The $4 Trillion Time Bomb Under American Healthcare

$4 trillion. That’s the size of the U.S. municipal bond market.

The market that builds cancer centers, emergency departments, and medical office buildings.

The market that everyone assumes is safe.

It’s not.

The same playbook that blew up the housing market in 2008 is running right now in municipal finance.

And when it detonates, your hospital system, your practice, your patients, and your city are all standing in the blast radius.

What We’ll Cover Today

Most people have never heard of municipal bonds.

Fewer understand how they connect to healthcare.

Almost no one knows the fraud risk hiding in plain sight.

Today, we fix that.

In this piece:

What municipal bonds are and why they matter to healthcare.

How nonprofit hospital systems use tax-exempt bonds to build empires.

The Federal Reserve study that exposed default rates 5-20x higher than reported.

Credit default swaps: the same instrument that blew up in 2008, now sitting on muni bonds.

What happens to healthcare infrastructure if the muni market freezes.

The questions you need to ask about your hospital, your city, and your portfolio.

By the end, you’ll understand a corner of the financial system that most physicians never see. And you’ll know why it matters to your practice, your patients, and your wealth.

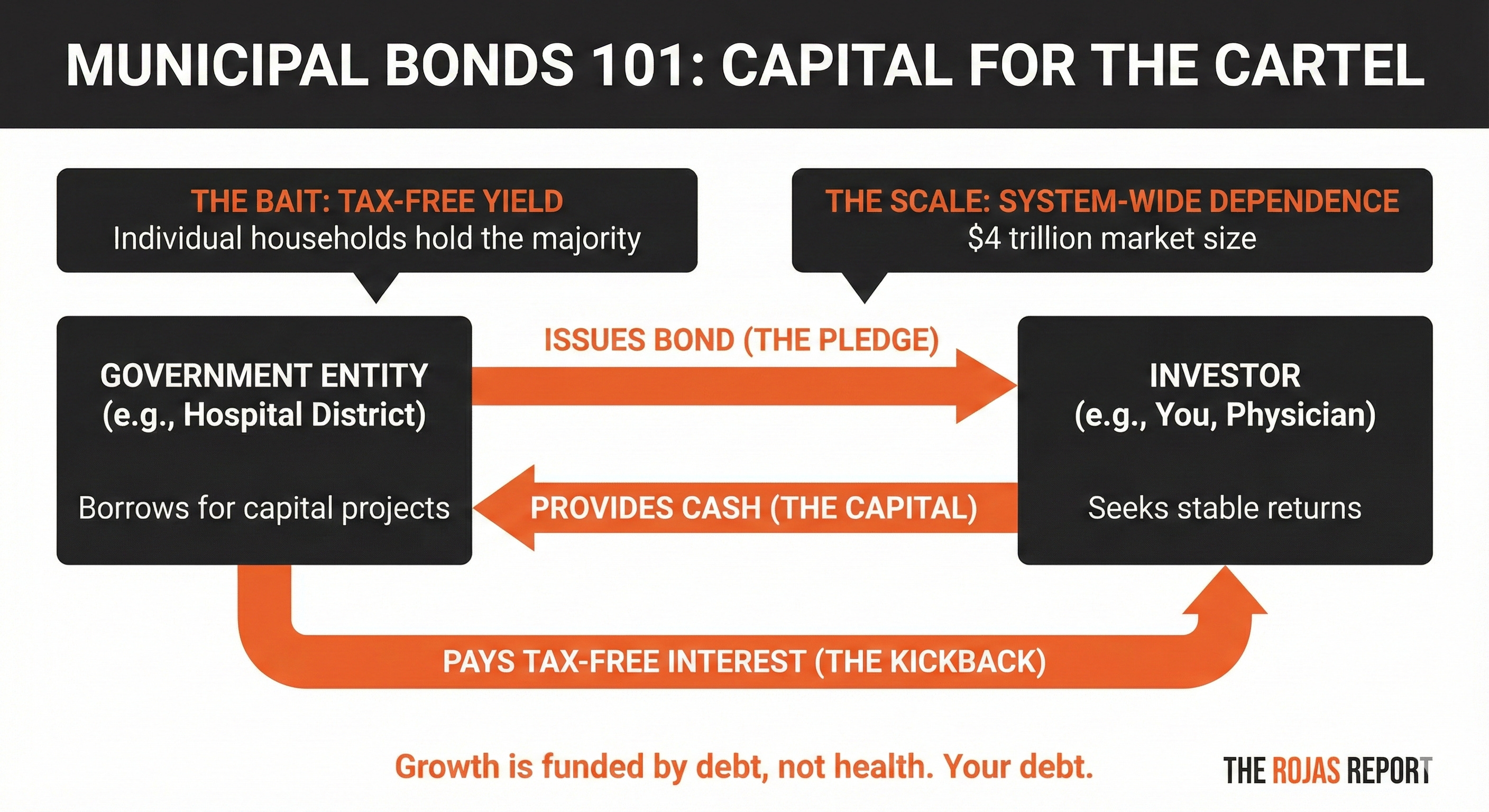

Municipal Bonds 101: The Basics

A municipal bond is a loan to a government entity.

