Behavioral Economics:

Why self-funding with a captive is the diamond in the rough.

Let me tell you about a delightful market inefficiency that most people are too conventionally minded to spot.

While everyone's wringing their hands about rising health benefit expenses, they're missing something brilliant hiding in plain sight: self-funded health plans with captive arrangements.

Here's the beautiful irony:

We've been conditioned to think that more prominent insurance companies equal better protection.

The same psychological quirk made people trust IBM in the 1980s. "Nobody ever got fired for buying IBM," they said. Well, nobody ever got fired for picking a primary insurance carrier either – but they probably should have.

Consider this delicious paradox:

By taking on what appears to be more risk through self-funding, companies end up with less risk and lower expenses. It's like discovering that jumping out of an airplane is statistically safer than crossing the street (it isn't, but wouldn't that be wonderful?).

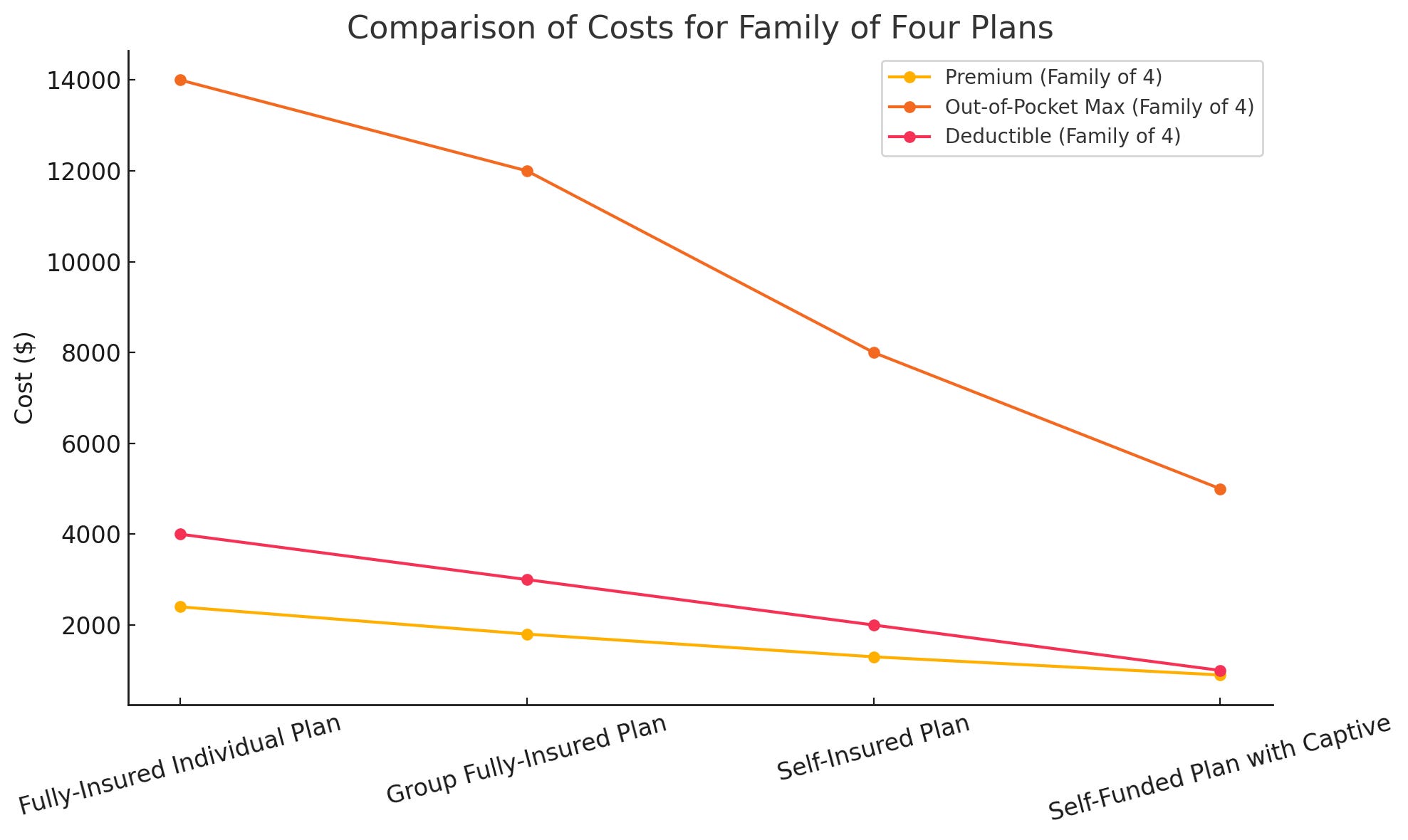

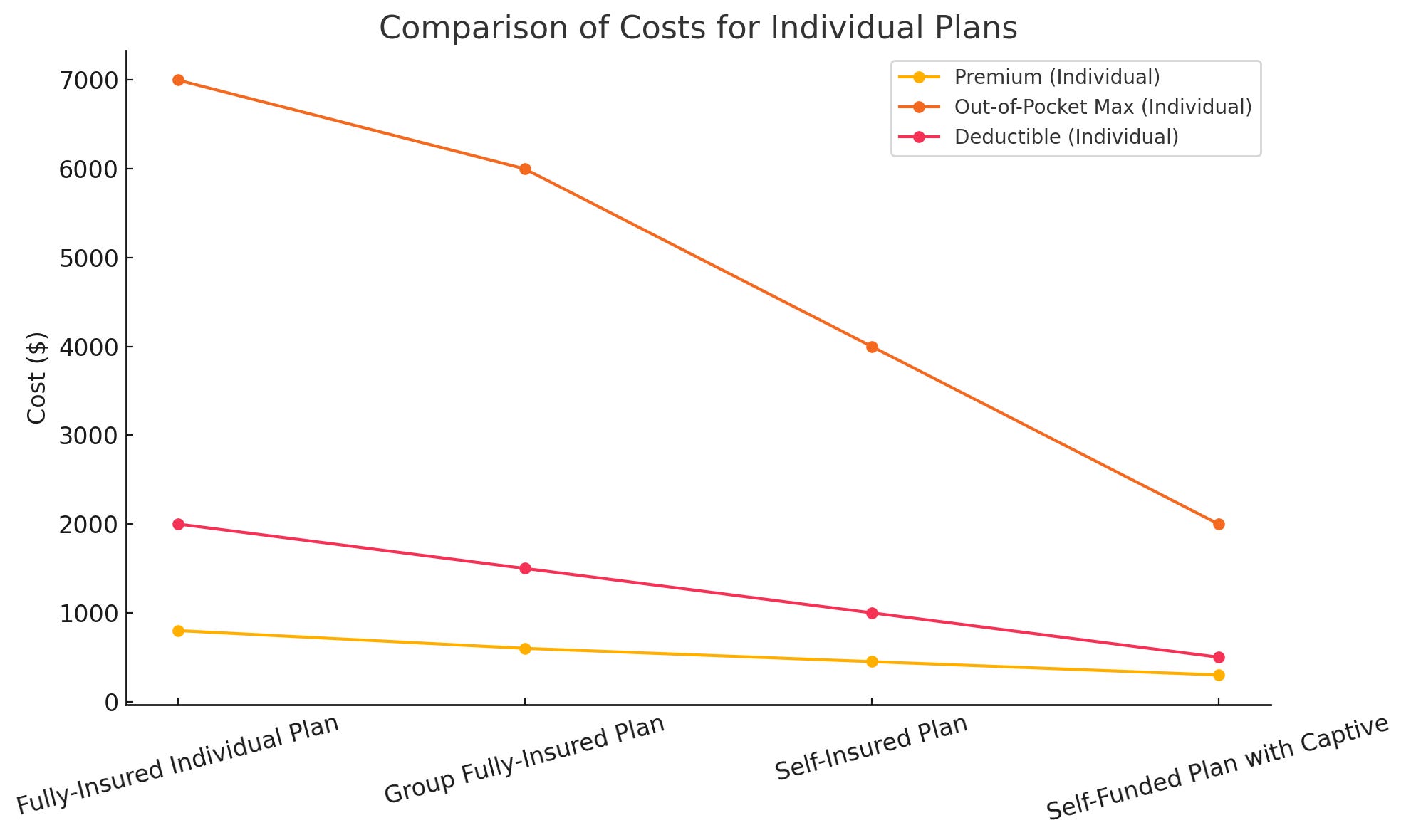

Traditional insurance plans charge a family of four about $29,000 annually because they can. It's not because they need to – it's because we've accepted this as "normal."

Meanwhile, self-funded plans with captive arrangements deliver the same healthcare for about a third of the cost. This isn't just savings; it's an arbitrage of human psychology.

