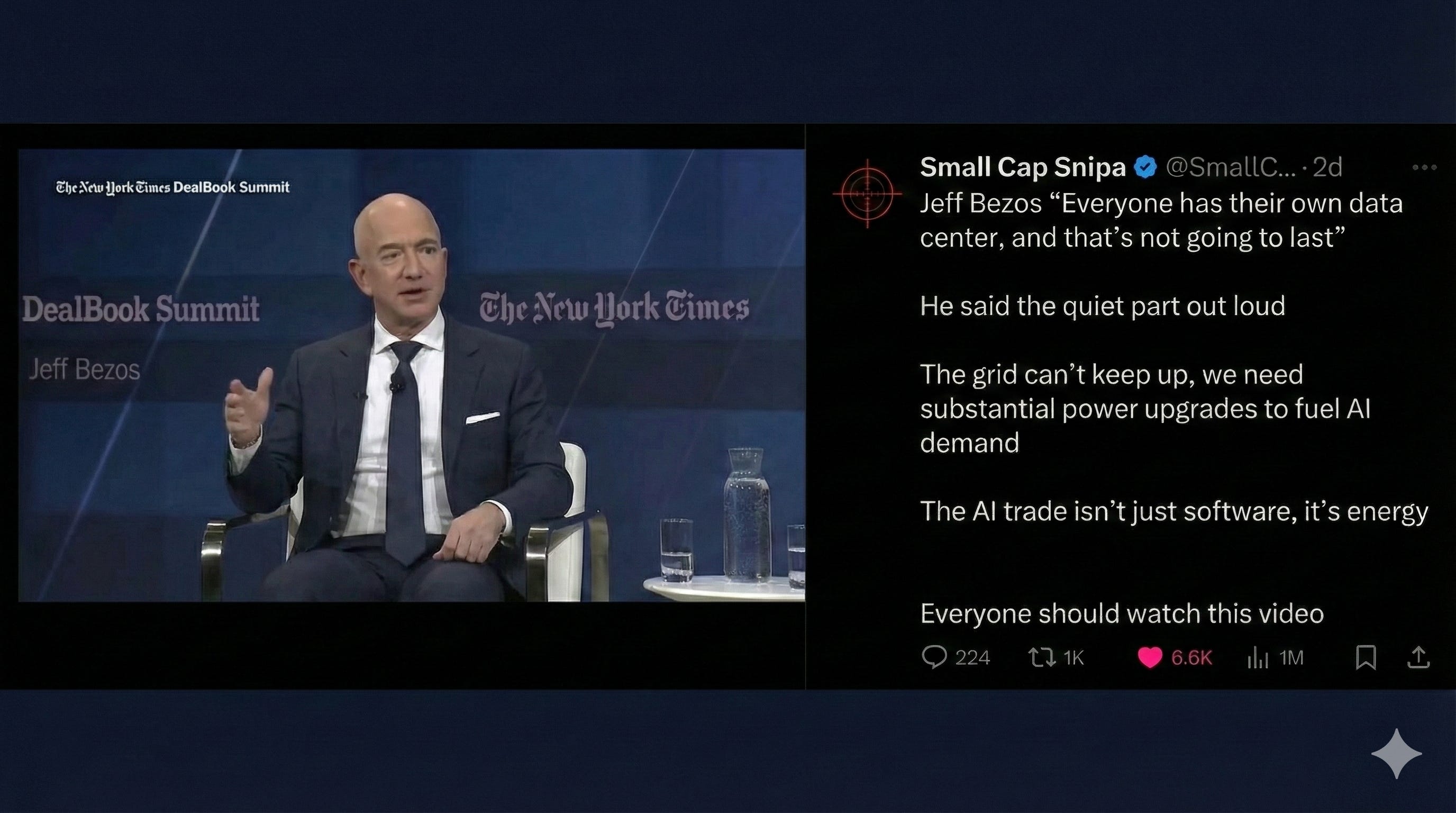

THE BILLIONAIRE SAID THE QUIET PART OUT LOUD

Jeff Bezos just explained what’s coming for healthcare. He wasn’t talking about healthcare.

“Everyone has their own data center, and that’s not going to last.”

Jeff Bezos. DealBook Summit. December 2025.

He wasn’t talking about medicine. But he was describing it perfectly.

IN TODAY’S ARTICLE:

Why the AI infrastructure thesis applies to healthcare

How AWS won by solving a legibility problem

The co-opetition alternative nobody built

Why the window is closing

Glossary at the bottom of today’s article.

THE PATTERN

Bezos is right.