Your city needs to build a road. It doesn’t have $50 million in cash. So it issues bonds. Investors buy those bonds. The city gets the money now. Investors are repaid over time, with interest.

The hook for investors:

Interest from most municipal bonds is exempt from federal income tax.

Sometimes, state and local taxes, too. That makes them attractive to wealthy individuals and institutions looking for tax-advantaged income.

The hook for governments:

They can borrow at lower rates than corporations because of the tax exemption. Cheaper borrowing means more projects get funded.

$4 trillion sits in this market.

Individual households hold the majority, either directly or through mutual funds. Your retired parents probably own some. Your financial advisor probably recommended them as “safe.”

The “Safe” Investment That Isn’t

Municipal bonds have a reputation.

Conservative.

Boring.

The thing your grandparents bought for tax-free income.

That reputation is built on a lie of omission.

The rating agencies, the same ones who slapped AAA ratings on toxic mortgage-backed securities in 2007, cover only a fraction of the municipal bond market.

They rate the big issuances. The visible ones. The ones with teams of lawyers and accountants making sure the paperwork looks clean.

What about the rest?

A Federal Reserve Bank of New York study found that actual municipal bond defaults between 2009 and 2019 were 5 to 20 times higher than what Moody’s and S&P reported.

Read that again.

The rating agencies missed 80-95% of the defaults.

Not because the defaults didn’t happen.

Because they weren’t looking.

