Your Hospital’s Press Release Is a Story. Page One of the 990 Is a Confession.

The first page of the 990 replaces every press release the hospital ever wrote.

The first page of the 990 replaces every press release the hospital ever wrote.

$8.5 billion came in.

$7.7 billion went out.The remaining $860 million has no ribbon-cutting ceremony.

It has no press release.

It has a line number.

IN TODAY’S ARTICLE:

The three lines on page one that replace every press release: total revenue, total expenses, and the gap between them

Memorial Hermann’s FY2024 front page, read to the dollar.

Net assets: the wealth line that tells you how many years the “charity” could run on reserves alone

The five-minute front-page read you will run on your own hospital by tonight.

Glossary at the bottom of today’s article.

Module 0 taught you to check whether a 990 exists. Module 1 handed you the list of systems where it never will. Today you open one.

The document is long.

Core form plus schedules can run past a hundred pages for a big system. Ignore almost all of it. The front page carries the three numbers that matter, and the balance sheet in Part X carries the fourth. You can pull all four in five minutes, and by the end of this module you will.

THE ONE DOCUMENT NOT WRITTEN BY MARKETING

Every hospital system produces an annual report. Glossy paper. Smiling nurses. A letter from the CEO about community and courage. A communications team drafted it, a design agency polished it, and a general counsel approved it.

The same system produces a Form 990. No photographs. No mission statement in serif font. Just tables, and directly above the officer’s signature on page one, this sentence: “Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete.”

One document was written to persuade you. One was signed under penalty of perjury.

When they conflict, start with the one signed under penalty of perjury.

The annual report is written for patients, donors, employees, and the local press. Everyone evaluating the institution’s finances starts with the filing. You will too.

Today’s worked example is Memorial Hermann Health System in Houston.

EIN 74-1152597. Fourteen years of filings sit in public view, and every figure in this article comes from those filings. Pull the page yourself at ProPublica’s Nonprofit Explorer while you read. A full 990 filer, bucket one from Module 0.

FIRST, THE VOCABULARY LESSON

One correction before the numbers, because the entire industry depends on you never making it.

“Nonprofit” describes a tax status. It has never described a business result. Nothing in section 501(c)(3) of the tax code requires an organization to break even, run lean, or price at cost.

The statute requires that no private individual own the earnings, that the organization pursues an exempt purpose, and that it file this disclosure. That is the whole deal: no owners, in exchange for no taxes.

An institution can satisfy every word of that bargain while clearing a billion dollars a year. Many do. The vocabulary was designed in an era of church wards and county hospitals, and the industry has spent fifty years hiding a conglomerate behind it. The IRS itself prefers the plainer term: tax-exempt organization.

That is the honest name because it describes the privilege rather than implying a virtue, and it is the name this series will continue to use.

Keep that correction loaded. Every number below gets clearer with it.

