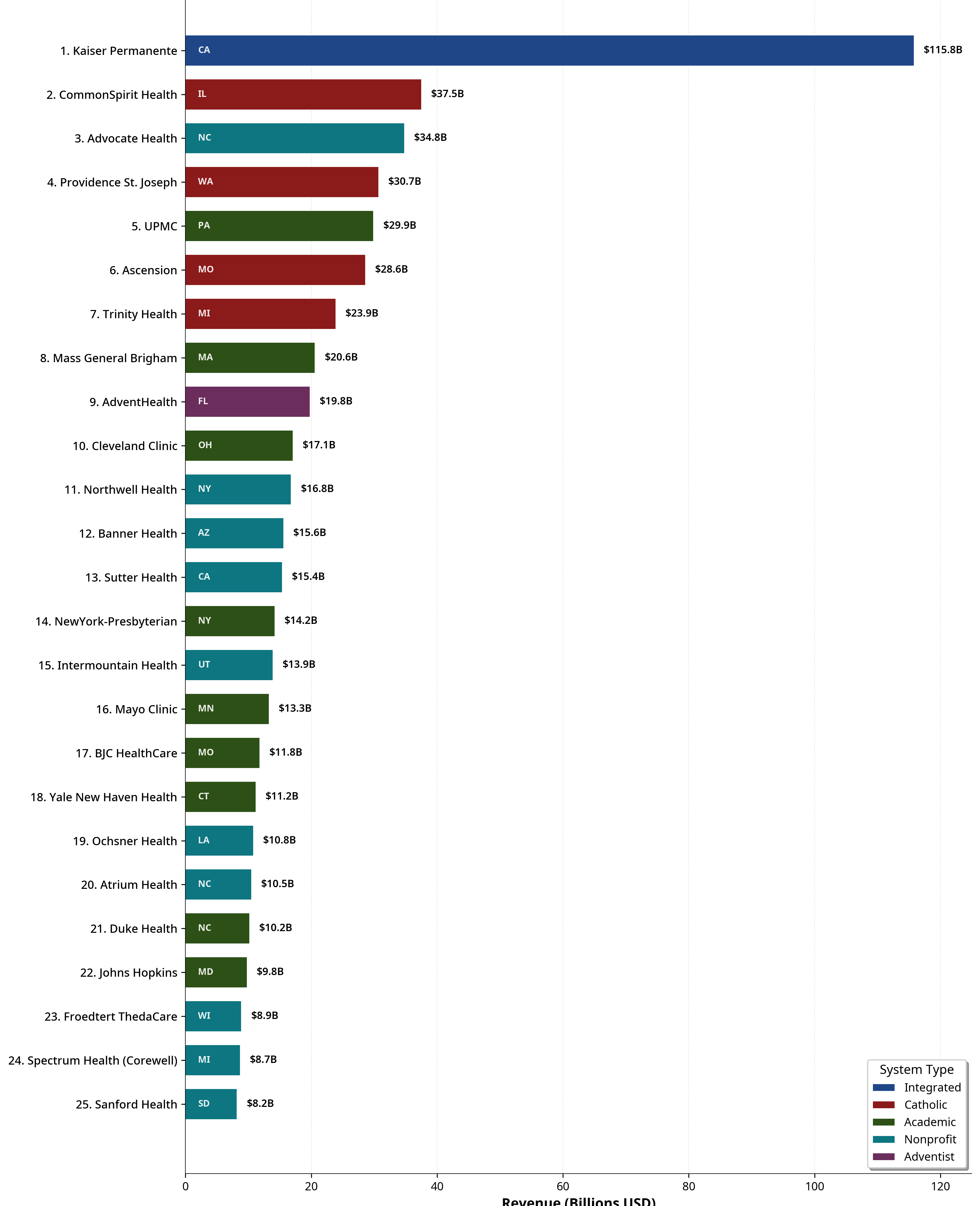

25 Most Powerful Nonprofit Health Systems in America

$527 billion in revenue. $125 billion in tax exemptions. Zero accountability.

Yesterday we showed you the map.

Today you meet the players.

These are the 25 nonprofit health systems that control American healthcare.

They pay no federal income tax.

They pay no state income tax.

They pay no property tax.

In exchange, they’re supposed to serve their communities.

Instead, they’ve built empires.

Combined, the top 25 nonprofit health systems generate over $500 billion in annual revenue, more than the GDP of Norway.

They operate in captured markets, set prices without competition, and have turned physician employment into the default career path for a generation of doctors.