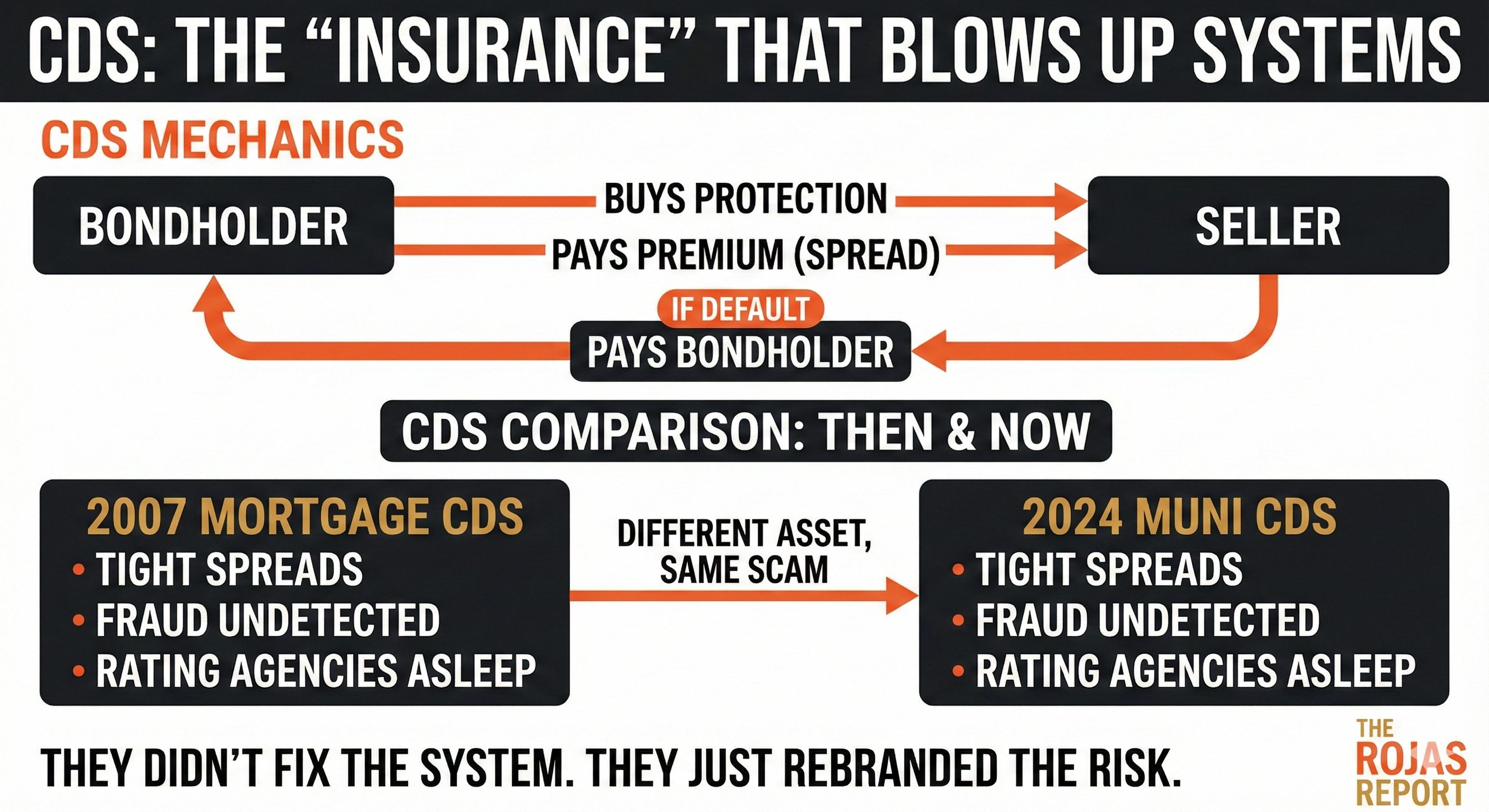

Credit Default Swaps: The 2008 Weapon Returns

Credit default swaps sound complicated.

They’re not.

A credit default swap is insurance against a borrower defaulting on their debt.

You own a bond.

You’re worried the issuer might default.

You buy a credit default swap from someone willing to take that risk.

You pay them a regular fee, called the “spread.”

If the issuer defaults, the issuer pays you the bond’s value.

The spread tells you what the market thinks about default risk.

Wide spread means high risk.

A tight spread means low risk.

In 2008, credit default swaps existed on mortgage-backed securities.

The spreads were tight.

The market believed housing was safe.

The models said prices only go up.

The models said diversification eliminated risk.

The models were wrong.

When the fraud in mortgage underwriting surfaced, the repricing was instant. Lehman Brothers. Bear Stearns. AIG.

The entire financial system froze in 72 hours.

The traders who had bought CDS protection at tight spreads made billions.

Everyone else got wiped out.

Credit default swaps exist for municipal bonds, too.

Right now, those spreads are tight.

The market believes municipal bonds are safe.

The market thinks state and local governments don’t commit fraud.

The market believes the money is where the budgets say it is.

The Fraud No One Is Looking For

A restaurant in Minneapolis called Safari.

Seats 35 people.

Claimed to serve 18,000 meals a day to hungry children during COVID.

The federal government paid them for every single one.

The children didn’t exist.

The meals didn’t exist.

The money did.

That’s one restaurant.

One city. One program.

Now scale it.

