Ohio Can Block Any Nonprofit Hospital Merger. There’s One $6.76 Billion Exception It Never Mentions.

Eight states can stop a hospital merger before it closes. Ohio is one. Watch where its authority ends.

There is a hospital in Columbus that collects $6.76 billion a year and pays no tax.

Every private system in Ohio answers to the Attorney General before it can merge or acquire.

This one does not.

The reason is one word buried in the statute.

IN TODAY’S ARTICLE:

The Columbus hospital that collects $6.76 billion a year and answers to no merger regulator

The word in the statute that decides who gets reviewed and who walks free

What “state instrumentality” buys you that “nonprofit” does not

The blind spot every state with a flagship medical center shares

Glossary at the bottom of today’s article.

THE POWER MOST STATES DO NOT HAVE

Start with the part Ohio gets right.

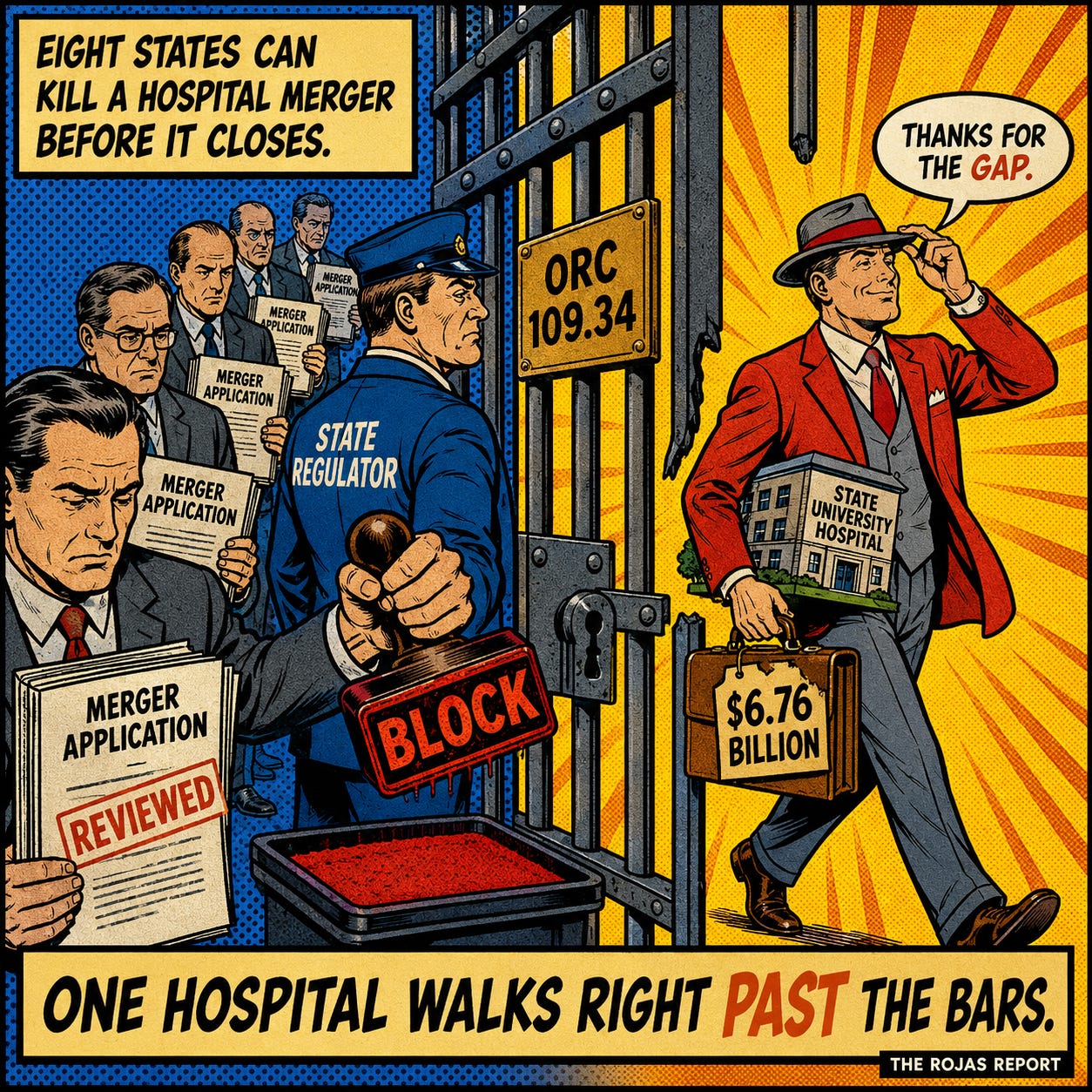

Ohio sits in a club of eight. Under Ohio Revised Code 109.34, a nonprofit health care entity that wants to sell, merge, or transfer control of at least 20 percent of its assets must do more than send a letter. It has to obtain the Attorney General’s written approval. The Attorney General can approve. The Attorney General can block. If the deal gets disapproved, it does not close.

Take another gander.

Not notify.

Not comment.

Approve, or kill.

Forty-two states cannot do this. Most require a courtesy notice, and the Attorney General gets to write a strongly worded opinion while the merger closes anyway. Eight states hold the real lever: California, Massachusetts, Ohio, Connecticut, New Jersey, Oregon, Rhode Island, and Wisconsin. Ohio is on the short list of attorneys general who can stand at the courthouse door and say no.

And they use it. In June 2025, Attorney General Dave Yost conditionally approved the $485 million sale of Summa Health to a General Catalyst subsidiary, converting a nonprofit system to for-profit.

The deal closed later that year. In February 2026, the same office joined the Department of Justice to sue OhioHealth for forcing insurers into contracts that block cheaper health plans. The power is live. The office is awake.

So Ohio armed its regulator. The question nobody in Columbus asks out loud is who that regulator was armed to point at.

THE WORD THAT DECIDES WHO GETS REVIEWED

Here is the one word.

Section 109.34 reaches a “nonprofit health care entity.” The statute defines it narrowly: a hospital owned by a corporation organized under Chapter 1702 of Ohio’s nonprofit corporation law, or an entity exempt under Section 501(a) of the federal tax code. That is the cage. It was built for the private 501(c)(3). It was built for Summa. It was built for OhioHealth.

It was not built for the state.