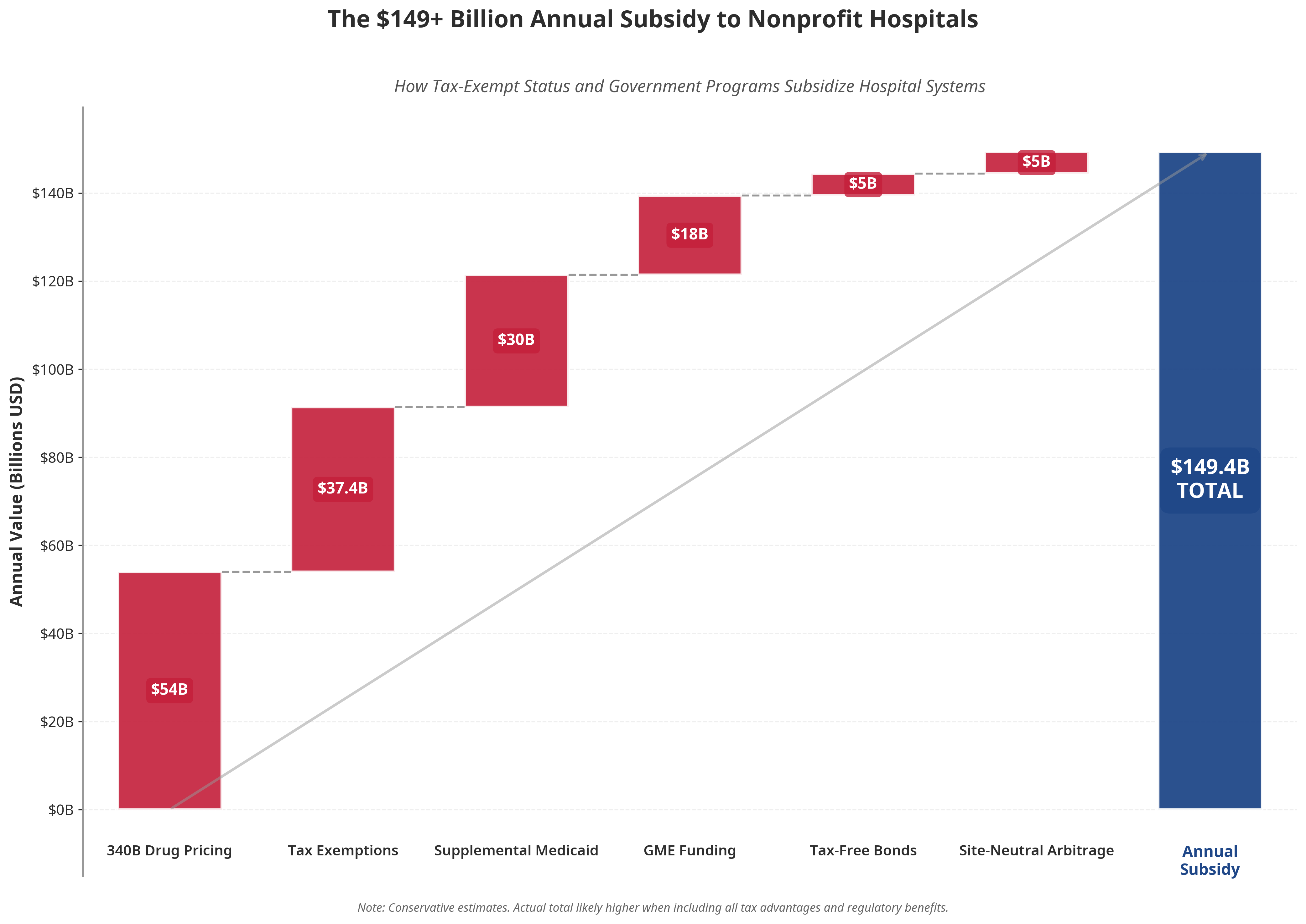

They receive over $125 billion annually in structural advantages that independent physicians cannot access. Tax exemptions. Drug discounts. Supplemental payments. Favorable reimbursement. Regulatory protection.

They are charities in name only.

THE Top 25 BY REVENUE.

THE PATTERNS YOU NEED TO SEE

1. Church Systems Built Empires Through Merger

Six of the top ten are religiously affiliated:

CommonSpirit (Catholic) — 19,009 beds

Providence (Catholic) — 10,282 beds

Ascension (Catholic) — 11,975 beds

Trinity (Catholic) — 10,903 beds

AdventHealth (Seventh-day Adventist) — 9,564 beds

These systems merged aggressively over the past two decades, consolidating Catholic hospitals into regional and national monopolies. CommonSpirit alone was formed from the merger of Dignity Health and Catholic Health Initiatives—combining operations across 24 states.