State and local governments manage trillions in budgets.

They employ millions of people.

They contract with thousands of vendors.

They issue bonds backed by revenue streams that auditors check once a year, if that.

What percentage of that is fraud?

Nobody knows.

That’s the point.

The scenario is simple:

What happens if fraud accounts for 5% of state and municipal budgets?

What about 10-15%?

At 5%, the math breaks.

That’s money that was supposed to service debt.

Money that was supposed to fund operations.

Money that exists on paper but has vanished into someone’s pocket.

CDS spreads widen.

Borrowing costs rise.

Budgets get squeezed.

At 10-15%, the market freezes.

Bond prices collapse.

Yields spike.

Governments can’t issue new debt.

Projects stop.

Payrolls get missed.

The CDS market reprices overnight.

The traders who bought protection at tight spreads make fortunes.

Everyone else gets wiped out.

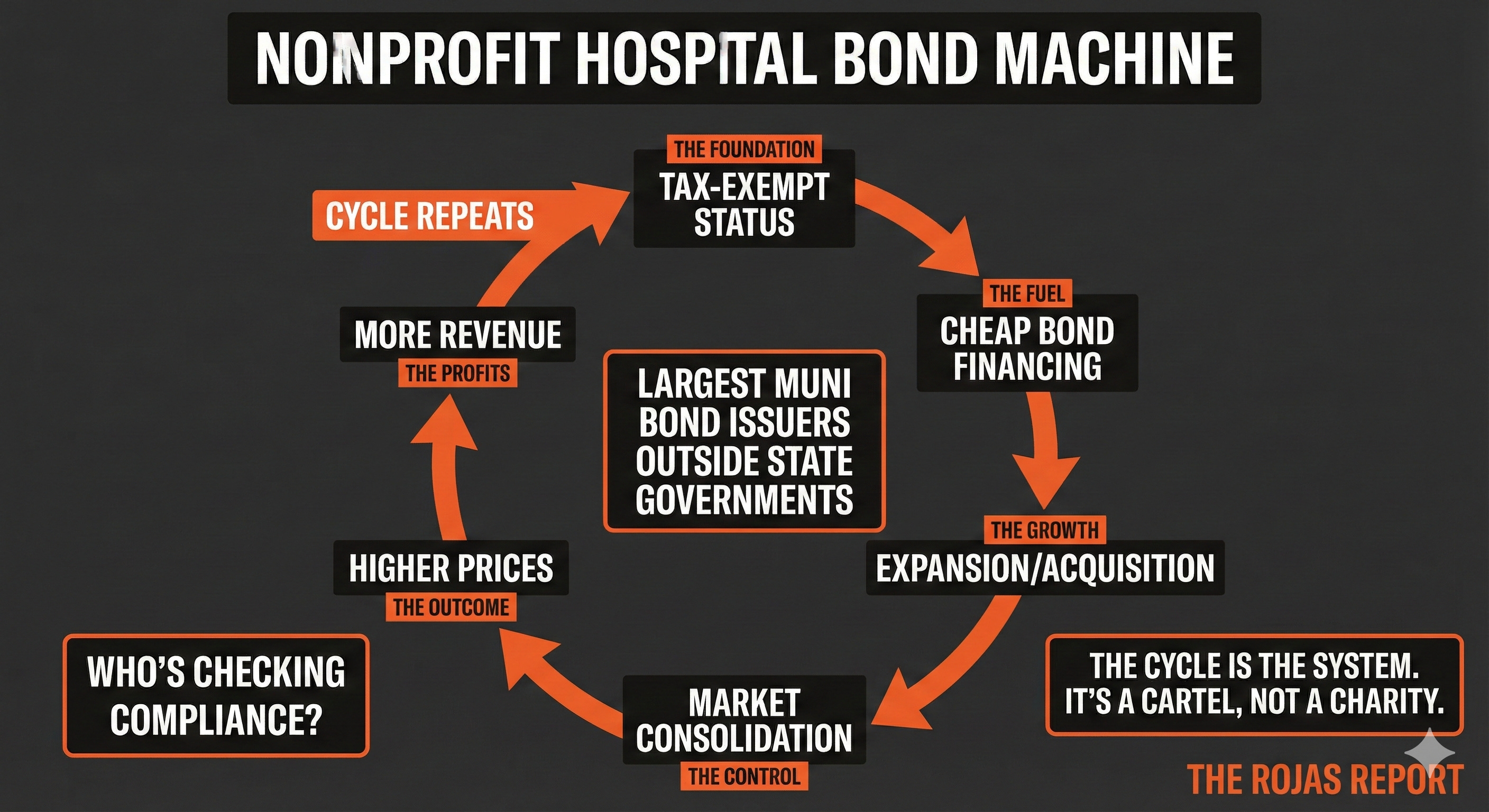

Why Healthcare Is Ground Zero

Nonprofit hospital systems are the largest issuers of tax-exempt municipal bonds outside state governments.

Kaiser. CommonSpirit Health. Ascension. Providence. Trinity Health.

These systems don’t just operate hospitals.

They operate bond portfolios worth tens of billions of dollars.

Tax-exempt revenue bonds fund their expansions.

Tax-exempt bonds build their new towers.

Tax-exempt bonds finance acquisitions that turn independent hospitals into system outposts.

The deal is simple:

In exchange for a tax exemption, these systems promise to serve their communities.

Except that the deal is broken.

These “nonprofit” systems generate billions in operating income.

They pay executives eight-figure compensation packages.

They sue patients for medical debt.

They use their tax-exempt status to borrow cheaply, acquire competitors, and build market power that independent physicians can’t match.

And their bond covenants?

Their financial disclosures?

Their compliance with tax-exempt requirements?

Who’s checking?

Free readers learn what the cartel is doing.

Paid subscribers learn how to beat them.

There's a reason the physicians building what comes next are on the other side of this paywall. They're not smarter. They just decided to stop being surprised. Subscribe here.

The Asymmetric Bet

Wall Street calls it an asymmetric bet.

