The Quiet $81 Billion:

How a 1992 Drug Discount Outgrew the NIH and Started a Federal War

In 1992, Congress wrote a paragraph to keep HIV clinics and rural hospitals alive. By 2024, that paragraph was moving $81 billion a year.

In December 2025, a federal judge in Maine froze the reform plan, and 40+ pharmaceutical manufacturers, 20+ state legislatures, the Trump White House, the American Hospital Association, and your community hospital are now in open conflict over who controls the money next.

There is a federal drug pricing program in this country that moves more money than the entire National Institutes of Health budget. Most physicians have never read its statute. Most lawmakers cannot explain how it works. Most patients have no idea their hospital is participating in it.

It is called 340B.

In 2024, it hit $81 billion in drug purchases. 40+ pharmaceutical manufacturers are in open revolt against it. 20+ state legislatures have passed laws to defend it. The Trump administration wants to move it to a different agency. A federal judge in Maine just froze the centerpiece of the reform plan.

And the fight has barely started.

IN TODAY’S ARTICLE

A 340-character paragraph in a 1992 veterans health bill became an $81 billion shadow drug economy. The statute does not require any of the savings to reach the patient. Read that sentence twice.

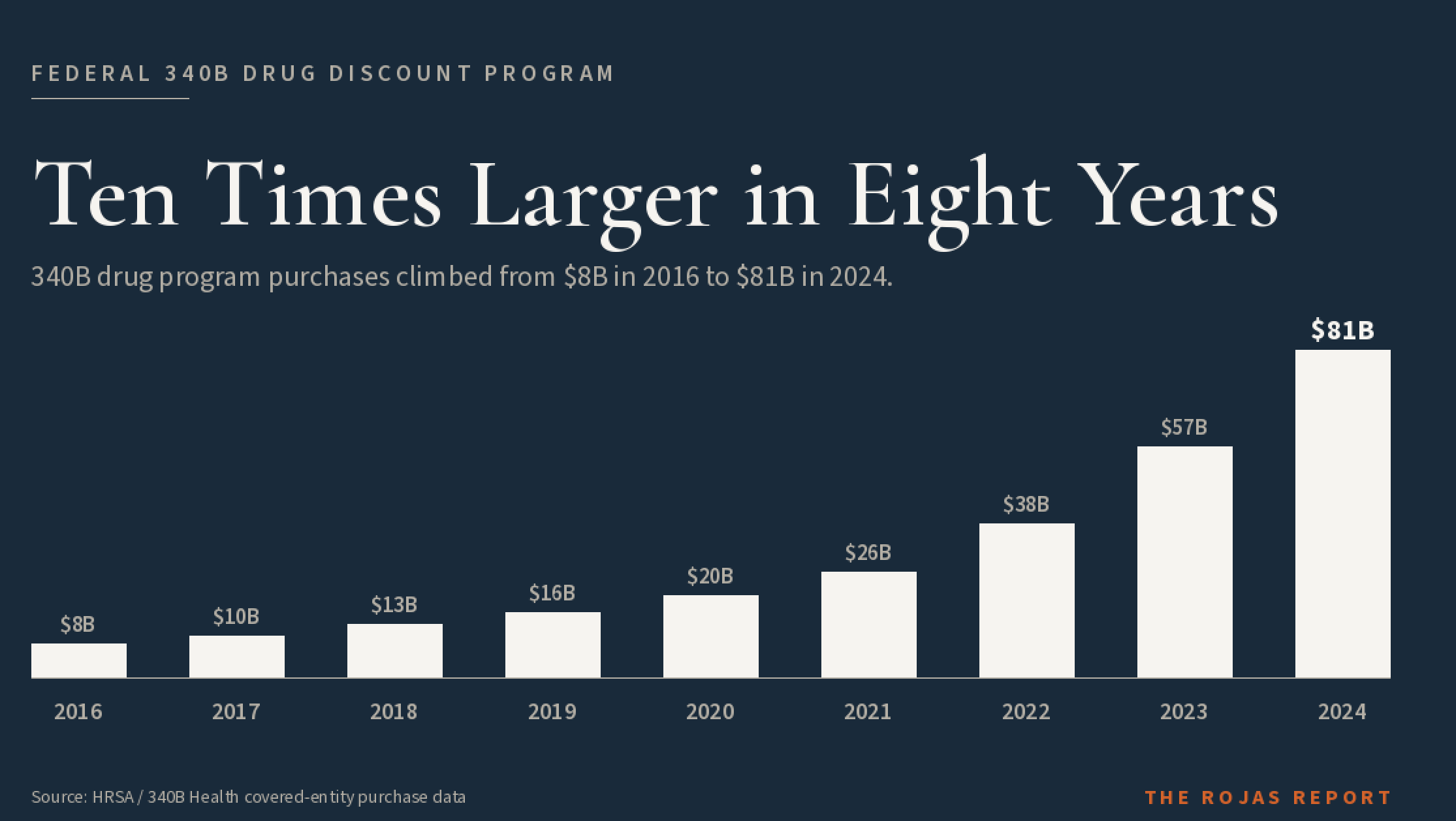

The 10x growth curve. 340B drug purchases jumped from roughly $8 billion in 2016 to $81 billion in 2024 at the ceiling price equivalent, the metric HRSA uses. Industry trackers estimate the list-price-equivalent total at more than $124 billion in 2023. Congress never voted to expand either number.