They now control nearly 100,000 beds and operate in almost every state.

The church systems share another trait: they are among the most aggressive acquirers of independent physician practices. The mission statement says “healing ministry.” The balance sheet says “market consolidation.”

2. They Don’t Receive State Funding, And They Don’t Need It

Common misconception: nonprofit hospitals receive state appropriations.

They don’t. Private nonprofit hospitals do not receive direct state funding. Only public hospitals (state/local government-owned) receive appropriations.

What nonprofit systems DO receive:

Total: $125+ billion annually in structural advantages.

Independent physicians are locked out of every single one of these programs. They pay full taxes, buy drugs at full price, receive lower reimbursement, and cannot access tax-free financing.

The nonprofit systems didn’t outcompete independent physicians. They out-lobbied them.

Tomorrow we show you exactly how.

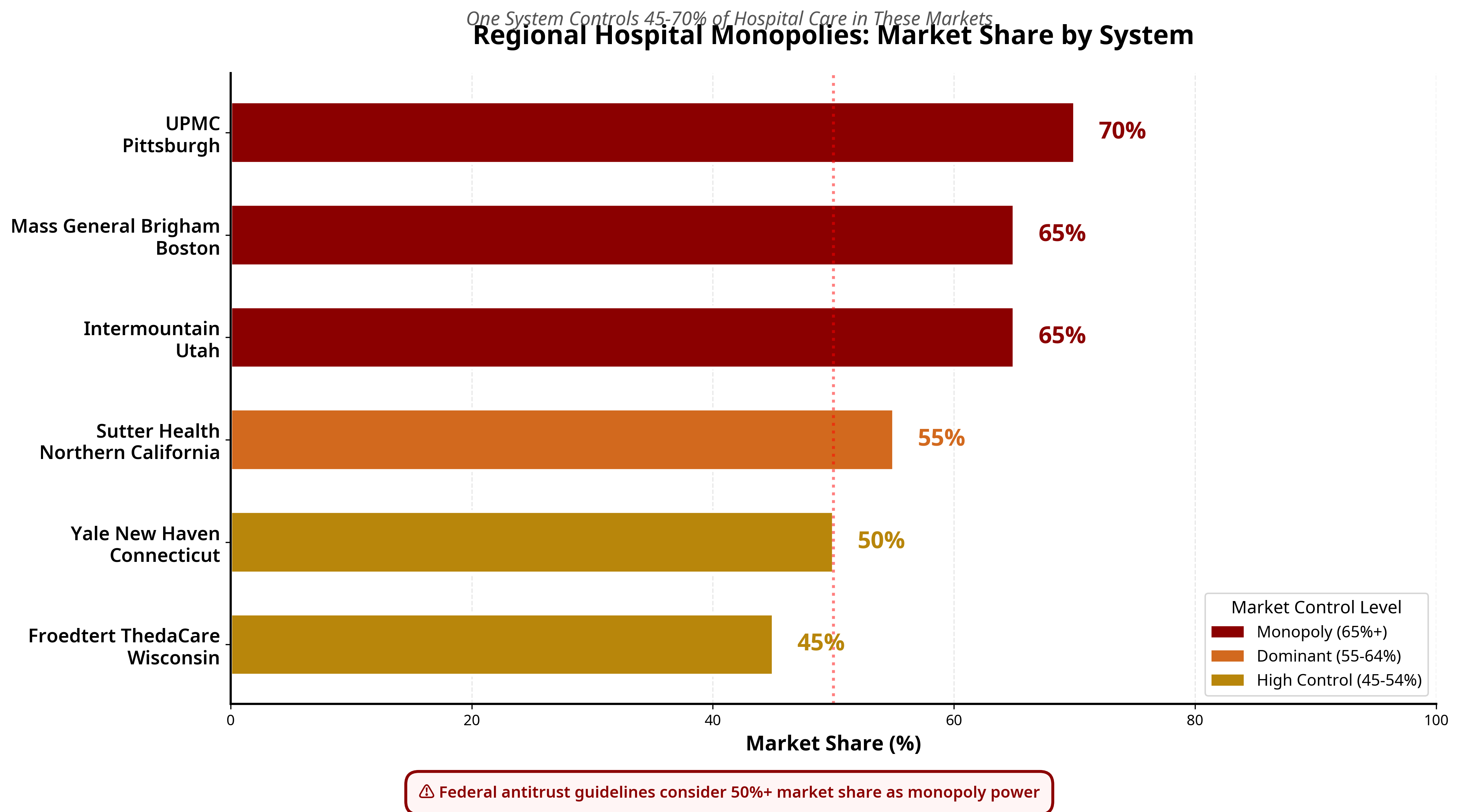

3. Geographic Monopolies Are the Business Model

These systems don’t compete nationally. They dominate locally.

