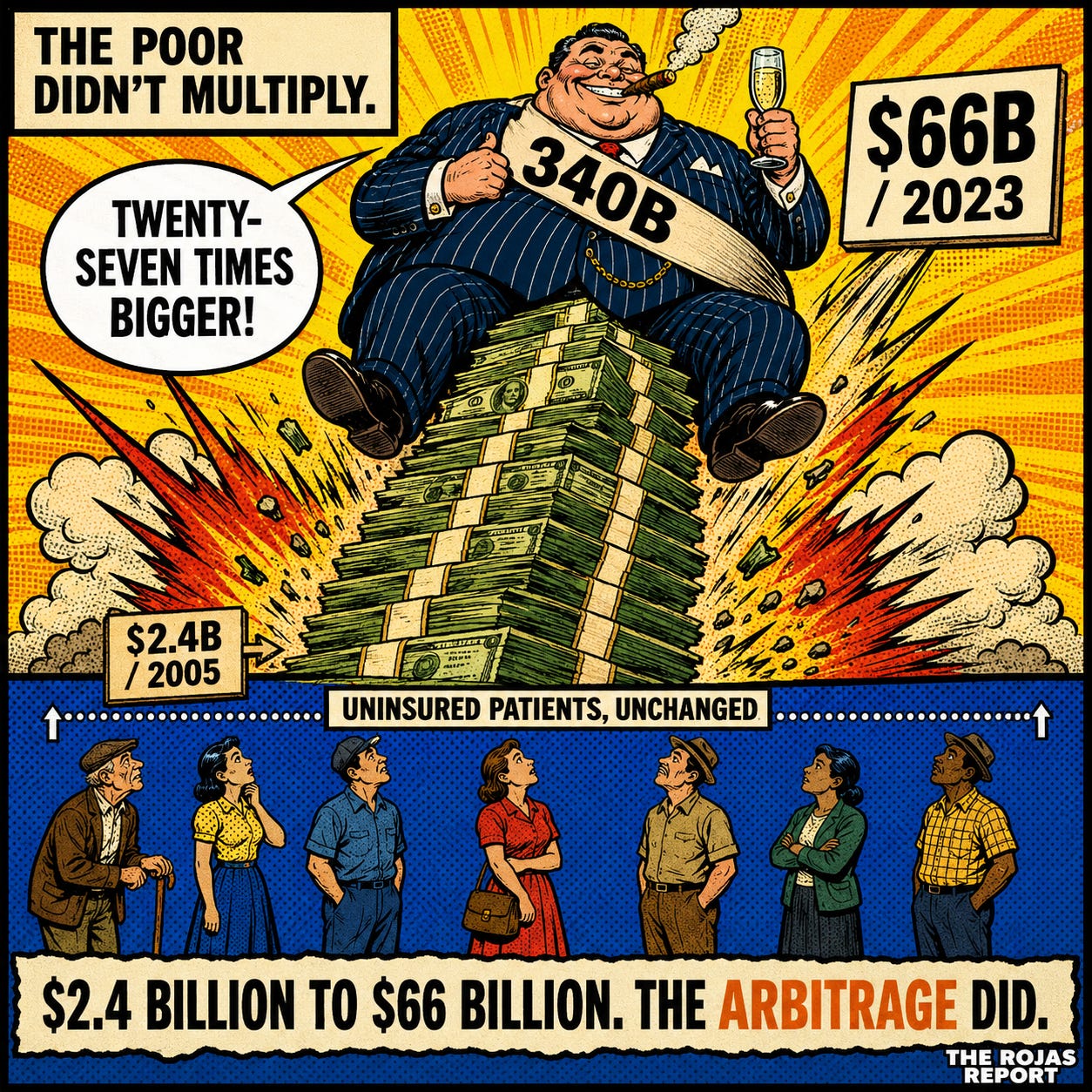

340B discounts ran roughly $66 billion in 2023. In 2005 they ran $2.4 billion. That is not growth. That is a twenty-seven-fold expansion in under two decades. At list price, the same purchases now total $124 billion, but the discounted figure is the money that actually changed hands, and it is the honest one to track.

The population of poor and uninsured Americans did not multiply twenty-seven times. The number of safety-net patients did not multiply twenty-seven times. What multiplied was the discovery, by hospital systems and the middlemen who serve them, that 340B is a margin engine wearing a charity costume.

Manufacturers put the markup at extreme multiples. PhRMA, citing an analysis by The Moran Company, claims hospitals collect an average of roughly 500 percent over their 340B acquisition cost on top drugs.

That attribution matters. It is the line between journalism and a press release. The figure may be directionally right. It is still their number, and their number carries their motive.

THE TWO ILLINOIS BILLS

Springfield has two 340B bills on the table. Read together, they tell the truth that neither tells alone.

