Abridge. Innovaccer. KeyCare. Three Startups. Health Systems on Every Cap Table. Zero Tools for Independent Physicians.

The venture capital money isn't missing. It's going exactly where it was always going.

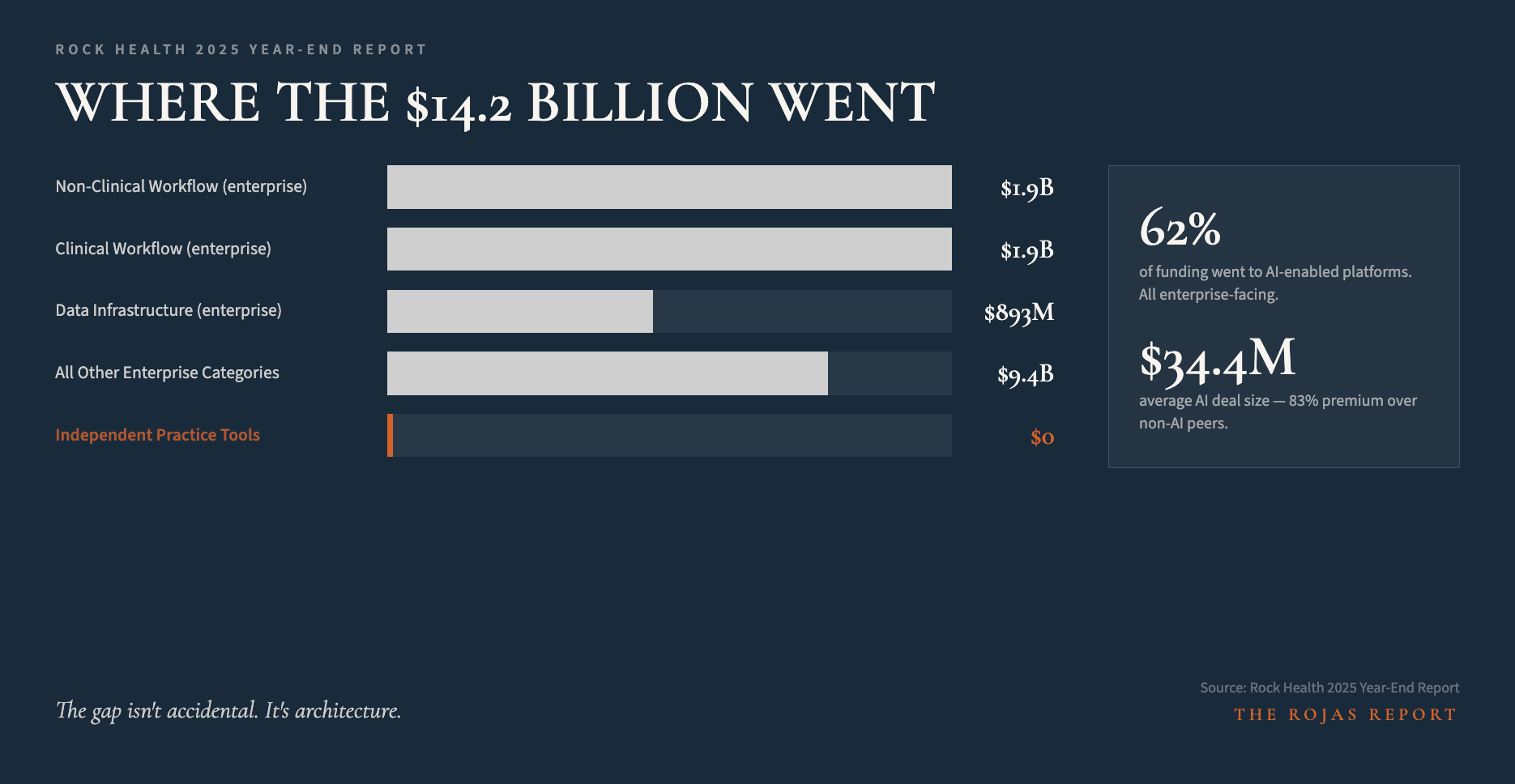

$14.2 billion.

That’s how much venture capital went into U.S. healthcare last year.

Zero of it went to independent physician practices.

That’s not a coincidence.

IN TODAY’S ARTICLE:

Where $14.2 billion in healthcare VC actually went in 2025, round by round

Why the platforms being built are structurally designed to exclude independent practices

The companies’ health systems are co-investing in to consolidate the market

What “anti-independent” architecture looks like when you name the players

Glossary at the bottom of today’s article.

THE HEADLINE THEY WANT YOU TO READ

Healthcare innovation is booming.

That’s the story. $14.2 billion into U.S. digital health in 2025 alone.

AI tools.

Workflow platforms.

Value-based care infrastructure.

The press releases write themselves.

The press releases do not mention the destination. Follow the money, and you find the same address every time.

Large health systems.

Payer networks.

Management Services Organizations are built to absorb independent practices, not support them.

The innovation is real.

The beneficiary isn’t you.

FOLLOW THE MONEY

Let’s name names.

Abridge raised $250 million in February 2025, then another $300 million in June. Ambient documentation software. Deployed at over 100 U.S. health systems and built natively into Epic’s enterprise workflow. A two-physician internal medicine practice in Wichita isn’t the customer.

Innovaccer closed a $275 million Series F in Q1 2025. Data infrastructure and care coordination. Enterprise contract minimums. Health system deployment teams. The independent gastroenterologist in Memphis doesn’t get a term sheet.

KeyCare just raised $27.4 million, bringing its total to over $55 million. Virtual care built on Epic, priced, and structured exclusively for health systems. Then look at who co-invested: WellSpan Health, Allina Health, and UCM Ventures, the venture arm of the University of Chicago Medical Center.

Read that last line again.

Health systems are on the platforms’ cap tables for the deployments they make against independent physicians. The investor and the competitor are the same entity.

This isn’t a gap in the market. A gap implies no one noticed. This is a decision. Capital is being deployed with full knowledge of where it will land and what it will build.

The consolidation playbook isn’t secret.

It’s just not reported.

Until now.

Subscribe to The Rojas Report