The Carriers Have a 30-Year Problem. They Solved It By Charging You More.

A 55.7 percent decline in claims would produce a refund in any other insurance line. It produced seven straight years of rate hikes instead. The float is the business.

There is a number in the malpractice industry’s own data that the AMA does not want you to add up.

Frequency down 55.7 percent over thirty years.

Premiums up every year since 2018.Do the math on who that math serves.

In Today’s Article:

Thirty years of frequency data. Seven years of premium data. The chart that the carriers do not put in their renewal mailers.

The Studdert finding that 1 percent of physicians produce 32 percent of paid claims. And what carriers do with the other 99 percent.

The Hyman finding that one paid claim makes the next one 3.7 times more likely. And why your premium does not reflect that you have zero.

How a cell captive turns this entire arithmetic against the carrier and back into your balance sheet.

Glossary at the bottom of today’s article.

THE NUMBERS THE AMA PUBLISHED

In April, the American Medical Association issued a press release. The headline called the medical liability system “broken.”

The press release then printed numbers that say the opposite.

In 1992, the rate of paid malpractice claims against US physicians began a steady descent. A 2017 JAMA Internal Medicine analysis by Schaffer and colleagues tracked the trajectory. Across all specialties, the rate of paid claims fell 55.7 percent between 1992 and 1996 and between 2009 and 2014. Less litigation. Fewer payouts. Year after year.

The AMA’s own 2024 data continued the decline.

The proportion of physicians who have been sued at least once in their careers dropped from 34 percent in 2016 to 28.7 percent in 2024.

In any other insurance line, that data would result in a rate reduction.

Auto premiums fall when accident frequency falls.

Property premiums fall when claim severity drops.Medical malpractice premiums have climbed nationwide for the seventh consecutive year.

The longest sustained upward trend since the early 2000s.

All against a thirty-year decline in claim frequency.

The AMA published both data sets.

The AMA called the result a broken system.

The carriers reading that press release called it a record.

THE CONCLUSION THE AMA REFUSED TO DRAW

There are two ways to interpret “fewer lawsuits, higher premiums.”

The first interpretation is the AMA’s. The litigation environment has grown more severe. Verdicts have grown larger. Lawyers have grown more aggressive. The system needs reform. Cap the damages. Limit the fees. Restore balance.

This is the interpretation that has been on offer for forty years. It is also the interpretation that does not name the party that benefits from those seven straight years.

The second interpretation is the one the data actually supports. A 55.7 percent decline in frequency, combined with seven consecutive years of rate increases, describes a market in which the price-setter has decoupled premium from risk. That is not a broken market. That is a captured one.

The party that captured it, is not the trial bar. It is the carriers.

The Doctors Company. MedPro Group. ProAssurance. Coverys.

The commercial medical professional liability sector did not produce the thirty-year decline in claim frequency.

Physicians did.

By practicing better medicine.

By refining surgical protocols.

By building surgical hospitals and ambultory surgery centers.

By building safety cultures inside their hospitals and practices.The carriers captured the savings.

The physicians got the renewal letter.

WHO ACTUALLY GETS SUED

The decline in frequency is not evenly distributed.

In 2016, David Studdert and colleagues published a paper in The New England Journal of Medicine stating that carriers do not disclose their premiums when explaining them. It found that one percent of US physicians account for thirty-two percent of all paid malpractice claims.

Read that sentence until you see it.

A small fraction of physicians produce nearly a third of all losses.

In 2023, David Hyman and colleagues extended the finding in JAMA Health Forum. They showed that a single paid claim increases the likelihood of the next paid claim by 3.7 times. Two paid claims, nearly 7 times. Three or more paid claims, over 11 times. Past claims predict future claims with statistical force that would reshape every premium calculation in the industry.

It does not.

A neurosurgeon with twenty years of clean practice pays the same range of premiums as a neurosurgeon with three closed claims. The experience rating is too coarse to separate them. The carrier’s actuarial team understands the 1 percent rule. The carrier’s pricing team does not price aggressively against it.

This is not accidental.

It is the underwriting design.

If carriers priced the 1 percent at their true loss profile, those physicians would be uninsurable in the commercial market. They would exit practice or move to risk pools. The 99 percent would see immediate premium relief.

That premium relief is the lost revenue the carriers refuse to give back.

The cross-subsidy is the product.