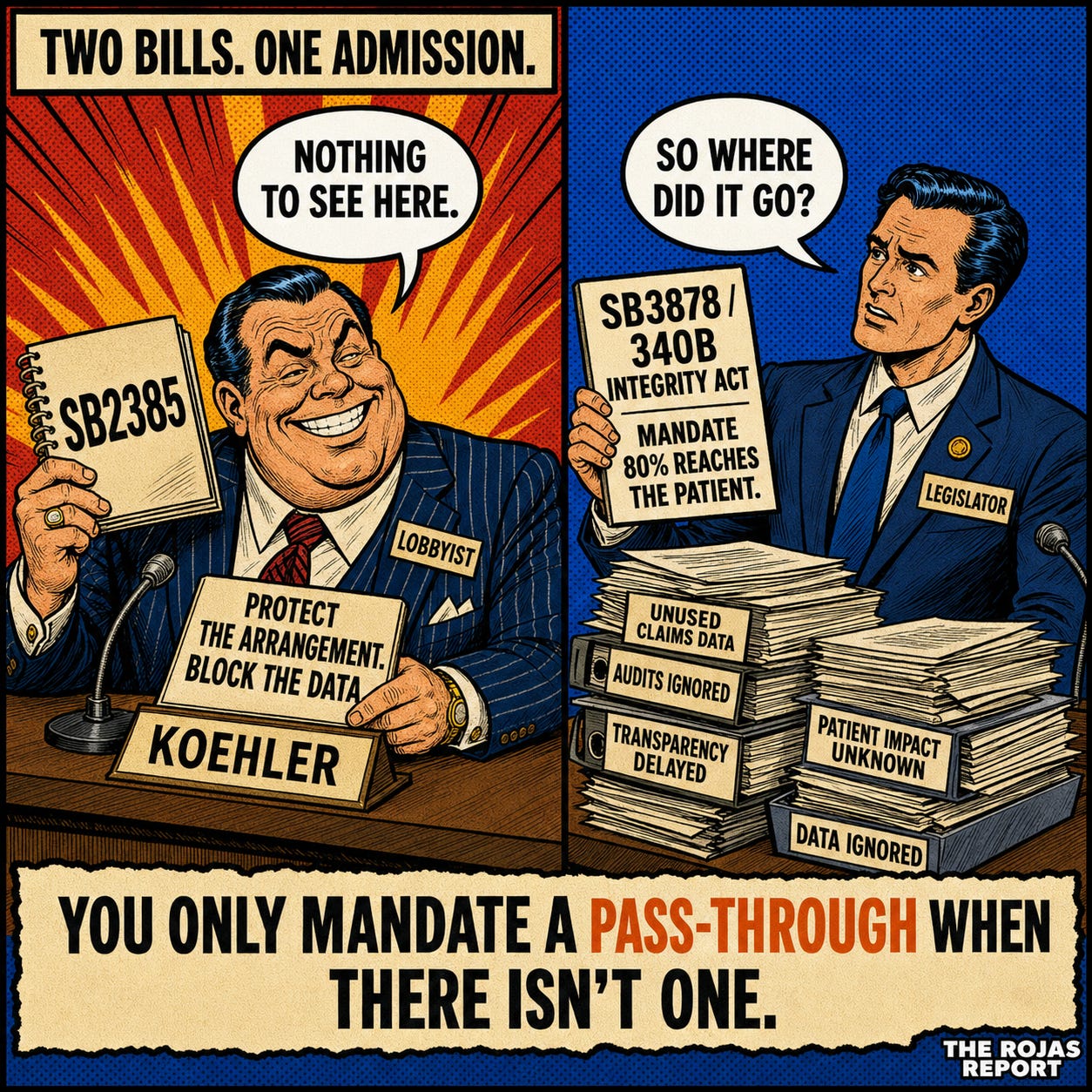

The first is SB2385, with a House companion in HB3350. Sponsor: State Senator David Koehler. Its name is the “Patient Access to Pharmacy Protection Act.” It bars manufacturers from restricting 340B deliveries to contract pharmacies and from demanding pricing or claims data from covered entities and their contract pharmacies.

Strip the title. The bill does not lower a single patient’s copay. It does not require a single dollar of the discount to reach a single patient. PhRMA’s own witness, Jessica Lynch, told the House Executive Committee the quiet part. “This is not an access bill,” she said. On that narrow point, the drug lobby is correct, which is its own kind of warning about how confused this fight has become.

The bill protects the arrangement. It keeps the spread flowing and forbids anyone from looking at the data that would show where it lands.

Then there is the second bill, SB3878, the 340B Integrity Act, and this is the one that tells the truth by accident. State Senator Julie Morrison introduced it in February 2026.

SB3878 would force covered entities, beginning July 2026, to use 80 percent of the prior year’s 340B profits to lower what low-income patients actually pay at the counter. It would bar Medicaid from billing for 340B drugs starting in 2027. It would order a report on what 340B is doing to the Illinois state employee health plan.

Sit with the first provision.

You cannot mandate that 80 percent of the profit be returned to the patient unless you already know it does not. SB3878 is a confession in legislative form. The savings are not reaching the patient. Springfield knows it. One bill protects the gap. The other tries to close it.

THE DISTINCTION THE BILL REFUSES TO MAKE

This is where most coverage stops, and where the real story starts.