The four players you need to know to follow every 340B headline: pharmaceutical manufacturers, covered entities, contract pharmacies, and HRSA. Three of them are at war with each other. The fourth has issued exactly one binding regulation in three decades.

The four-phase escalation. From the 2022 contract pharmacy crackdown by AbbVie, Sanofi, Eli Lilly, and Genentech, to the December 2025 Maine ruling that stopped HRSA’s rebate pilot cold.

The next move by HHS Secretary Robert F. Kennedy Jr. and CMS Administrator Mehmet Oz determines whether 340B remains in its current form, is rebuilt as a rebate, or is folded into Medicare entirely.

Glossary at the bottom of today’s article.

THE 1992 ORIGIN STORY

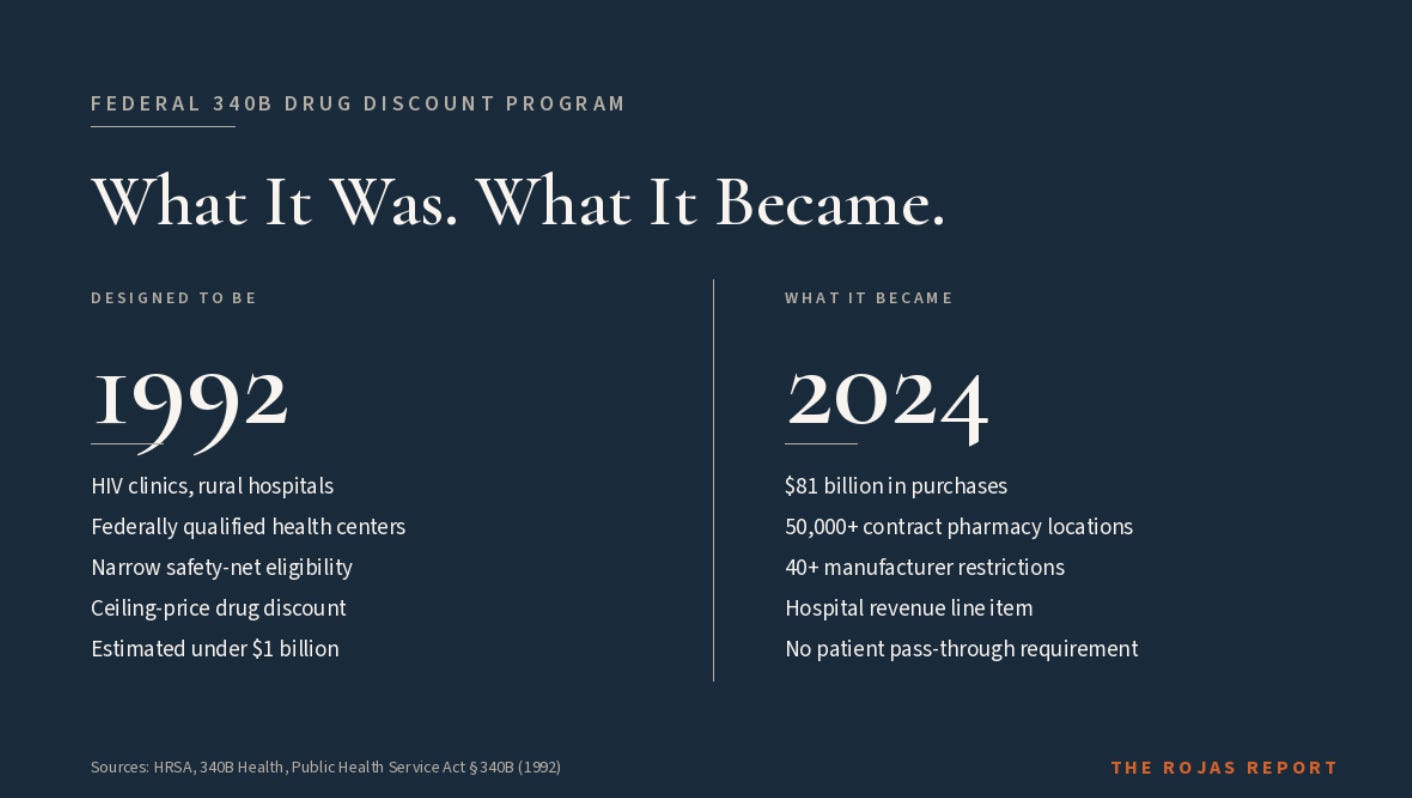

There is an $81 billion economy built on a paragraph almost nobody has read. That paragraph is Section 340B of the Public Health Service Act, passed in 1992.

It was tucked into the Veterans Health Care Act, signed by George H.W. Bush, and almost nobody noticed. The deal was simple. If a pharmaceutical manufacturer wanted Medicaid to cover its drugs, it also had to offer those drugs at steep discounts to a defined list of “covered entities.” That list was narrow. HIV clinics under the Ryan White program. Federally Qualified Health Centers. Disproportionate Share Hospitals serving large numbers of Medicaid and low-income Medicare patients. Tuberculosis clinics. Family planning clinics.