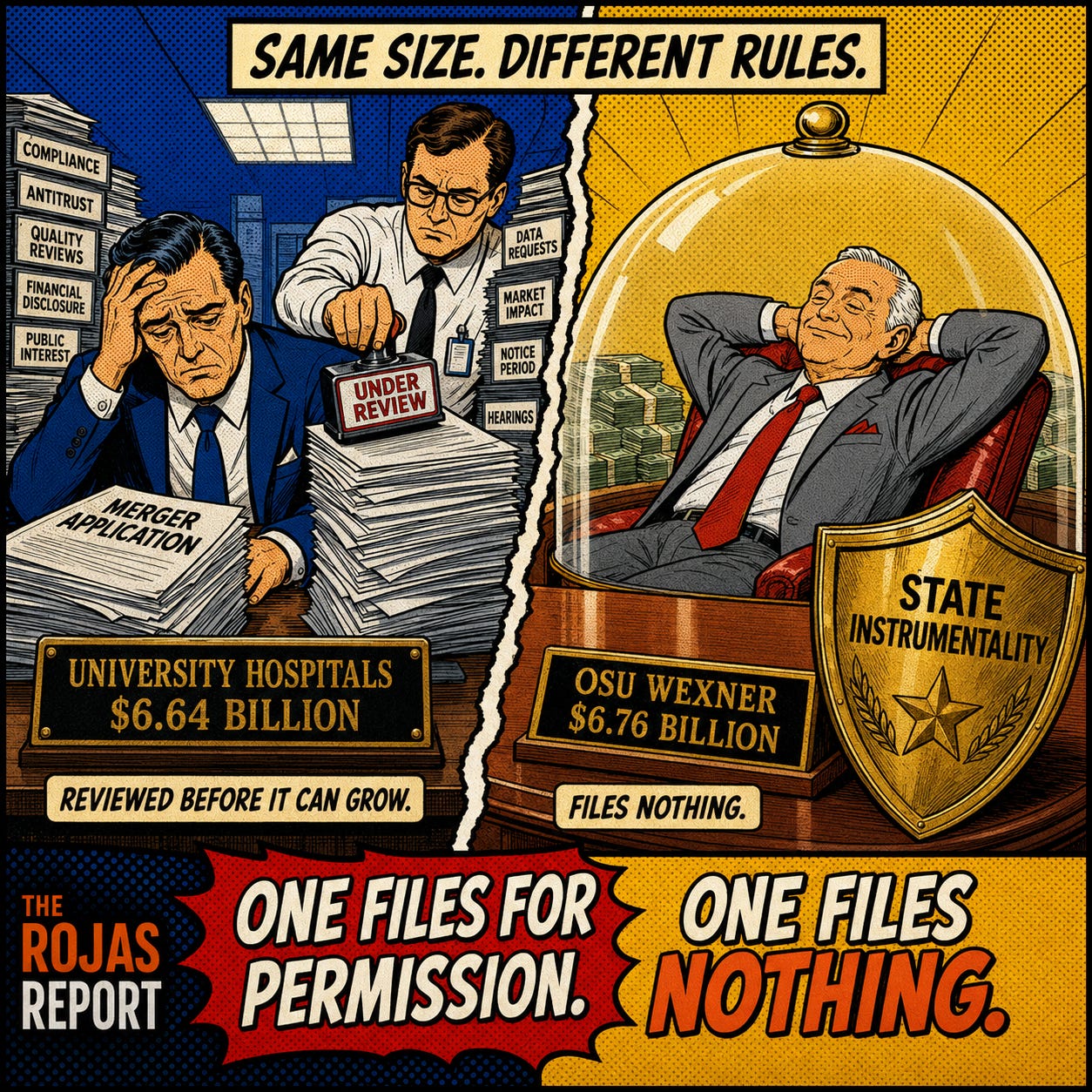

The Ohio State University Wexner Medical Center is not a private nonprofit corporation. It is the medical center of a public university. A state instrumentality. A special purpose government entity.

It is exempt from federal income tax and local property tax not because it filed for charitable status, but because it is an arm of the State of Ohio.

That distinction sounds like paperwork.

It is the whole story.

A private nonprofit gets its tax exemption from the IRS and its merger oversight from the Attorney General’s charitable trust authority.

A state university hospital gets its exemption from being the government.

The 2025 audit says it plainly: the medical center is exempt from federal and state income tax as an integral part of the State of Ohio. Not as a charity. As the state.

So OSU’s acquisitions do not trigger the charitable-trust merger review under Section 109.34. The statute’s own definitions exclude the state’s hospital. The biggest hospital in central Ohio sits in the one gap the statute leaves, by design of the definition, not by anyone’s oversight.

THE HOSPITAL THE STATUTE WAS NEVER WRITTEN TO REACH

Look at the size of what is standing in the gap.

OSU Wexner posted record revenue of $5.99 billion in fiscal 2024. By fiscal 2025, total revenue reached $6.76 billion. That puts it in the same weight class as the systems the Attorney General does review. University Hospitals, a private system within the statute’s reach, collects $6.64 billion. OSU collects more. OSU files less.

And it has been growing. East Hospital. The Harding psychiatric hospital merger. Outpatient centers and joint ventures across the region. A $3 billion new inpatient tower under construction.

Every private system that grew that way in Ohio left a paper trail at the Attorney General’s office. The state’s own system grew alongside them, in the same market, competing for the same patients, under a different set of rules.

This is the blind spot.

Not a scandal of a signature given.

A scandal of a signature never required.

The deals get reviewed before they close, unless the buyer is the state.

Every private hospital in Ohio files for permission to grow.

The biggest one files nothing.

