TRENDS IN HEALTH INSURANCE:

Premiums and Deducitbles 2000 to 2022.

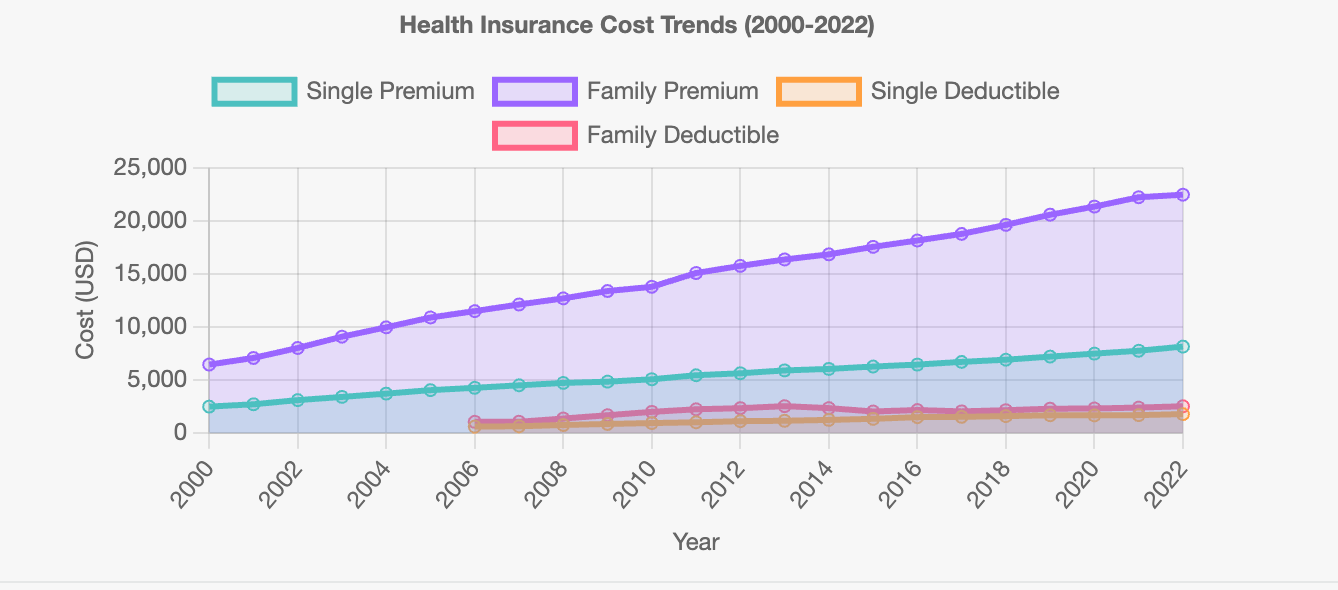

Over the past two decades, the costs associated with health insurance premiums and deductibles have significantly increased. This data examines the trends in single— and family premiums and deductibles from 2000 to 2022.

Single Premiums

In 2000, the average annual single premium was $2,471. By 2022, it had more than tripled, reaching $8,133. This represents a substantial increase in the financial burden on individuals purchasing health insurance.

Family Premiums

Family premiums have also seen a dramatic rise. In 2000, the average annual family premium was $6,438. This increased to $22,463 by 2022, an almost four-fold increase. The rising costs reflect the growing expenses in the healthcare system and the increasing complexity and comprehensiveness of health insurance plans.

Single Deductibles

Data for single deductibles begins in 2006. At that time, the average deductible was $584. By 2022, this had risen to $1,763. This increase indicates a trend towards higher out-of-pocket costs for individuals before insurance benefits kick in.

Family Deductibles

Family deductibles show a similar trend, starting at $1,034 in 2006 and rising to $2,504 in 2022. This doubling of deductibles over 16 years signals a shift in cost-sharing strategies within health insurance policies.

The data clearly shows a substantial increase in both premiums and deductibles for health insurance from 2000 to 2022. These rising expenses underscore the growing financial burden on individuals and families managing healthcare expenses. As healthcare expenses continue to increase, stakeholders must explore strategies to make health insurance more affordable and accessible, keeping in mind the significant impact on the lives of these individuals and families.

Click here for an interactive version of the chart:

https://puc.poecdn.net/preview.4e5292b5b09b607f0988.html

-Rojas out

Disclosure: My firm provides employee benefits, workers' compensation, and property and casualty consulting to medical professionals and healthcare companies.

Very interesting! Along the journey from 2000 to 2022, employers implemented employee cost sharing to create a "consumer" mindset among employees ...to keep premiums down. Complexity was increased in the name of keeping premiums down (complexity caused by situational decision making for narrow networks, ER visits, etc). The ACA increased the pool of insured people by millions so the risks could be spread out...which should keep premiums down. High deductible plans were introduced to keep premiums down. Health systems emerged to keep care costs down.

None of these has been effective across the population. During this time period, we also watched the baby boomers hit retirement age ...and care costs tend to correlate with age.

The healthy still pay for the sick (that's the way insurance works)...and there are entire industries specializing in the "weird and wonderful" to develop more costly solutions for the sickest of the sick.