What makes self-funding brilliant isn't just the mechanics—it's how it flips the entire model on its head. Companies create a micro-insurance ecosystem instead of paying an insurance company to worry about healthcare.

It's like realizing you don't need an expensive security service when your neighbors are actually better at watching your house.

Here's the part that would make any behavioral economist giddy:

The seemingly riskier option is actually safer. Traditional insurers sell peace of mind, but self-funded plans deliver it.

They're the equivalent of discovering that the generic medication isn't just cheaper than the branded version – it's actually better.

The market is mispricing self-funded health plans because they don't fit our mental model of how insurance "should" work.

This is precisely the kind of cognitive bias that creates outstanding opportunities. It's like finding out that the restaurant with the shabby exterior serves better food than the fancy one in the hotel.

By 2024, 65% of covered workers had already joined self-funded plans, up from 42% in 2020.

This isn't just a trend – it's a wake-up call that our traditional assumptions about health benefits need a complete rethink.

If you're still paying traditional insurance rates, you're essentially paying a premium for the privilege of having less control and higher expenses.

It's like insisting on buying bottled water in a city with perfectly good tap water – except this costs your company millions.

The real innovation here isn't technological – it's psychological.

Self-funding with captive arrangements isn't just a different way to structure health benefits; it's a different way to think about them entirely.

And in a world where everyone's looking for the next significant disruption in healthcare, sometimes the best solutions hide behind our preconceptions.

Remember: Sometimes, the most valuable innovations aren't new ideas but new ways of looking at old ones.

Self-funding isn't just a better mousetrap – it's realizing we've been thinking about mice all wrong. Let me tell you about a delightful market inefficiency that most people are too conventionally minded to spot.

While everyone's wringing their hands about rising health benefit expenses, they're missing something brilliant hiding in plain sight: self-funded health plans with captive arrangements.

Here's the beautiful irony:

We've been conditioned to think that more prominent insurance companies equal better protection.

The same psychological quirk made people trust IBM in the 1980s. "Nobody ever got fired for buying IBM," they said.

Nobody ever got fired for picking a primary insurance carrier, but they probably ought to have been.

Consider this delicious paradox:

By taking on what appears to be more risk through self-funding, companies end up with less risk and lower expenses.

It's like discovering that jumping out of an airplane is statistically safer than crossing the street (it isn't, but wouldn't that be wonderful?).

Traditional insurance plans for a family of four have premiums of $29,000 annually because they can.

It's not because they need to – we've accepted this as "normal."

Meanwhile, self-funded plans with captive arrangements deliver the same healthcare for about a third of the cost.

This isn't just savings; it's an arbitrage of human psychology.

What makes self-funding brilliant isn't just the mechanics—it's how it flips the entire model on its head. Instead of paying an insurance company to worry about healthcare, companies create their own micro-insurance ecosystem.

It's like realizing you don't need an expensive security service when your neighbors are actually better at watching your house.

Here's the part that would make any behavioral economist giddy: The seemingly riskier option is actually safer.

Traditional insurers sell peace of mind, but self-funded plans deliver it.

They're the equivalent of discovering that generic medication isn't just cheaper than the branded version—it's actually better.

The market is mispricing self-funded health plans because they don't fit our mental model of how insurance "should" work.

This is precisely the kind of cognitive bias that creates outstanding opportunities.

It's like finding out that the restaurant with the shabby exterior serves better food than the fancy one in the hotel.

By 2024, 65% of covered workers had already joined self-funded plans, up from 42% in 2020.

This isn't just a trend—it's a wake-up call that our traditional assumptions about health benefits need to be rethought.

If you're still paying traditional insurance rates, you're essentially paying a premium for the privilege of having less control and higher expenses.

It's like insisting on buying bottled water in a city with perfect tap water—except this will cost your company millions.

The real innovation here isn't technological – it's psychological.

Self-funding with captive arrangements isn't just a different way to structure health benefits; it's a different way to think about them entirely.

Sometimes, the best solutions hide behind our preconceptions in a world where everyone looks for the next significant disruption.

Remember:

Sometimes, the most valuable innovations aren't new ideas but new ways of looking at old ones.

Self-funding isn't just a better mousetrap – it's realizing we've been thinking about mice all wrong.

-Rojas out

Great summary of a complicated concept for MDs to understand!

pjs