The rural hospital categories most readers associate with 340B today were not in the 1992 statute. Critical Access Hospitals. Sole Community Hospitals. Rural Referral Centers. Free-standing cancer hospitals. Congress added all of them 18 years later, in the Affordable Care Act of 2010. That single expansion is one of the structural reasons the program reached $81 billion.

The logic was straightforward. Safety-net institutions were drowning in the cost of outpatient drugs. Congress wanted to “stretch scarce federal resources as far as possible, reaching more eligible patients and providing more comprehensive services.” Those are the actual words from the original legislative report.

Now read what is missing from that sentence.

There is no mandate that the savings get passed to the patient.

There is no mandate requiring the savings to be returned to the program that generated them.There is no requirement that the entity be non-profit.

There is no cap on what a hospital can do with the money.

There is no public reporting requirement on how the savings get spent.

That is the quiet part out loud. The federal program designed to subsidize care for low-income patients does not require the subsidy to reach those patients. Read that sentence again. The federal program designed to subsidize care for low-income patients does not require the subsidy to reach those patients.

That gap is what built the $81 billion economy.

This is not a story about a drug discount. This is a story about the most leveraged subsidy in American healthcare, owned by whoever learned to access it first.

No one is coming to save independent medicine. So we’re saving each other. 60,000+ physicians. One signal. Subscribe at Read.RojasReport.Com/Subscribe

HOW THE DISCOUNT WORKS

The mechanic is simple.

The economics are not.

A drug manufacturer sets a list price. Call it $1,000 per vial. Under 340B, the manufacturer is required to offer that drug to a covered entity at a “ceiling price” calculated by a federal formula. The formula is based on the Medicaid Best Price and the Average Manufacturer Price, with an inflation adjustment. The ceiling price is often a fraction of the list price. Sometimes it is literally one cent. That is called “penny pricing,” and it triggers when a manufacturer raises a drug’s price faster than inflation.

The covered entity buys the drug at the ceiling price. Then it dispenses the drug to its patients. The covered entity bills the patient’s insurance, including Medicare and commercial insurance, at the patient’s full negotiated rate. The spread between what the entity paid and what insurance reimburses is the 340B margin.

That margin is the entire economic engine of the program.

For a Critical Access Hospital in rural Kentucky, that margin keeps the lights on. For an FQHC in inner-city Detroit, that margin pays for case managers and dental clinics. For a billion-dollar academic medical center in a wealthy suburb, that margin is a revenue line on the income statement.

The statute does not distinguish between those three. They are all “covered entities.”

If you have ever been billed at the full sticker price for a drug your hospital bought for one cent, you have just lived inside the 340B program.

You did not know it.

Now you do.

Is it appropriate for a billion-dollar academic medical center, with no statutory obligation to publicly report how it spends the money, to claim the same ceiling-price discount on a $15,000 cancer drug as a Critical Access Hospital that loses money on every patient it admits? Federal law says yes. Three decades of growth say nobody is checking.

