Why the Biggest Buyer in Outpatient Surgery Just Became a Seller

Cheap money built the consolidators. Expensive money is taking them apart. The opening is yours.

Bain Capital offered $3.2 billion to take Surgery Partners private.

The board said no.

Then the company started selling off surgery centers.

That is not strength.

That is a machine running out of fuel.

In today’s article:

Why the largest shareholder in the biggest public surgery-center roll-up tried to buy the whole thing, and why the board refused

The pivot that gives the game away: a buyer turning seller to service its own debt

The number that broke the model was never the surgery center.

The open door this leaves for physicians who still own their buildings.

Glossary at the bottom of today’s article.

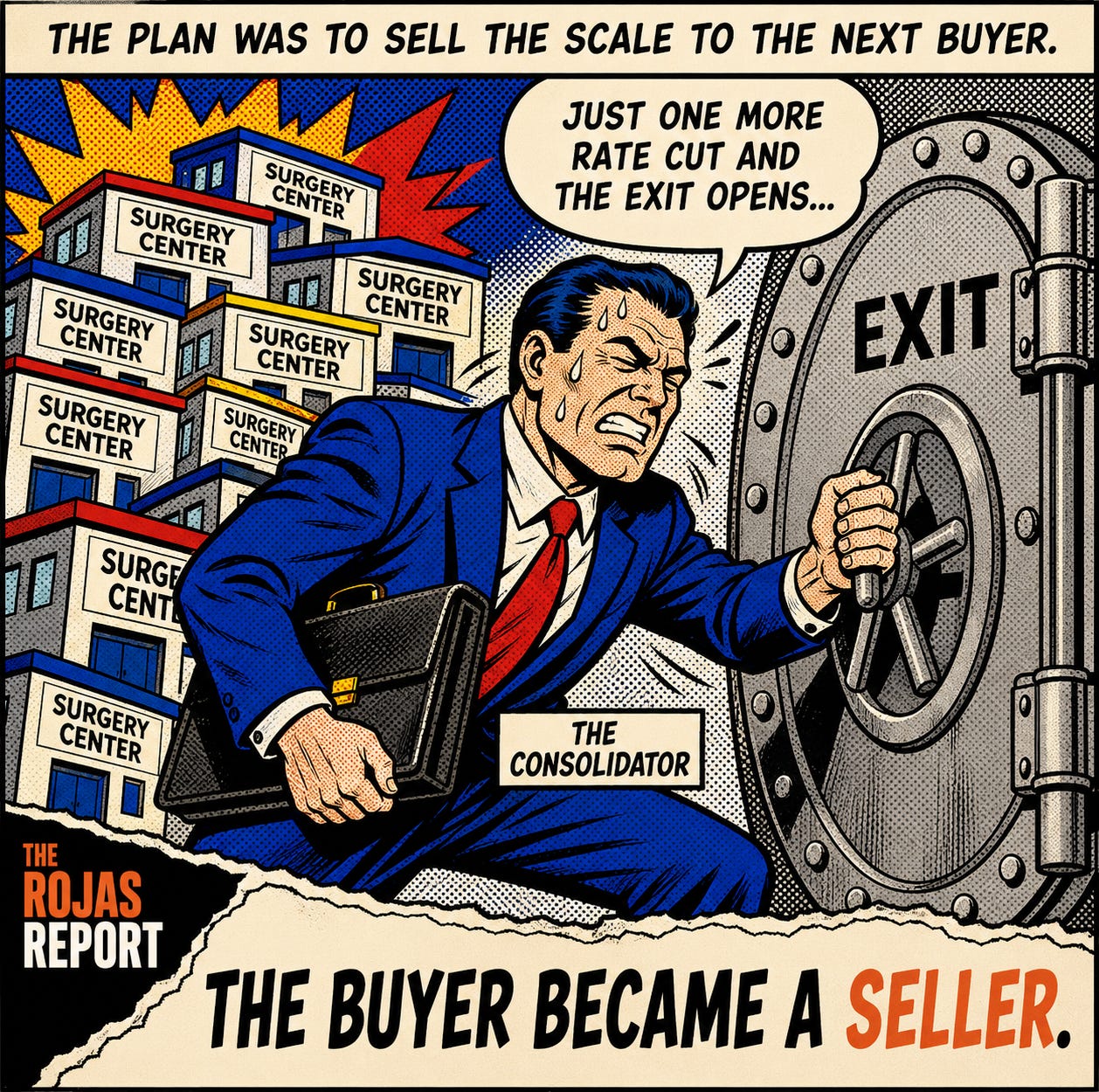

THE BUYER WHO BECAME A SELLER

In August 2017, Bain Capital bought control of Surgery Partners. It paid $502.7 million for a majority stake and folded in National Surgical Healthcare for another $760 million. The thesis was the one every physician has heard pitched across a steakhouse table. Buy the centers. Build the scale. Sell the scale to the next buyer at a higher multiple.

For a while it worked exactly as designed. Surgery Partners grew into more than 200 surgical facilities across 33 states, with roughly 4,600 affiliated physicians. It went public in 2015. By late 2022, it needed an $800 million equity raise to keep the engine running, and Bain wrote a $225 million check into that raise.

Then came the tell.

On January 28, 2025, Bain offered $25.75 a share to take Surgery Partners fully private. The bid valued the company at nearly $3.2 billion, about 12.7 times earnings, a 27 percent premium. The stock jumped 20 percent in a day. Bain already owned about 39 percent of the company. This was the largest shareholder trying to buy the rest.

On June 17, 2025, the independent committee said no. Its chairman, Brent Turner, cited the company’s growth and market position. CEO Eric Evans framed the rejection as a sign of confidence.

Watch what happened next, because the press release will not say it plainly. After walking away from the buyout, Surgery Partners pivoted to selling and partnering off facilities. The stated reason was to cut leverage and accelerate cash flow. The biggest buyer of Ambulatory Surgery Centers became a seller of them. To pay down its own debt.

That is the entire story in one move.

THE MATH THAT BROKE

The consolidators do not want this part said out loud. The roll-up never ran on surgery. It ran on cheap debt.

The model needs three things. Borrow cheaply. Buy centers below the price you can mark them at once they sit inside a bigger platform. Sell the platform to the next buyer before the music stops. Every link in that chain depends on money being cheap and exits being open.

Money got expensive. Exits closed.

The deal data shows the seizure. Private equity healthcare acquisitions fell from 1,114 in 2021 to 940 in 2022 to 788 in 2023, according to PitchBook. The buyers did not lose interest in medicine. They lost the financing that made the math work.

And when the deals did happen, they got smaller. Of 148 transactions involving outpatient care operators in 2024, 119 were add-on acquisitions. Seven were leveraged buyouts. The era of the headline mega-deal gave way to quiet tuck-ins, because a tuck-in does not need the same leverage or the same exit.

Now hold that against the demand side, because this is where the establishment narrative falls apart. Outpatient surgery is not slowing. CMS added 289 procedures to the ASC covered procedures list for 2026 and began a three-year elimination of the inpatient-only list, starting with 285 mostly musculoskeletal procedures. The ASC market grows 6 to 8 percent a year. Surgery Partners itself deployed $66 million in acquisitions in a single quarter of 2025 and added eight facilities.

So the surgery center is fine. The leverage stacked on top of it is not. The thing that broke was the capital structure, not the care.

Everyone in healthcare has a take on consolidation.

Almost no one has the deal terms.

This is where the deal terms live.

Subscribe.