They Called It Patient Protection. Physicians Are Still Waiting to Get Paid.

The No Surprises Act created a dispute resolution system built on a projection that was wrong by a factor of 100. The physicians treating emergency patients absorbed the consequences.

Your emergency physician doesn’t get to decide whether to treat you.

Federal law requires it.

The same law that forces treatment controls payment.

It promises 30 days.

It delivers 150.

IN TODAY’S ARTICLE:

How the No Surprises Act created a legal obligation to treat and a bureaucratic obstacle to payment

The volume problem: 489,000 disputes in the first 14 months alone

Why insurers’ own QPA calculation anchors arbitration outcomes downward

Who benefits from 150-day payment delays, and how the math works

Glossary at the bottom of today’s article.

THE SETUP

December 27, 2020. Congress passed the No Surprises Act.

The deal was simple.

Patients would no longer receive unexpected bills from out-of-network physicians. When an insurer and a physician disagreed on payment, they would submit to federal arbitration. An independent arbitrator would decide.

The process would take 30 days.

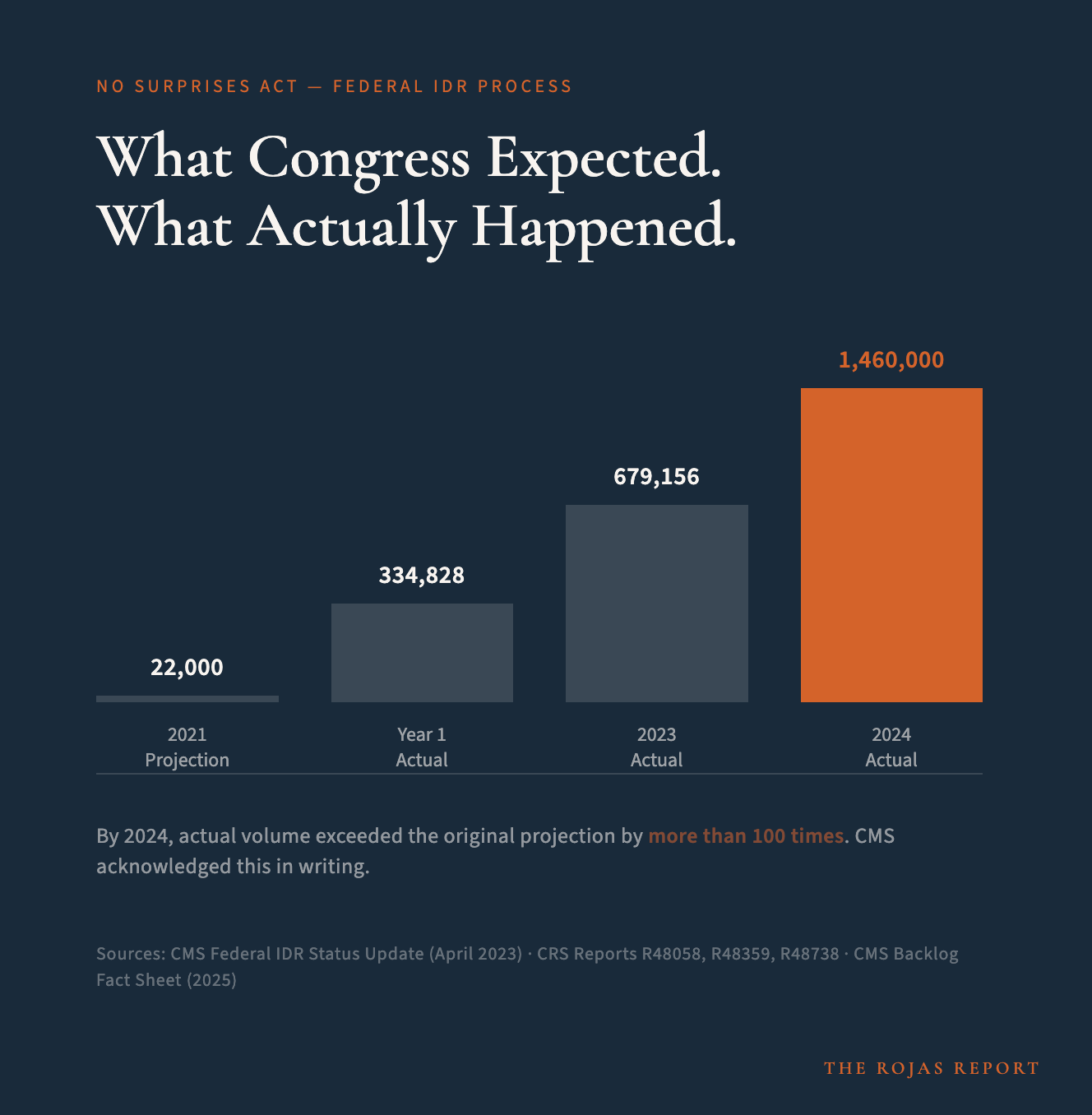

Congress projected 22,000 disputes a year.

In the 14 months between April 2022 and June 2023, 489,000 disputes.

By 2024: 1.46 million.

By 2025, CMS put it in writing. Annual volume now exceeds 100 times the original projection.

The deal was simple. The numbers behind it were not.

TEXAS TOLD THEM

Before the No Surprises Act passed, two states had already built surprise-billing dispute-resolution systems: New York and Texas.

New York’s law used an independent nonprofit database called FAIR Health as the payment benchmark. It anchored insurer payments at a fixed percentage of the usual and customary rate. Emergency billing disputes in New York’s system collapsed. Not reduced. Collapsed.

Texas used arbitration, like the federal model. In 2020, the first full year Texas law was in effect, the Texas Department of Insurance received 44,910 arbitration requests and 3,855 mediation requests. Total: 48,765 dispute resolution requests. For a state where the law covered about 20% of Texans, per the Texas Department of Insurance’s own report.

The federal departments building the IDR projections had access to Texas data.

They used New York.

The data used to predict the scale were available. It was not used.

Why? The CMS methodology divided New York’s 2018 insured population of 12.3 million by the national commercially insured population of 183 million. They calculated that New York represented 5.7% of the country. They took New York’s approximately 1,000 annual resolved IDR disputes and extrapolated: the federal system would see roughly 17,435 disputes per year.

Texas, covering 20% of Texans and producing nearly 50,000 disputes in its first year, would have projected several hundred thousand annual federal disputes. Possibly over a million.

The GAO later found that four industry groups told them the departments failed to account for the experience of states with similar processes when making the estimate.

The GAO found that the federal departments underestimated dispute volume by a factor of 14 in the first year alone. By 2024, the actual-to-projected ratio exceeded 100.

WHAT 30 DAYS ACTUALLY MEANS

The statute is clear. The IDR process resolves within 30 business days of initiation.

The GAO examined what actually happened.

Average resolution time: 150 days.

Longest documented delay: 268 days.

The 30-day mandatory negotiation period between the insurer and the physician occurs before the IDR process even begins. Add the wait before arbitration even starts. A physician who treats an emergency patient and cannot agree on payment with the insurer may wait for resolution for the better part of a year.

The physician delivered the care. The patient received the care. The bill was submitted. The dispute was filed.

And then: nothing, for months.

Texas handed the government a warning.

The U.S. government used different data.

Someone made that choice.

100,000+ physicians are reading the receipts.

You can too. Subscribe