THE FOUR PLAYERS

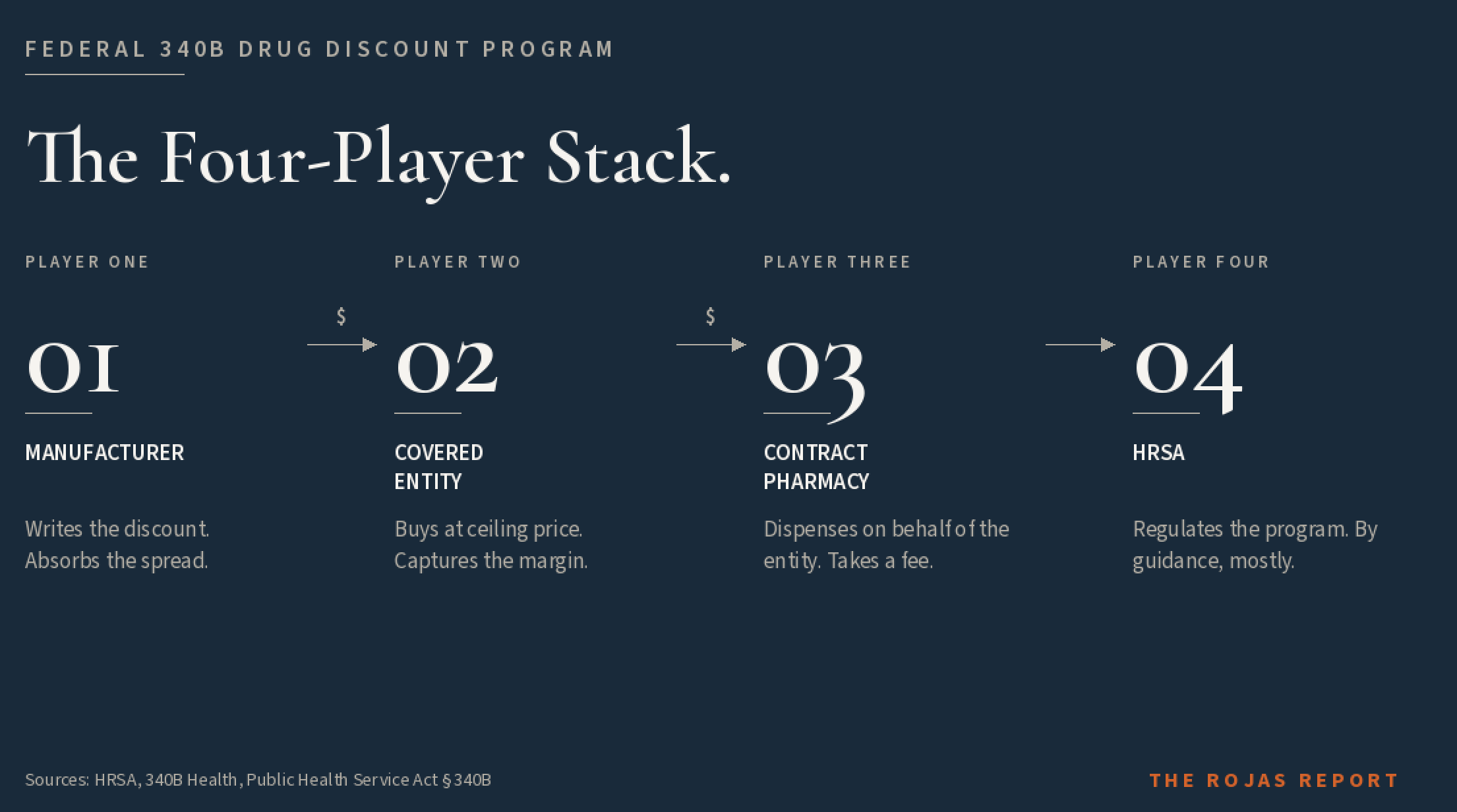

Every 340B headline you read involves four parties. Get them straight, and the news stops being confusing.

Pharmaceutical Manufacturers. The companies that make the drugs have to offer the discount. AbbVie. Sanofi. Eli Lilly. Genentech. Novartis. AstraZeneca. Johnson & Johnson. They are the ones writing the checks, and after a decade of program growth, they are the ones leading the counter-offensive. PhRMA is their trade association. PhRMA is also the entity that filed and lost the Supreme Court appeal of Arkansas’s contract pharmacy law.

Covered Entities. Hospitals, FQHCs, Ryan White HIV clinics, and other safety-net institutions are eligible to purchase drugs at the ceiling price. There are roughly 50,000 covered entity sites in the country, depending on how you count. The largest concentration is Disproportionate Share Hospitals, which account for the lion’s share of program spend. The American Hospital Association is the largest organized voice on the covered-entity side. America’s Essential Hospitals represents the most safety-net-dependent slice of the membership.

Contract Pharmacies. This is the player who detonated the program. In 1996, HRSA issued guidance allowing covered entities to contract with one outside pharmacy to dispense 340B drugs on their behalf. In 2010, HRSA expanded that guidance to allow unlimited contract pharmacy arrangements. The result is what you would expect. Walgreens, CVS, and Walmart became the largest 340B pharmacy networks in America. A rural hospital in West Virginia could now claim 340B savings on a prescription dispensed at a CVS in suburban Cleveland.

HRSA and the Office of Pharmacy Affairs. The Health Resources and Services Administration is the HHS agency that runs 340B. The Office of Pharmacy Affairs (OPA) is the HRSA unit responsible for enforcement. HRSA has issued exactly one binding regulation in the program’s three-decade history. Almost every operating rule comes from non-binding “guidance.” That fact will matter a lot by the time this article is over.

You did not know the names of any of these contract pharmacy operators 60 seconds ago. Now you do.

Everyone in healthcare has an opinion.

Very few have receipts.

This is where the receipts live.

Subscribe to The Rojas Report.

THE GROWTH CURVE

Here is the number that broke the program.

In 2016, a total of 340B drug purchases were roughly $8 billion. By 2024, they hit $81 billion. That is a 10x expansion in eight years. No federal healthcare program in modern memory has grown that fast without congressional action.

Year by year, ceiling-price equivalent purchases:

A note on the two numbers in circulation.

Readers will see both $81 billion and $124 billion attached to the 340B program. Both are real.

They measure different things.

The $81 billion figure is the program’s ceiling-price equivalent purchase total. It is the cash that actually moved through covered entities at 340B prices in 2024. This is the number HRSA and most industry analysts use when reporting “340B drug purchases.”

The $124 billion figure is the program’s WAC (wholesale acquisition cost). It estimates what those same purchases would have cost at full list price before the 340B discount was applied. Drug Channels Institute and Berkeley Research Group typically publish this number to illustrate the size of the discount itself rather than the cash that changed hands. Their most recent published WAC-equivalent figure for the program crossed $124 billion in 2023. [VERIFY: Drug Channels Institute and Berkeley Research Group source citations and most recent published figures]

Same program. Two metrics. The $124 billion answers “how much would these drugs have cost at full price?” The $81 billion answers “how much actually moved through the program?” The gap between them is the discount itself, which is the point of the program.

When this series quotes a 340B program-size number without qualification, the figure is ceiling-price equivalent. When the WAC-equivalent figure is the relevant frame, it is labeled.