You can keep finding that out after the deal closes, or you can read it here first.

WHAT ZERO TAX BUYS

Tax exemption is not a discount.

It is a head start that compounds every year.

OSU Wexner pays no federal income tax on $6.76 billion in revenue. It pays no property tax on a real estate footprint that, across Columbus nonprofit hospitals, the Lown Institute values at $992 million.

The statewide property tax exemption for Ohio nonprofit hospitals runs $419 million a year. The total annual tax break for the state’s nonprofit hospitals comes to $2.2 billion.

A physician-owned hospital across the street pays all of it. Income tax. Property tax. The full freight. Then it competes against an entity that pays none, files no merger paperwork, and carries the implicit credit of the State of Ohio behind its bonds.

There is no market in Ohio, only regulatory capture.

THE REGULATOR POINTED EVERYWHERE BUT HOME

The standard defense is that the IRS watches nonprofit hospitals. It does not, in any way that matters. The IRS has revoked a hospital’s tax exemption exactly once, in 2017, and the Government Accountability Office has spent years documenting that the agency has no real process to check whether these hospitals earn their exemptions.

The federal regulator is asleep.

That is why the Attorney General matters. Across the country, state attorneys general are the regulators with real teeth when it comes to nonprofit hospital behavior. Ohio’s has more teeth than most. The office can block a merger. It is suing OhioHealth right now. Vivek Ramaswamy is running for governor on a promise to make Medicaid fraud prosecution a top statewide priority, working through that same office.

So the tools exist.

The will exists.

The lever is in the room.

It has simply never been pointed at the state’s own $6.76 billion hospital, because the statute that built the lever was written to reach private nonprofits, and the state quietly stands outside its own reach.