When you control 50%+ of a market, you don’t negotiate prices. You dictate them.

Employers have no alternative. Insurers must include you or lose members. Patients have nowhere else to go.

This is the economics of capture, and it’s happening in 44 out of 51 U.S. healthcare markets.

4. Insurance Integration Is the Endgame

The smartest systems aren’t just providers—they’re payers too:

This is vertical integration at scale.

They collect the premium, provide the care, issue the preauthorizations, denials, and set the prices.

The patient is locked inside the system from enrollment to treatment.

Kaiser pioneered this model.

Now every major system wants to replicate it.

When a system controls both the coverage models and the hospital, competition doesn’t just decline, it becomes structurally impossible.

5. Academic Medical Centers Are the Prestige Play

A large share of the top 25 are academic medical centers:

UPMC

Mass General Brigham

Cleveland Clinic

NewYork-Presbyterian

Mayo Clinic

BJC HealthCare / Washington University

Yale New Haven

Duke Health

Johns Hopkins

These systems leverage their research reputation and training programs to justify premium pricing. “World-class care” becomes the marketing hook for $15,000 MRIs and $50,000 joint replacements.

They also receive north of $30 billion annually in Graduate Medical Education funding, federal dollars that flow only to teaching hospitals, not to the independent practices where many residents actually train.

The prestige is real. So is the pricing power.

THE TAX EXEMPTION QUESTION

U.S. nonprofit hospitals received $37.4 billion in total tax benefits in 2021, according to Johns Hopkins Bloomberg School of Public Health analysis.

That includes:

Federal income tax exemption

State income tax exemption

Local property tax exemption

Sales tax exemptions

Access to tax-exempt municipal bond financing

The question policymakers should be asking: What are communities getting in return?

The charity care numbers don’t add up. Studies consistently show that many nonprofit systems spend less on charity care than the value of their tax exemption. They sue patients for medical debt. They pay executives tens of millions. They buy physician practices and raise prices.

This is not charity. This is market capture with a 501(c)(3) wrapper.

THE PHYSICIAN IMPACT

Every system on this list runs the same playbook:

Step 1: Acquire physician practices (often below market value, often from distressed sellers)

Step 2: Convert independent doctors to employees

Step 3: Add facility fees to every visit (patients pay more for the same care)

Step 4: Restrict referrals to system-owned specialists (capture the downstream revenue)

Step 5: Eliminate competition (fewer alternatives means higher prices)

The result in states dominated by these systems:

Independent physician rates under 20%

ASC counts among the lowest in the nation

Premiums among the highest in the nation

These aren’t coincidences. They’re outcomes of a 20-year consolidation strategy, funded by $125 billion in annual structural advantages.