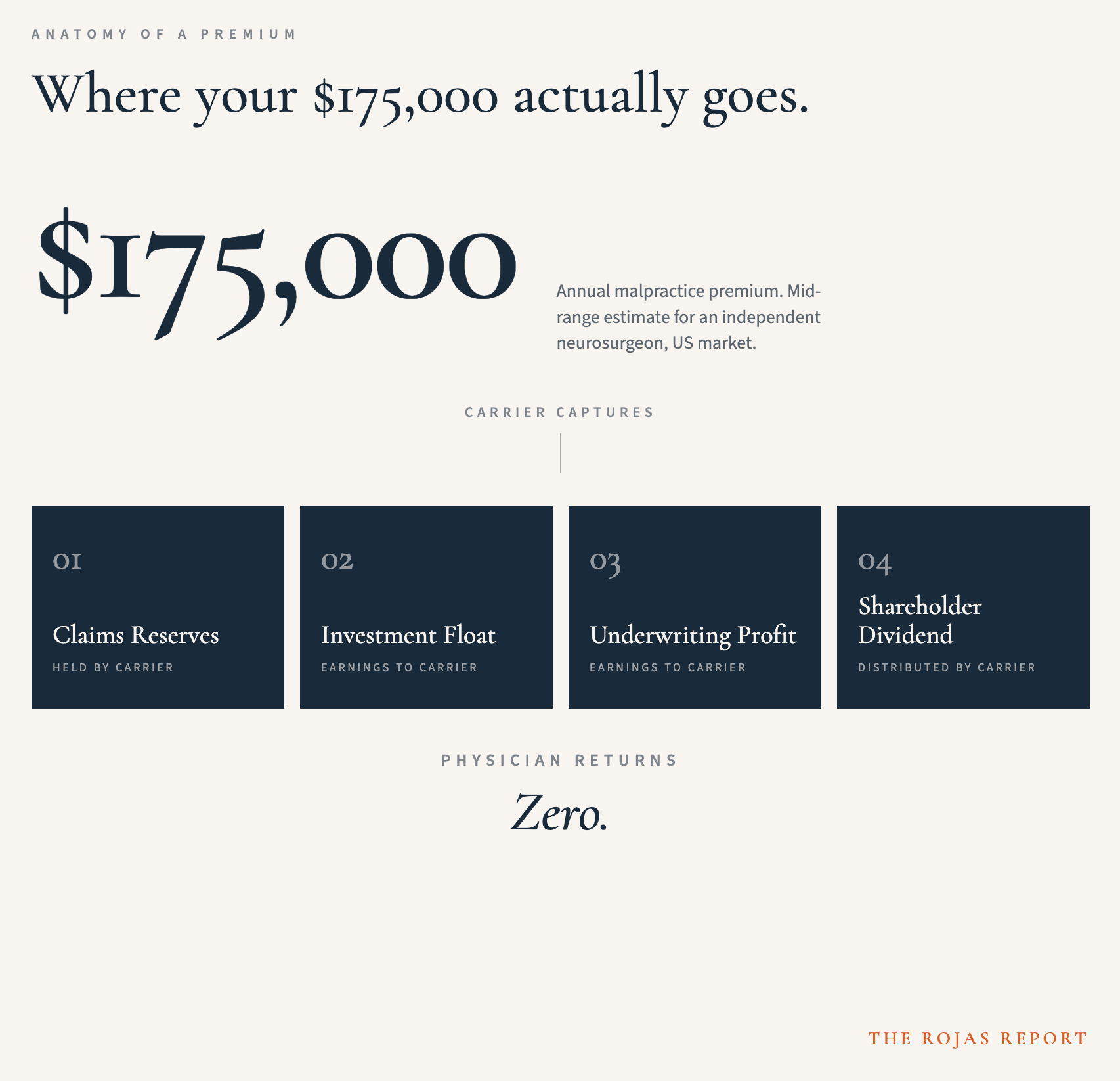

WHERE THE PREMIUM GOES

A neurosurgeon paying $175,000 a year in malpractice premium is doing four things at once.

First, she is funding her own future claims, projected by an actuarial model.

Second, she is funding the future claims of every other neurosurgeon in the carrier’s book. Including the ones with three closed claims.

Third, she is funding the carrier’s investment portfolio. The premium does not sit in a vault. It is deployed into bonds, equities, real estate, and structured credit. The carrier holds the premium against future claims and earns investment income on it. The hold is called float. The income belongs to the carrier.

Fourth, she is funding the carrier’s underwriting profit. If claims come in below the actuarial projection, the unspent premium is recognized as earnings. The earnings flow to the carrier’s shareholders.

Of those four dollars, the neurosurgeon owns zero. None of them. The reserves return as claim payments only if she has a claim. The float income is captured. The underwriting profit is captured. The shareholder dividend is captured.

She wrote the check.

The carrier owns everything that the check produced.

The carriers raised rates for 7 years in a row while claim frequency hit a 30-year low.

You can keep funding that arithmetic.

Or you can subscribe and learn how to flip it.