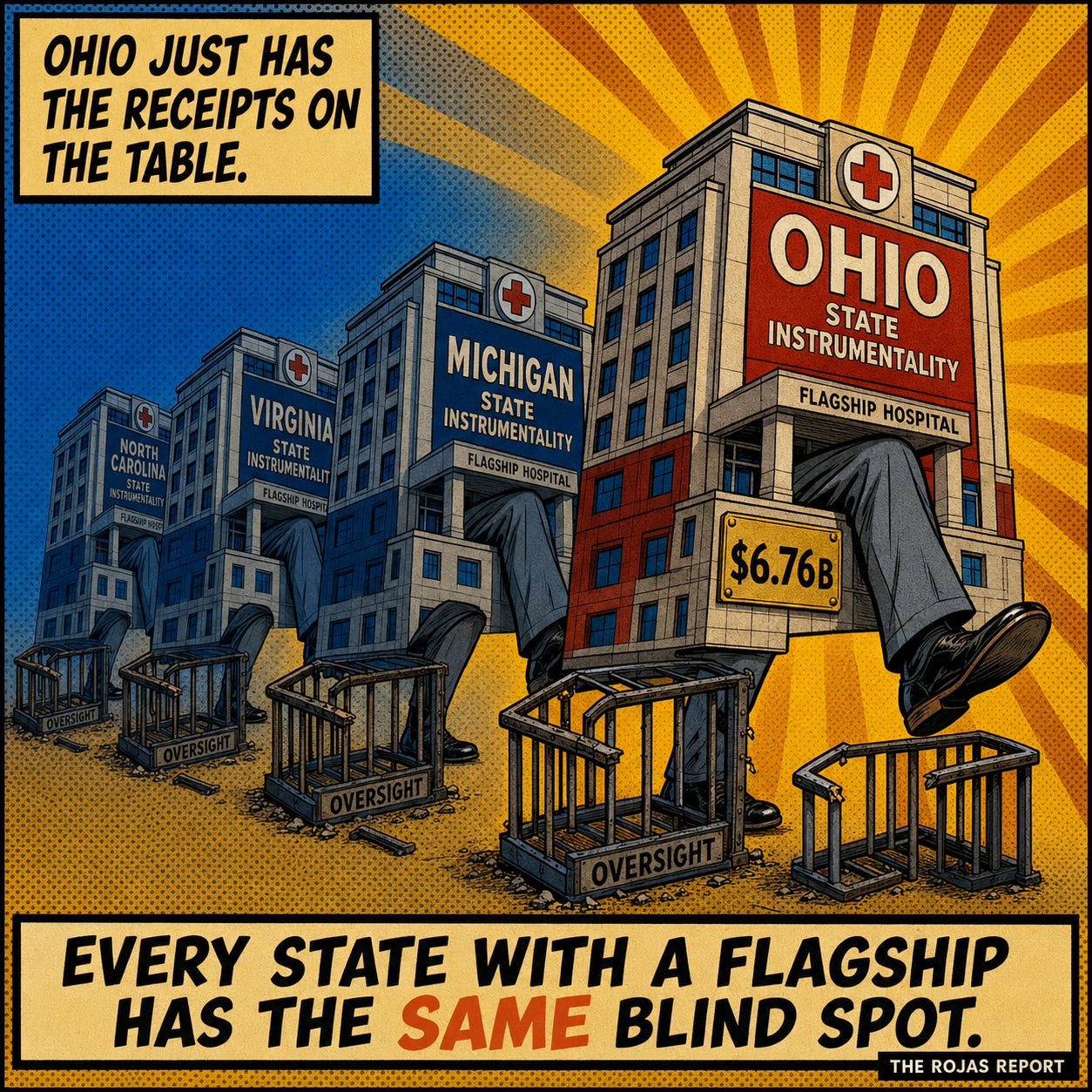

THIS IS NOT AN OHIO STORY

Here is the part worth sitting with.

Ohio did not make a mistake unique to Ohio. It built a regulator to catch private nonprofit consolidation and left its public flagship outside the statute.

Michigan Medicine is a state instrumentality.

UVA Health is a state instrumentality.

UNC Health is a state instrumentality.

Every state with a flagship academic medical center built the same structure: a hospital that grows like a private system, collects like a private system, and answers to the merger regulator like a government, which is to say, it does not.

Ohio just happens to have the receipts on the table and an Attorney General with the power to read them.

The cage works.

It catches the private systems.

The largest one in the state walks past it every year, because the law that built the bars was never written to hold the state.

That is the blind spot. Over the next pieces in this series, we follow a single dollar through the system that sits inside it. Where it comes in. Where it gets harvested. Where it goes. And who is on the hook when it breaks.

-Rojas out.

GLOSSARY

ORC 109.34: Ohio’s hospital merger statute. It requires a nonprofit health care entity to get the Attorney General’s written approval before selling, merging, or transferring at least 20 percent of its assets. The Attorney General can block the deal outright.