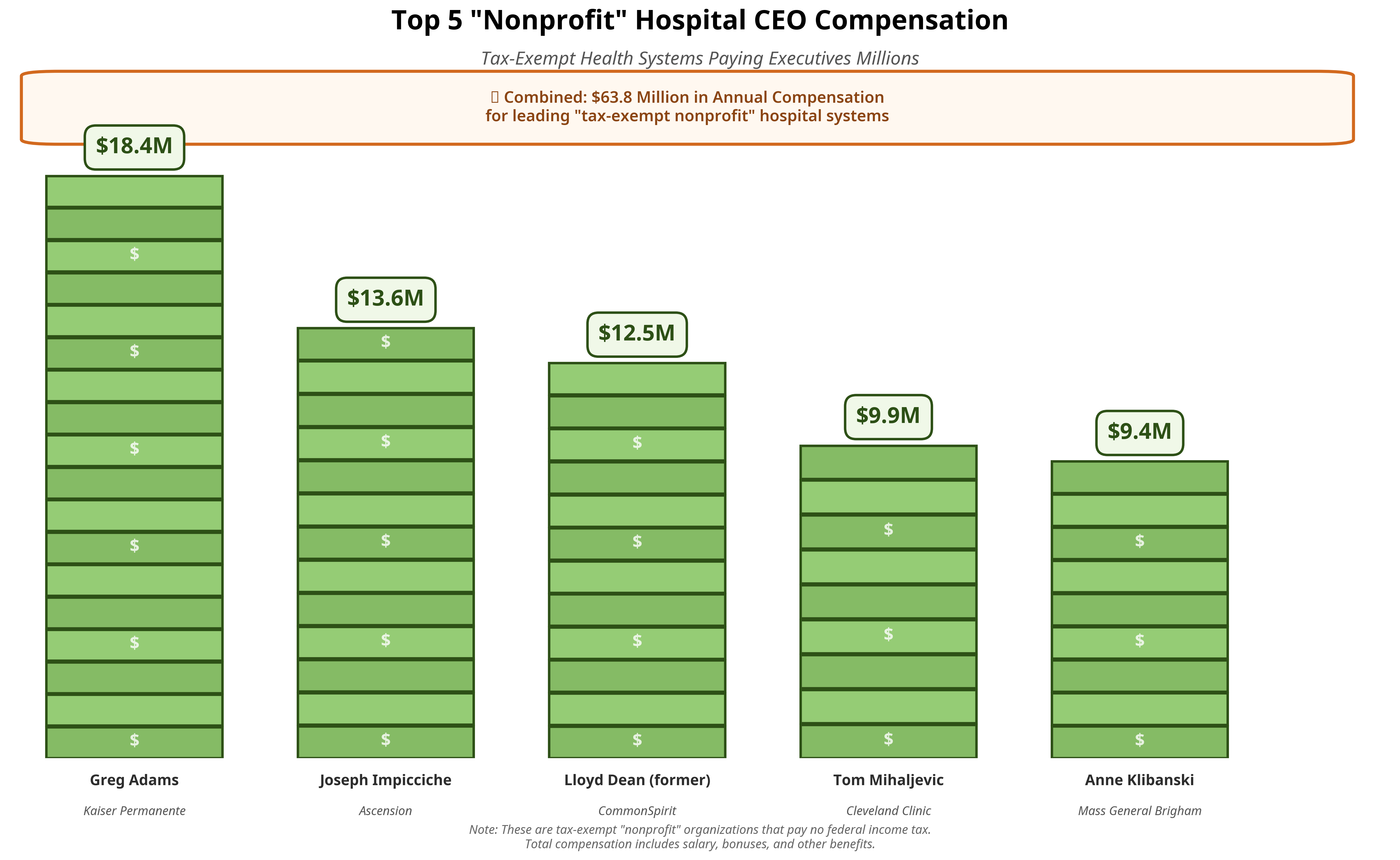

THE EXECUTIVES

These “nonprofit” systems pay like Fortune 500 companies:

The average primary care physician earns $260,000.

The CEO of a “charitable” hospital system earns 50-70x that amount.

These compensation packages are set by boards composed of business executives, donors, and former system leaders—not patients, not physicians, not the communities these systems are supposed to serve.

🎥 FEATURED CLIP

The full 70-minute History of Certificate of Need drops December 14, 2025.

THE TAKEAWAYS

25 nonprofit systems control $527 billion in annual healthcare revenue

Six of the top ten are church-affiliated systems built through aggressive merger

They receive $125+ billion annually in structural advantages independent physicians cannot access

Geographic monopolies are the business model—50%+ market share in their core regions

Insurance integration is accelerating—Kaiser, UPMC, and others control both premium and provider revenue

Executive compensation rivals Fortune 500 companies—while charity care obligations go unenforced

🎁 Give the Gift of Truth

Healthcare is 20% of the U.S. economy. Someone you know needs to understand how it actually works.

Gift them a subscription to The Rojas Report. It’s cheaper than a hospital aspirin and infinitely more useful.

Give the Gift of The Rojas Report

If this kind of data, clarity, and investigative reporting matters to you, upgrade to paid.

I’m building the only physician-led media company fearless enough to publish this every day.

$10/month or $100/year. Join the movement.

TOMORROW: The $125 Billion Heist, How Policy, Finance, and Regulation Rig Healthcare for Hospital Systems

You’ve seen the map. You’ve met the players.

Tomorrow you learn exactly how they rigged the game.

Eleven structural advantages. $125 billion annually. And not a single one available to independent physicians.

Supported by:

This publication exists because 3,000+ readers fund it.

The Rojas Report is healthcare’s first independent media company.