Not every covered entity is running an arbitrage. A federally qualified health center in rural Illinois with no pharmacy of its own is not a billion-dollar system. It genuinely relies on a contract pharmacy to get drugs into a patient’s hands, because building a dispensary it cannot staff is not an option. For that clinic, contract pharmacy access is survival, and the savings often do fund care for people who cannot pay.

The billion-dollar disproportionate-share hospital system running thousands of contract pharmacy arrangements across affluent suburbs is a different animal entirely. Same statute. Same word. Opposite reality.

SB2385 protects both. Identically.

It writes one rule for the rural FQHC and the multi-state system and refuses to tell them apart. That refusal is not an oversight. It is the design.The large systems and their middlemen need the small clinic as a human shield, because “we are protecting rural safety-net clinics” is a far better headline than “we are protecting our margin.”

A physician sees the cost of this every day and never sees the cause. The independent practice down the road cannot run a 340B arbitrage. It buys drugs at real prices, competes against a hospital outpatient department buying the same drug at a fraction, and loses.

The discount that was sold to Congress as care for the poor has become a weapon against independent medicine. That is the part no one in Springfield is paid to say.

THE FIGHT IS NOT ABOUT ILLINOIS

Roughly twenty states have passed or are weighing contract pharmacy protection laws. Arkansas went first, and its law survived federal challenge in the Eighth Circuit. Manufacturers won the opposite ruling in the Third and DC Circuits on the federal question. The Seventh Circuit, which covers Illinois, has not ruled. That is why Illinois is contested ground, not settled.

The legal terrain is shifting beneath it all. In August 2025, the Second Circuit revived an antitrust case against insulin manufacturers, holding that coordinated contract pharmacy restrictions constituted a restraint of trade. HRSA issued guidance in the same month on a rebate model that would route 340B savings as a back-end payment rather than an upfront discount. Drugmakers want that model because it lets them see the claims data. Covered entities fight it because the data is exactly what they do not want seen.

Everyone in this fight is protecting a flow of money and calling it a principle. The drug manufacturer, protecting its revenue, calls it ‘program integrity’. The hospital system protecting its spread calls it patient access. Both want you watching the other one.

The patient, the one the program was built for, is not in the room. Neither is the independent physician. They are the line items everyone else is fighting to keep.

-Rojas out.

GLOSSARY

340B: A federal program from 1992 that forces drug manufacturers to sell outpatient drugs at a discount to clinics and hospitals that serve low-income patients.

Covered entity: A clinic, health center, or hospital eligible to buy drugs at the 340B discount. Ranges from a tiny rural FQHC to a multi-billion-dollar hospital system.

Contract pharmacy: A retail or mail pharmacy that signs an agreement to dispense 340B drugs for a covered entity. A billing relationship, not a special facility.

The spread: The gap between the discounted 340B price a covered entity pays and the full price collected when the drug is dispensed. The money in dispute.

PBM (pharmacy benefit manager): A middleman that administers drug benefits. Often owns or is tied to the third-party administrators that run 340B contract pharmacy programs and take a cut of the spread.

DSH hospital: A disproportionate-share hospital, one treating a large share of low-income patients. The eligibility door through which the largest systems entered 340B.

FQHC: A federally qualified health center. Community clinics serving low-income populations, often genuinely dependent on contract pharmacies because they have no dispensary of their own.

Rebate model: A proposed change where the 340B discount is paid back to the entity after the sale instead of taken off the price upfront. Manufacturers want it because it exposes claims data.

SOURCES

[1] HRSA, “2023 340B Covered Entity Purchases” (Oct 1, 2024). $66.3B in discounted purchases.

[2] National Alliance of Healthcare Purchaser Coalitions, “340B By the Numbers”. 2005 baseline.

[3] MedPAC, “Overview of the 340B Drug Pricing Program” (May 2015).

[4] IQVIA, “The 340B Drug Discount Program Grew to $124B in 2023” (2024). List-price value only, never paired against the 2005 discounted figure.

[5] PhRMA / The Moran Company, “New Analysis Shows Hospitals Mark Up Medicine Prices 500%” (Aug 2, 2023). Contested industry estimate, attributed as such.

[6] Avalere, “340B Hospital Child Sites and Contract Pharmacy Demographics” (Apr 18, 2022).

[10] Illinois SB3878, “340B Integrity Act,” Sen. Julie Morrison (introduced Feb 6, 2026).

[11] PhRMA v. McClain, 95 F.4th 1136 (8th Cir, Mar 12, 2024). Arkansas law upheld.

[12] Sanofi Aventis U.S. LLC v. HHS (3rd Cir, Jan 30, 2023). Manufacturer-favorable.

[13] Novartis Pharmaceuticals Corp. v. Johnson (DC Cir, May 21, 2024). Manufacturer-favorable.

[14] Mosaic Health, Inc. v. Sanofi-Aventis U.S., LLC (2nd Cir, No. 24-598, Aug 6, 2025). Revived under Sherman Act Section 1.

[15] HRSA 340B Rebate Model Pilot Program, 90 Fed. Reg. 36,163 (Aug 1, 2025).

[16] 340B Report, “2025 in Review: 13 States Enacted 340B Contract Pharmacy Access Laws” (Dec 18, 2025). Over 20 states total.