Low probability.

Massive payoff.

In 2008, Michael Burry and a handful of other traders saw the housing fraud before everyone else. They bought credit default swaps on mortgage-backed securities. They paid premiums for years while everyone called them crazy.

Then the market saw what it saw.

And they made billions.

The same trade structure exists in municipal bonds today.

The market is not pricing fraud risk.

The spreads are tight.

The assumptions are rosy.

Everyone believes the money is real.

If it’s not, if even a fraction of state and local budgets are compromised, the repricing will be violent.

What Happens When the Music Stops

March 2020 gave us a preview.

Investors pulled a record $12.2 billion from municipal bond funds in the week ended March 18, 2020, followed by an even larger $13.7 billion to $14 billion the following week. The largest outflow ever recorded.

Bond prices cratered.

Yields spiked.

The market froze.

The Federal Reserve had to intervene directly, announcing it would buy municipal bonds for the first time in history. Without that intervention, cities and hospital systems would have been entirely locked out of the capital markets.

That was a liquidity crisis.

A panic.

Not fraud.

Imagine the same dynamic, but triggered by the discovery that the underlying finances were fake. That the revenues backing the bonds don’t exist. That the audits were compromised. The rating agencies, once again, missed everything.

There’s no Fed playbook for that.

The Questions You Need to Ask

If your hospital system issues tax-exempt bonds:

Who audits the bond compliance?

When was the last time anyone verified the revenue projections?

What happens to your system’s borrowing costs if muni spreads blow out?

How much of your capital plan depends on cheap tax-exempt financing?

If your state or city issued bonds for healthcare facilities:

What’s the default history on unrated healthcare bonds in your region?

Who’s checking that the facilities actually deliver community benefit?

What happens to local healthcare infrastructure if the muni market seizes?

If you manage money or own muni bonds:

Are you pricing fraud risk in your municipal bond holdings?

Do you own unrated paper you’ve never stress-tested?

What’s your exposure if CDS spreads on munis go vertical?