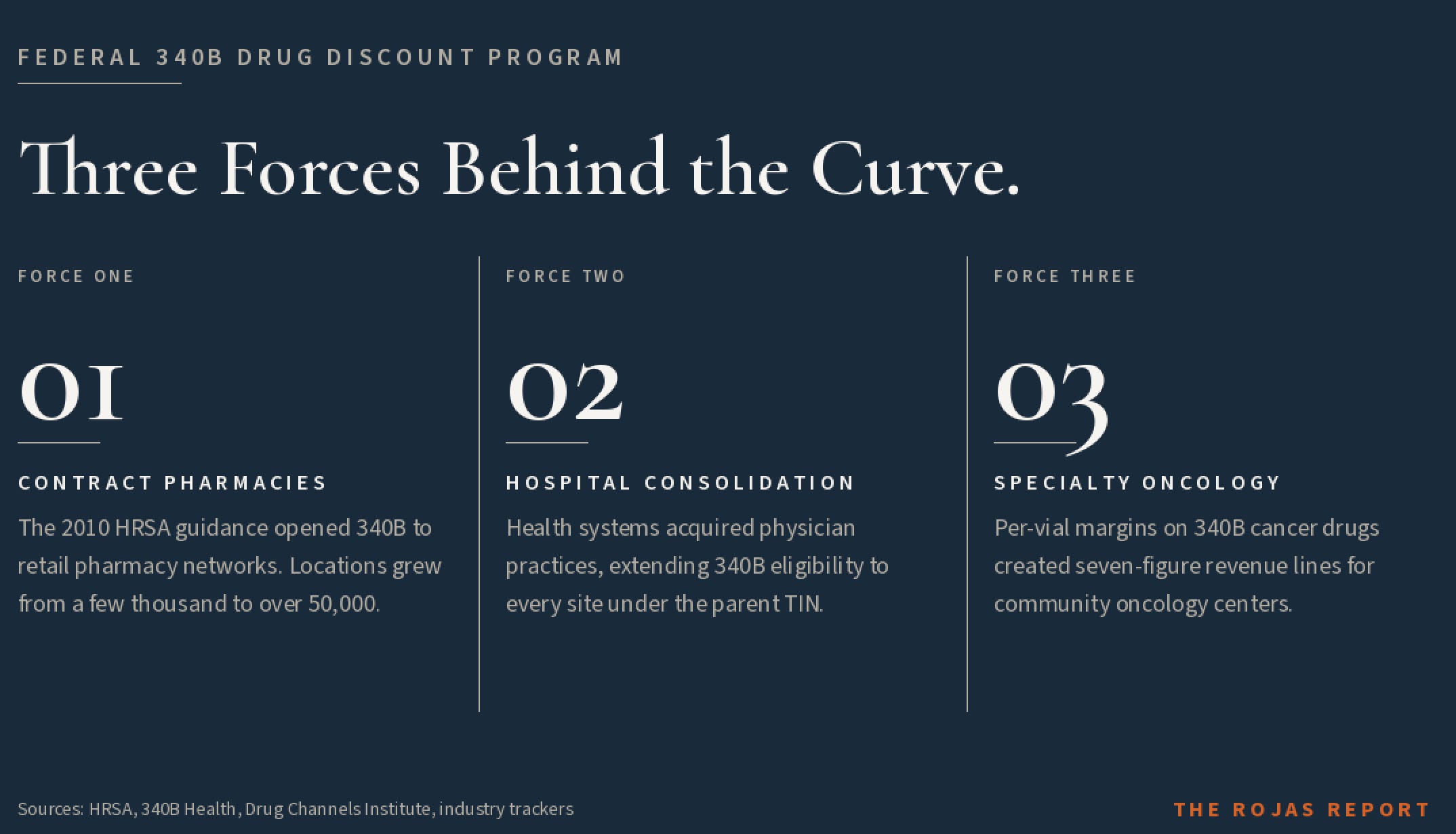

Three forces drove that curve.

The first is contract pharmacy expansion. The 2010 HRSA guidance turned 340B from a hospital-pharmacy program into a national retail-pharmacy program. The number of contract pharmacy locations grew from a few thousand to tens of thousands.

The second is hospital consolidation. As health systems acquired physician practices and outpatient clinics, they extended 340B eligibility to every site under the parent’s TIN. A drug administered in a private oncology office became a 340B drug the day the practice was acquired.

The third is the cancer drug economy. Specialty oncology drugs went from rare to routine, and the per-vial margins on 340B oncology agents created seven-figure annual revenue lines for community cancer centers. Pharmaceutical manufacturers watched their fastest-growing product lines get repriced at fractions of the list price, and they stopped pretending the program was still about HIV clinics.

The system is not broken. It is working exactly as the 1992 statute permits, just not for the reason the 1992 statute was written.

THE FOUR-PHASE ESCALATION

The 2022-2026 timeline is the part nobody outside healthcare consulting can keep straight. Here is the spine.

Phase 1: The Contract Pharmacy Crackdown (2022-2024). Starting in 2020 and accelerating through 2024, more than 40 pharmaceutical manufacturers unilaterally restricted 340B pricing at contract pharmacies. AbbVie, Sanofi, Eli Lilly, Genentech, Novartis, and AstraZeneca led the charge.