Fragmented infrastructure loses. The capital requirements are too high.

The complexity is too great. The inefficiencies are too expensive.

Independent data centers couldn’t compete.

AWS absorbed them.

Azure absorbed them.

Google Cloud absorbed them.

The consolidators won.

Now look at healthcare.

The commonly cited statistics understate the problem.

The American Medical Association reports that 42% of physicians remain in “private practice.”

That number is a lie.

It includes PE-affiliated practices, which are independent in name only.

The real number: 12%.

Across cardiology, gastroenterology, oncology, orthopedics, and urology, only 12% of physicians remain in truly unaffiliated private practice. Hospital systems employ 55%. Corporate entities like Optum own 23%. PE-backed MSOs are consuming what’s left.

The pattern is identical.

The consolidators have already won.

Bezos said the quiet part out loud: fragmentation is a temporary condition. In healthcare, it’s nearly a historical artifact.

The strange thing about consolidation is that everyone sees it happening and no one thinks it applies to them." → The rest of this article breaks down the only structural alternative. Paid subscribers get the playbook. Subscribe

WHY AWS WON

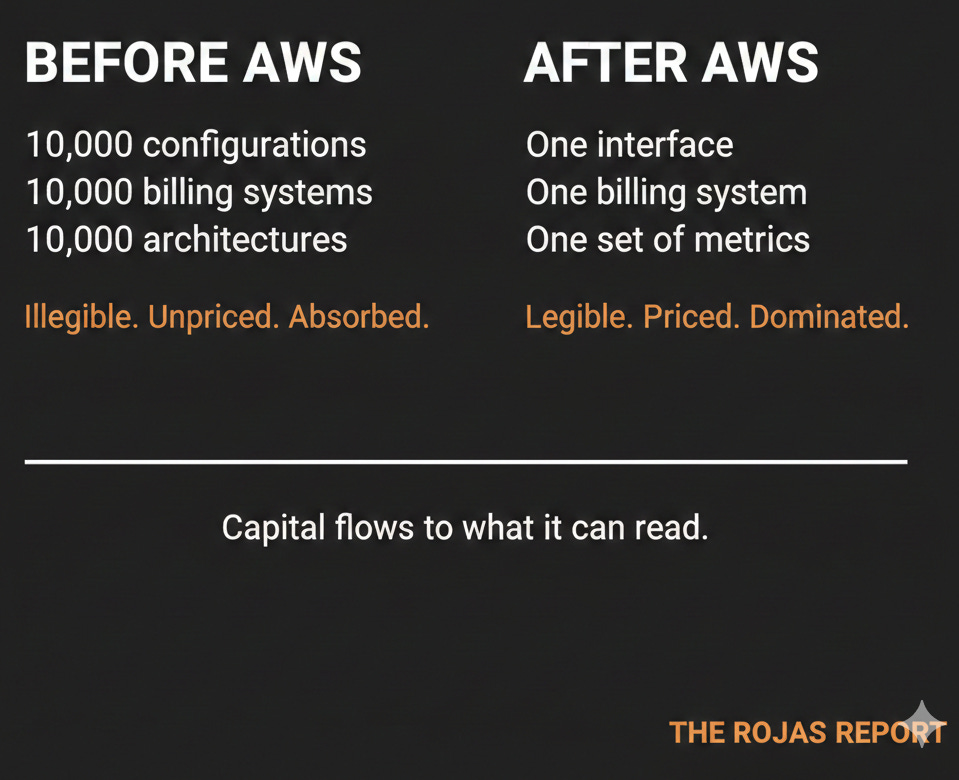

AWS didn’t just offer cheaper servers.

AWS offered legibility.

Before AWS, every company ran its own infrastructure. Custom configurations. Proprietary systems. Unique architectures. A nightmare for investors, auditors, and acquirers trying to understand what they were looking at.

AWS standardized the stack.

One interface. One billing system. One set of metrics.

One way of seeing.

Capital markets could finally read the infrastructure.

They could price it. Audit it. Compare it.

Legibility to capital was the product.

Compute was just the delivery mechanism.

This is the same dynamic we described in Article 1.

States cannot act on what they cannot see.

Neither can markets.

Independent data centers were illegible to capital.

AWS made infrastructure visible.

Capital flowed to what it could read.

Independent practices are illegible to payers, to regulators, to capital. Hospital systems are visible. PE platforms are visible. They offer one contract, one data stream, one compliance structure.

Capital flows to what it can read.

The question isn’t whether independent medicine will become legible. It will. The question is who makes it legible, and who captures the value when it happens.