The Inevitability

The system isn’t broken.

It’s working exactly as designed.

Municipal bonds are supposed to fund public goods.

Instead, they fund nonprofit empires that operate like for-profit corporations while paying no taxes.

Rating agencies are supposed to identify risk.

Instead, they cover a fraction of the market and miss 80-95% of actual defaults.

Auditors are supposed to catch fraud.

Instead, they check boxes once a year and sign off on numbers nobody verified.

Credit default swaps are supposed to accurately price risk.

Instead, they reflect the market’s assumptions, which are built on the same blind spots that enabled the 2008 crisis.

When the fraud surfaces, and it always surfaces, the repricing will be fast.

The market will act like it never saw it coming. The same analysts who called munis “safe” will explain why the collapse was apparent in hindsight.

You don’t have to wait for hindsight.

The question isn’t whether there’s fraud in state and local government finances. The question is how much. And whether you’re positioned for what happens when the number becomes public.

The cartel counts on complexity to hide in plain sight.

Municipal bonds, credit default swaps, and hospital revenue financing.

These aren’t topics that make headlines.

They’re not designed to.

But they’re where the money moves.

And when you follow the money, you find the truth.

A paid subscription costs less than one hour of your billing rate.

The intelligence inside has helped physicians renegotiate contracts, exit bad deals, and see consolidation plays before they hit.

You're not paying for content.

You're paying for the advantage of knowing first.

-Rojas out.

Glossary

Municipal Bond: A debt security issued by a state, city, county, or other government entity to fund public projects. Interest payments are typically exempt from federal income tax.

Tax-Exempt Bond: A bond whose interest payments are not subject to federal income tax, and often state/local taxes. This allows governments to borrow at lower rates.

Revenue Bond: A type of municipal bond backed by the revenue from a specific project or source (like hospital patient revenue), rather than the full taxing power of the government.

Credit Default Swap (CDS): A financial contract that acts as insurance against a borrower defaulting on debt. The buyer pays a regular premium; the seller pays out if default occurs.

CDS Spread: The cost of buying credit default swap protection, expressed in basis points. A wider spread indicates higher perceived default risk.

Default: Failure to make required payments on a debt obligation, including interest or principal payments.

Rating Agency: A company that evaluates the creditworthiness of debt issuers and assigns ratings (like AAA, AA, BBB). Major agencies include Moody’s, S&P, and Fitch.

Unrated Bond: A bond that a major rating agency has not evaluated. These are typically smaller issuances and carry unknown risk profiles.

Yield: The return an investor receives on a bond, expressed as a percentage. When bond prices fall, yields rise.

Liquidity: The ease with which an asset can be bought or sold without significantly affecting its price. A “frozen” market has no liquidity.

Asymmetric Bet: An investment with limited downside but potentially massive upside if a low-probability event occurs.

Bond Covenant: A legally binding term in a bond agreement that requires the issuer to meet certain conditions or refrain from specific actions.

501(c)(3): The section of the Internal Revenue Code that grants tax-exempt status to nonprofit organizations, including most nonprofit hospitals.

Sources

Appleson, J., Parsons, E., & Haughwout, A. (2012, August). “The Untold Story of Municipal Bond Defaults.” Federal Reserve Bank of New York.

Campbell, S., & Wessel, D. (2020, August). “How well did the Fed’s intervention in the municipal bond market work?” Brookings Institution.

Long ago we held municipal bonds because they were deemed “safe.” But then our spidey senses kicked in — even without knowing any of the great information you provided in this article. We decided to stop putting money into munis and never looked back. It’s all built on a house of cards (if not outright fraud).

Hospital systems truly are making out like bandits in every sense of the word.

Great article Dutch, as per usual. I was once involved with a hospital ownership team who went down the path of issuing bonds. I frankly could not believe the willingness on behalf of the bond issuer to ignore what was obvious…the hospitals were going concerns, neither had the cash flow to support the bond payments, not even close. But yet the process moved forward. It never happened, thank God! I was gone long before then. I just could not in good conscience watch it happen.