The mechanism was simple. Manufacturers began demanding claim-level data via third-party platforms such as 340B ESP and Kalderos Truzo.

No data, no discount. The covered entities sued. HRSA issued violation letters.

The cases spread across federal circuits. A localized dispute escalated into an industry-wide embargo, fundamentally disrupting the traditional 340B supply chain.

Phase 2: The State Legislative Counter-Offensive (2024-2025). With Congress paralyzed, state legislatures stepped in. Arkansas went first, becoming the first state to enforce a contract pharmacy protection law. AstraZeneca was the first manufacturer it went after. Louisiana, Mississippi, Minnesota, Maryland, West Virginia, Nebraska, Kansas, Missouri, Colorado, Utah, Ohio, Oregon, North Dakota, Vermont, Maine, Rhode Island, Hawaii, and more followed.

The Supreme Court declined to hear PhRMA’s appeal of the Arkansas case. The Fifth Circuit upheld Louisiana’s law. The Eighth Circuit upheld Arkansas’s. Federal district court injunctions blocked enforcement in West Virginia and Oklahoma.

The result: 340B is no longer a unified federal program.

It is a 50-state mosaic of conflicting compliance mandates.

Phase 3: The Rebate Revolution (2025). In July 2025, AbbVie executives walked into the Office of Management and Budget and pitched a structural rewrite. Stop the upfront discount. Make covered entities pay the full list price. Force them to submit claim-level data through a clearinghouse. Pay them back as a rebate after the data clears. AbbVie called it a “program integrity measure.”

The American Hospital Association estimated the compliance cost for 340 B hospitals at over $400 million per year in September 2025 and revised that estimate to over $1 billion in April 2026. HRSA opened a Request for Information. More than 5,500 public comments came in.

Of the 5,500 comments, roughly 1,100 of them were identical, traced to a template circulated by Patients Rising, a pharma-funded patient advocacy group. The 340B Report exposed it.

Patients Rising shut the campaign down.

That is the quiet part out loud.

A trade association funded a patient-advocacy group to manufacture the appearance of grassroots support for a rule change that would transfer hundreds of millions of dollars in working capital from hospitals to manufacturers.

The advocacy stopped within days of the exposure.

The rule change did not.

Phase 4: The Maine Stay and the 2026 Realignment (December 2025-Present). On December 29, 2025, the U.S. District Court for the District of Maine issued a preliminary injunction halting HRSA’s rebate pilot. On January 7, 2026, the First Circuit denied the government’s request for a stay. On January 20, 2026, the government dropped its appeal. On February 5, 2026, HHS told the court it would scrap the current pilot. On February 17, 2026, HRSA opened a fresh Request for Information on the same model.

In April 2026, HHS Secretary Robert F. Kennedy Jr. testified before a Senate subcommittee that he was “unaware of the current status” of the rebate model and agreed to brief the Senate’s bipartisan “Gang of Six.”

The administration’s FY 2027 budget proposes integrating the Office of Pharmacy Affairs into CMS Program Management, placing CMS Administrator Mehmet Oz in charge of the rewrite.

That is where we are this morning.

WHY THIS MATTERS

If you are a physician, 340B is why your employer-hospital can afford to keep your oncology clinic open in a market where reimbursement does not cover the cost of chemotherapy. It is also the reason your employer-hospital can pay an executive an eight-figure salary who has never seen a patient. The 1992 statute does not distinguish between those two uses. Read that sentence again. The statute that lets your hospital subsidize your clinic is the same statute that lets your hospital subsidize the executive who closed the rural site down the road.

If you are a lawmaker, 340B is the program your constituents do not know they depend on, your state law may or may not protect, and your federal counterparts cannot agree on how to fix it. The federal courts have split. The Supreme Court declined to step in. The Fifth and Eighth Circuits upheld state laws. The Fourth and Tenth Circuits have not. Your district falls under one of those circuits. You probably do not know which one applies to your hospital. Your hospital does.

If you are a patient, 340B is invisible to you.

Your health benefits are still billed at full price.

Your copay is still your copay.

The discount happens in the back room, between the manufacturer and the hospital, and you never see the money.Whether your hospital uses that money to subsidize your cancer care or to build a parking garage is a decision the statute does not require anyone to disclose.

That is the design problem.

That is the political problem.

That is the rest of the series.

WHAT BREAKS NEXT

The Maine ruling pauses the rebate model. It does not resolve it. AbbVie, Sanofi, Eli Lilly, and the rest are not done. Patients Rising is regrouping. The state laws are still being challenged. The IRA’s Maximum Fair Price program is colliding with 340B ceiling prices in Q1 2026, and ceiling prices for negotiated drugs are compressing fast. Penny pricing is disappearing.

Three forces decide what 340B looks like 18 months from now. The federal courts. The state legislatures. The CMS reorganization that turns Mehmet Oz into the program’s de facto administrator.

Is it appropriate for the federal agency that runs Medicare and Medicaid to also run an $81 billion drug discount program, with the same Administrator who is currently rewriting Medicare’s drug negotiation playbook, with no congressional vote, with no public comment period on the transfer itself, and with a budget proposal that has not yet been enacted? That is the question every covered entity in the country is asking this morning. It is not the question being answered.