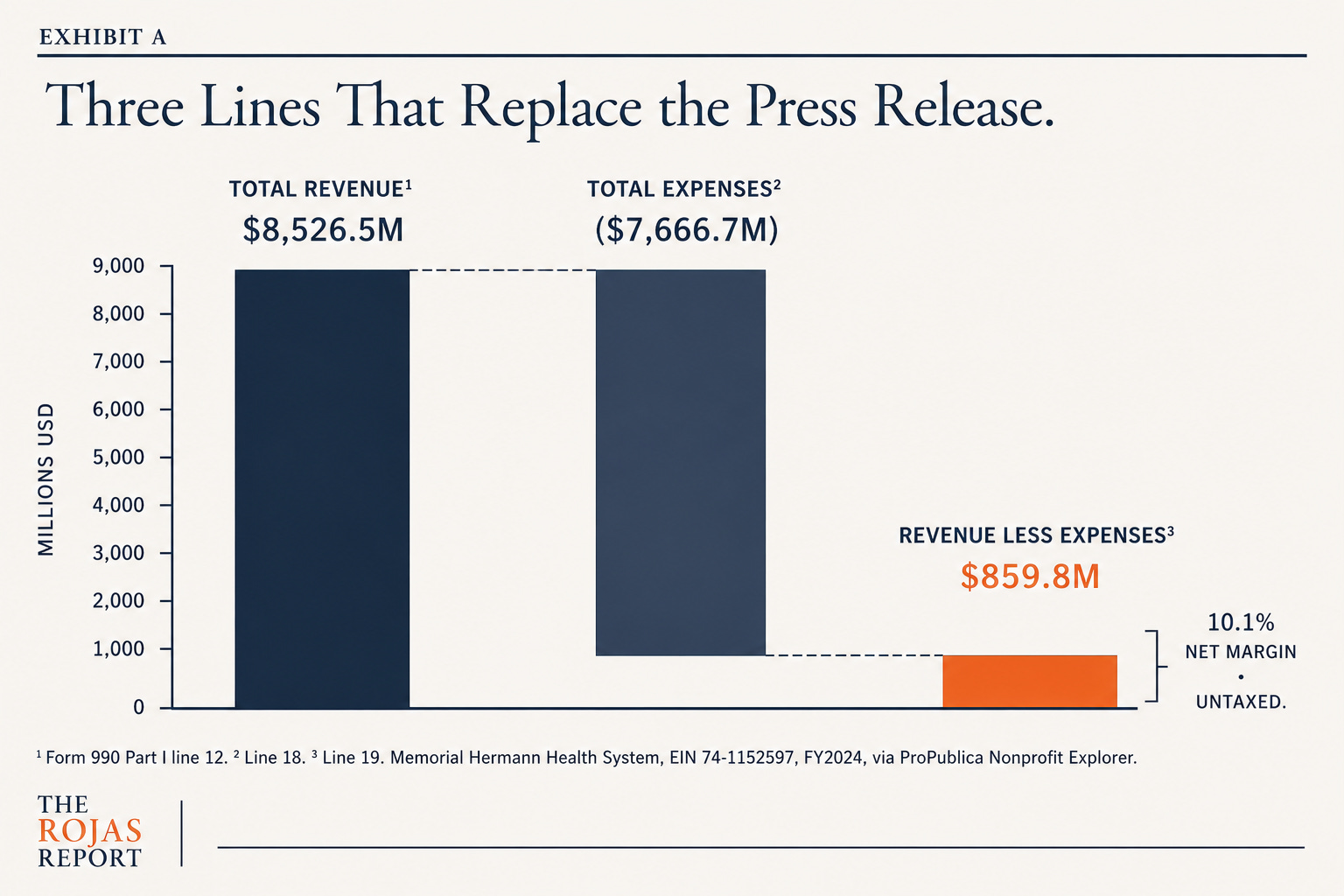

LINE ONE: TOTAL REVENUE

Part I, line 12. Everything that came in.

Memorial Hermann, fiscal year 2024: $8,526,519,854.

One health system. One metro. One year.

Program service revenue represented more than 94% of total revenue. Donations represented just 0.2%. Investment income alone exceeded $408 million.

Read those three lines together, and a quiet fact emerges. This charity is funded two-tenths of one percent by charity. Its investment portfolio earned nearly thirty times what its donors gave. The word “nonprofit” makes people picture a soup kitchen. The filing describes a multibillion-dollar healthcare conglomerate.

LINE TWO: TOTAL EXPENSES

Part I, line 18. Everything that went out.

Memorial Hermann, FY2024: $7,666,749,931.

Salaries and wages below the executive suite claimed $2,719,843,676 of that, 35.5% of all spending, which is the part of the institution that actually treats people. The rest covers supplies, drugs, interest, depreciation, and the general overhead of running what is functionally a mid-cap corporation with a chapel in the lobby.

One analyst’s note on that word depreciation: a real expense on paper, a non-cash expense in the bank account. The cash an institution generates in a year typically exceeds the surplus the front page admits to. Line 19 is the floor of the story, never the ceiling.

Most readers stop here.

Revenue big, expenses big, hospital big. Fine.

The lesson lives in the subtraction.

LINE THREE: THE LINE WITH NO PRESS RELEASE

Part I, line 19. Revenue less expenses.

Memorial Hermann, FY2024: $859,769,923.

Say it plainly: this nonprofit cleared $860 million in 12 months. That is $2.4 million a day, including weekends and holidays. Roughly $98,000 an hour, around the clock, all year.

A for-profit company calls that number profit, reports it to shareholders every quarter, and pays tax on it. A nonprofit hospital calls it “operating margin” or “revenue over expenses,” mentions it never, and pays tax on none of it.

The tax status changed the vocabulary.

The math stayed identical.

WHERE A SURPLUS GOES WHEN NOBODY OWNS IT

Here is the question the surplus forces. A for-profit’s earnings have a destination: dividends, buybacks, owners. A nonprofit has no owners. So where does $860 million go?

Three places, and only three.

Reserves. The surplus joins the investment portfolio, where it generates the $408 million in annual investment income you met on line one. Money making money, tax-free, forever.

Buildings. Towers, wings, imaging centers. Capacity in the zip codes with the payer mix the strategy team likes.

Acquisitions. Physician practices, surgery centers, competitors. The surplus is the war chest that funds consolidation, and consolidation feeds the next surplus. Module 5 of this series will show you the acquisition ledger on Schedule R, where every purchased practice appears as a new row.

Notice what all three have in common.

Every destination makes the institution bigger. None of them reduces your bill. Nothing on the front page suggests the surplus was returned to patients through lower prices. The money has nowhere to go but back into the machine.

Bond analysts read the filing first.

Rating agencies do too.

Starting today, so will you.You can keep learning your hospital’s finances from its marketing department. Or you can learn them from the document its officers sign under penalty of perjury.

Subscribe today.