The ACA Didn’t Regulate Insurers. It Underwrote Them.

Nineteen tickers. Five snapshots. One verdict: the law worked exactly as designed. Just not for you.

March 23, 2010.

The Affordable Care Act becomes law.

The insurance lobby warns of ruin.New taxes.

Profit caps.

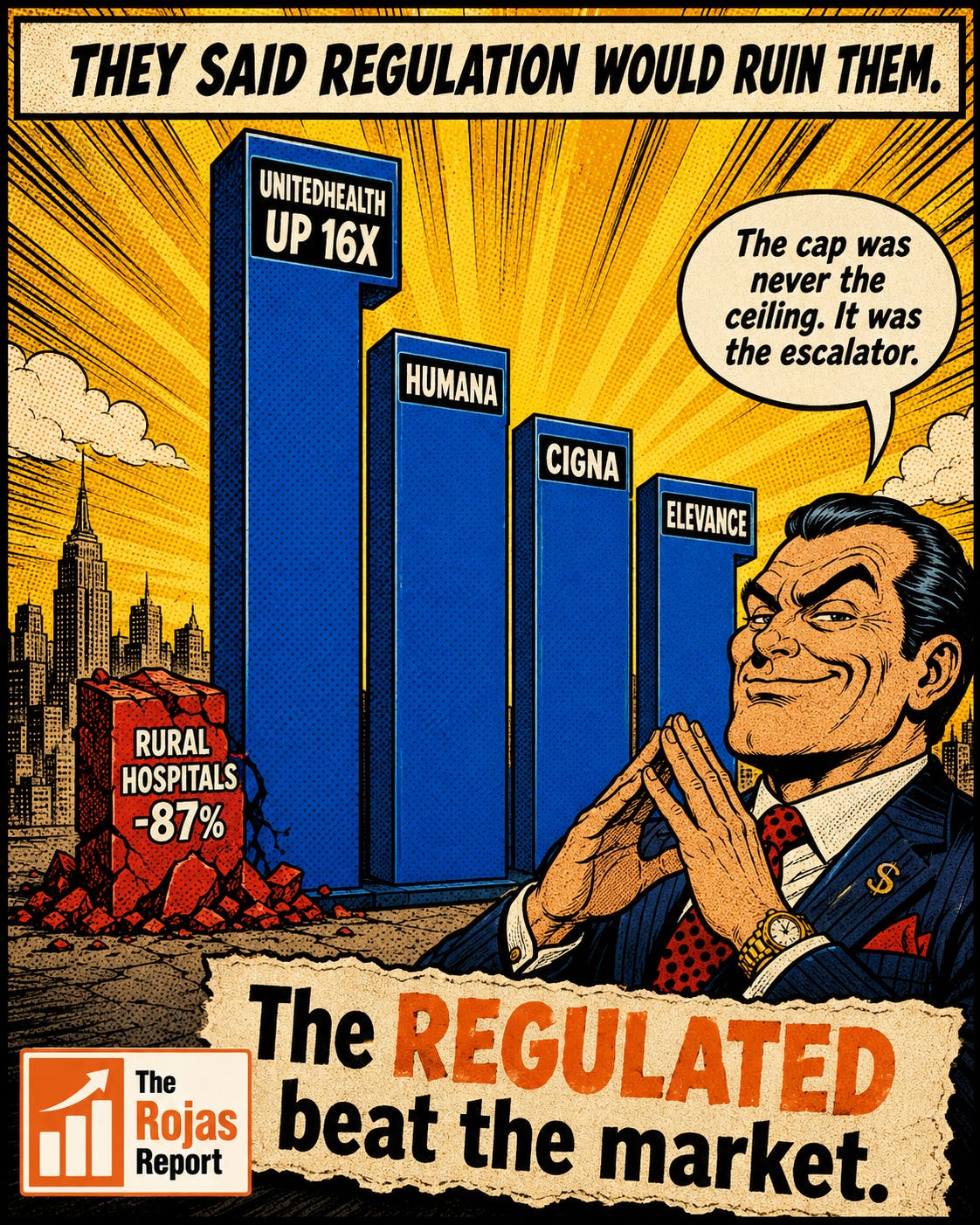

Coverage mandates.UnitedHealth trades at $25 that spring.

Today it trades at $425.

Humana went from $41 to $397.

Cigna from $33 to $288.Ruin looks a lot like a 1,000% return.

IN TODAY’S ARTICLE:

The 2010 panic that never happened: why Wall Street briefly feared the ACA, and how fast that fear converted into the trade of the decade

The scoreboard: healthcare tickers across 21 years, and why the claims layer beat the cure layer by an order of magnitude

The 80/20 rule that became a growth mandate: how capping profit as a percentage made healthcare inflation a fiduciary duty

Who lost: rural hospitals down 87%, device makers flat, and what that tells physicians about where the money actually flows

Glossary at the bottom of today’s article.

THE FEAR THAT NEVER HAPPENED

In the winter of 2009, the health insurance industry told America it was fighting for its life.

The bill moving through Congress bans the denial of coverage for pre-existing conditions. It taxed insurers and device makers. It imposed a Medical Loss Ratio: insurers must spend at least 80 cents of every premium dollar on actual care, and 85 cents in the large-group market. Anything less gets rebated to customers.

On paper, that reads like a leash.

Markets briefly believed it. President Obama signed the ACA on March 23, 2010, and insurer stocks wobbled. Analysts wrote about margin compression. The industry’s trade group warned that reform meant rationing, ruin, and premium spirals.

Then the checks started clearing.

Medicaid expansion added millions of new members, paid for by taxpayers and administered by private plans. The exchanges delivered millions more, premiums subsidized by the Treasury. Medicare Advantage, already growing, became the industry’s favorite product: government rates, private margins.

The leash turned out to be a pipeline.

THE SCOREBOARD

Read these numbers like a jury reads evidence. Adjusted closing prices, spring 2010 (the weeks after the ACA signing) to July 2026:

The claims layer:

UnitedHealth: $25 to $425. Up roughly 16x.

Humana: $41 to $397.

Cigna: $33 to $288.

Elevance (then Anthem): $51 to $418.

The distribution layer:

McKesson: $59 to $786. From 2005, that is a total return of 2,864%. A drug distributor. Not a drug inventor. A company that moves boxes between the people who make medicine and the people who take it.

The people who actually touch patients:

Community Health Systems, one of the largest rural hospital operators in the country: $31 in 2010. Under $4 today. Down 87% since the ACA passed.

Medtronic, which makes the devices surgeons implant: up 169% over 21 years. The S&P 500 did far better.

Boston Scientific: up 31% over 21 years. Twenty-one years.

The pattern is not subtle. The further you get from the patient, the better the return. The closer you get to the claim, the richer you become.

Pharma is the one exception that proves the rule. Eli Lilly is up nearly 3,900% since 2005, but the overwhelming share of that gain came in the last five years, driven by GLP-1 drugs. Lilly got paid for inventing something. The insurers got paid for existing.

Every healthcare conference has a panel on “fixing the broken system.”

Nobody on that panel reads a stock chart.

100,000 physicians, healthcare executives, and lawmakers read the receipts here every month, and the receipts live nowhere else.