This is the Primer. The 340B Files start in Part 1.

Part 1: The Rebate Revolution. I walk through the AbbVie OMB pitch line by line. The names in the room. The legal theory. The American Hospital Association’s revised $1 billion compliance bill. And the part of the AbbVie framework signaled in the OMB deck itself: an “operational patient definition” that could narrow who qualifies for 340B pricing.

Part 2: The AstroTurf Operation. How 1,100 identical comments from a pharma-funded patient group nearly hijacked the federal record. Who funds Patients Rising? Why did the campaign stop within days of exposure?

Part 3: The Maine Stay and the State Counter-Offensive. The legal landscape after Loper Bright. The 50-state map. The two circuits that upheld state laws. The two that have not.

Part 4: The IRA Collision. What happens when the Inflation Reduction Act’s negotiated prices land on top of 340B ceiling prices, and which hospitals do not survive the math?

You did not know any of this 20 minutes ago. Now you do.

-Rojas out.

GLOSSARY

340B Program: A federal drug pricing program created by Section 340B of the Public Health Service Act in 1992. Requires drug manufacturers participating in Medicaid to sell outpatient drugs at a ceiling price to qualified safety-net institutions called "covered entities." Hit $81 billion in drug purchases in 2024.

Average Manufacturer Price (AMP): The average price paid to a manufacturer by wholesalers for drugs distributed to retail pharmacies. One of the inputs to the 340B ceiling price formula.

Ceiling Price: The maximum price a manufacturer can charge a covered entity for a 340B-eligible drug. Calculated from AMP and Medicaid Best Price.

Ceiling-Price Equivalent: Metric used by HRSA and most industry analysts to report 340B program size. Measures the cash that actually moved through covered entities at 340B prices. Anchored at $81 billion in 2024.

CMS (Centers for Medicare & Medicaid Services): The HHS agency that runs Medicare and Medicaid. The FY 2027 budget proposal would move 340B oversight from HRSA to CMS, putting CMS Administrator Mehmet Oz in charge.

Contract Pharmacy: A retail pharmacy that dispenses 340B drugs on behalf of a covered entity under a contract. Walgreens, CVS, and Walmart operate the largest 340B contract pharmacy networks in the country. Authorized in 1996 HRSA guidance, expanded to unlimited arrangements in 2010 HRSA guidance.

Covered Entity: A safety-net healthcare institution eligible to participate in 340B. Original 1992 categories included Disproportionate Share Hospitals, Federally Qualified Health Centers, Ryan White HIV clinics, tuberculosis clinics, and family planning clinics. The Affordable Care Act of 2010 added Critical Access Hospitals, Sole Community Hospitals, Rural Referral Centers, and free-standing cancer hospitals. Roughly 50,000 sites nationally.

Disproportionate Share Hospital (DSH): A hospital serving a high percentage of low-income Medicaid and Medicare patients. The largest 340B covered-entity category by program spend.

Duplicate Discount: A statutorily prohibited situation where a manufacturer pays both a 340B discount and a Medicaid (or Medicare inflation, or Maximum Fair Price) rebate on the same drug claim. The core program-integrity argument advanced by manufacturers in favor of a rebate model.

Federally Qualified Health Center (FQHC): A community health center receiving HRSA funding to serve underserved populations. A core 340B covered-entity category.

HRSA (Health Resources and Services Administration): The HHS agency that currently administers 340B through its Office of Pharmacy Affairs. Has issued one binding regulation in the program’s three-decade history.

IRA (Inflation Reduction Act): 2022 federal law authorizing Medicare drug price negotiation, creating the Maximum Fair Price for covered drugs and an inflation rebate that affects 340B ceiling-price calculations.

Loper Bright Enterprises v. Raimondo: 2024 Supreme Court decision overturning Chevron v. NRDC. Eliminated the doctrine that courts defer to agency interpretations of ambiguous statutes. Cited as the legal backdrop for hospital challenges to HRSA’s rebate pilot.

Mehmet Oz: CMS Administrator under the second Trump administration. Confirmed along party lines. Would become the de facto administrator of 340B if the FY 2027 budget proposal moving the program from HRSA to CMS is enacted.

Maximum Fair Price (MFP): The Medicare-negotiated price for selected drugs under the IRA. First MFPs took effect January 1, 2026, on Eliquis, Jardiance, Imbruvica, Januvia, and other negotiated drugs. Overlaps with 340B ceiling prices on the same products.

Office of Management and Budget (OMB): The White House budget and regulatory review office. AbbVie executives pitched the rebate model framework here on July 1, 2025.

Office of Pharmacy Affairs (OPA): The unit inside HRSA responsible for 340B program enforcement.

Operational Patient Definition: Phrase from the AbbVie OMB deck signaling a structural narrowing of who qualifies as a 340B-eligible patient. The 340B statute does not define “patient.” HRSA’s 1996 guidance defined it broadly. The size of any cut implied by AbbVie’s framing is not clear from the public record.

Patients Rising: A patient advocacy group identified by the 340B Report as the source of duplicate-template comments submitted during HRSA’s 340B Rebate RFI process. Pharma-funded.

Penny Pricing: A 340B mechanism that drops the ceiling price of a drug to one cent when the manufacturer raises the drug’s price faster than inflation. Disappearing fast under IRA-era negotiated pricing.

PhRMA: Pharmaceutical Research and Manufacturers of America. The trade association representing the manufacturer side of the 340B fight. Filed and lost the Supreme Court appeal of Arkansas’s contract pharmacy law.

Rebate Model: The proposed structural rewrite of 340B in which covered entities pay full list price upfront and receive the discount as a post-purchase rebate after submitting claim-level data through a clearinghouse. Pitched by AbbVie at OMB on July 1, 2025. Halted by federal court in Maine on December 29, 2025. Reopened by HRSA RFI on February 17, 2026.

Request for Information (RFI): A formal federal process for collecting public input. HRSA’s 2025 340B Rebate RFI received more than 5,500 comments, roughly 1,100 of which were identical templates from Patients Rising.

Robert F. Kennedy Jr.: HHS Secretary under the second Trump administration. Testified before a Senate subcommittee in April 2026 that he was “unaware of the current status” of the rebate model and agreed to brief the bipartisan “Gang of Six” Senate working group.

Ryan White HIV/AIDS Program: Federal HIV/AIDS funding program. Ryan White clinics are 340B covered entities and were among the original intended beneficiaries of the 1992 statute.

Third Party Administrator (TPA): A vendor that manages 340B operations for a covered entity, including inventory tracking and split-billing software. 340B ESP and Kalderos Truzo are two of the platforms manufacturers have demanded data through.

WAC-Equivalent (Wholesale Acquisition Cost-Equivalent): Alternative metric for 340B program size used by industry trackers including Drug Channels Institute and Berkeley Research Group. Measures the list-price value of the same drug volume before the 340B discount was applied. Crossed $124 billion in 2023.

SOURCES

AbbVie, Inc. 340B Rebate Guidance OMB Briefing Deck. Filed in connection with the July 1, 2025 OIRA meeting under RIN 0906-ZA14. Includes the phrases “manufacturers lack timely claim-level data to prevent duplicate discounts and ensure compliance,” “A rebate model is a straightforward solution,” and the reference to “implement an operational patient definition.”

340B Report. “AHA Urges HRSA to Delay 340B Rebate Pilot, Argues Hospitals Face at Least $400M in Annual Costs.” September 2025.

American Hospital Association. Letter to HRSA on the 340B Rebate Model. September 30, 2025. Cites per-hospital compliance costs of $150,000 to over $500,000, a conservative aggregate above $400 million, and the “interest-free loans” framing.

American Hospital Association. April 2026 court filing. Revised compliance estimate above $1 billion annually; UC Health estimate of approximately $120 million in additional drug acquisition costs (~$10 million per month) for 2025 pilot drugs.

340B Report. “HRSA Proposes 340B Rebate Model Pilot for Narrow Set of Drugs Under Strict Conditions.” July 2025.

Federal Register. Pilot notice describing the 340B Rebate Model Pilot Program. August 7, 2025.

340B Report. “Maine Federal Judge Halts 340B Rebate Pilot Nationwide.” December 2025.

340B Report. “1st Circuit Declines HHS’ Bid to Immediately Pause Order Blocking 340B Rebate Pilot, But Signals Plans for Quick Ruling.” December 2025.

340B Report. “1st Circuit Grants HHS’ Motion to Voluntarily Dismiss 340B Rebate Pilot Appeal.” January 2026.

340B Report. “HHS Formally Withdraws 340B Rebate Pilot, Agrees to New Guardrails for Any Future Rebate Efforts.” February 2026.

340B Report. “HRSA Releases Request for Information Seeking Comments on Whether to Move Forward with 340B Rebate Pilot.” February 2026.

340B Report. “Trump’s FY 27 HHS Budget Again Looks to Move 340B from HRSA to CMS, Calls for Major OPA Funding Increase.” April 2026.

340B Report. April 21, 2026. Coverage of HHS Secretary Robert F. Kennedy Jr. Senate subcommittee testimony stating he was “unaware of the current status” of the 340B rebate model.

Loper Bright Enterprises v. Raimondo, 603 U.S. 369 (2024). For 340B impact analysis see 340B Report, “The Demise of Chevron Deference: What Does It Mean for the 340B Program?” November 2024.

Health Resources and Services Administration. 1996 Patient Definition Guidance. Federal Register.

Association of American Medical Colleges. 2024 statement on legislative proposals to define “patient” in 340B statute.

LEGAL DISCLAIMER

This report is based entirely on publicly available federal records, court filings, and legislative materials, supplemented by an industry strategic briefing reviewed by The Rojas Report. It identifies structural patterns and anomalies in the 340B drug pricing program. No allegation of fraud, wrongdoing, or criminal activity is made against any individual or entity. All conclusions are limited to what the data supports, and limitations are stated explicitly.

Methodology note: 340B drug purchase totals are reported as ceiling-price equivalent purchases per HRSA and industry tracker convention, anchored at $81 billion in 2024. Alternative methodologies (WAC-equivalent, list-price-equivalent) measure the notional value of the underlying drugs at full price and have placed the program above $124 billion in 2023. Both figures are real. They measure different things, as explained in “The Growth Curve” section.