Nonprofit health care entity: As the statute defines it, a hospital owned by a corporation organized under Ohio’s nonprofit corporation law (Chapter 1702) or exempt under Section 501(a) of the federal tax code. A private charity, not a government body.

State instrumentality: An arm of state government. A public university and its medical center fall in this category. It is tax-exempt because it is the government, not because it holds a charitable IRS designation.

Pre-approval authority: The power held by eight state attorneys general to block a nonprofit hospital merger before it closes, rather than only comment on it after the fact.

Section 6001: The federal Affordable Care Act provision that banned new physician-owned hospitals and froze growth at existing ones. It is why the state hospital faces no physician-owned competitor of comparable scale.

SOURCES

Ohio Revised Code, Section 109.34, “Notice of transactions by nonprofit health care entity”

The Ohio State University Wexner Medical Center, “Facts and Figures” (FY2025 total revenue, $6.76B)

Columbus Business First, “OSU Wexner Medical Center posts record revenue in FY24” ($5.99B)

Ohio Auditor of State, OSU Wexner Medical Center Health System Financial Statements (FY2025) (tax status, “integral part of the State of Ohio”)

Lown Institute, 2024 Hospital Fair Share Spending Report, Ohio State Report ($2.2B total tax breaks; $419M property; $992M Columbus property value)

Chief Healthcare Executive, “General Catalyst firm to close $485M purchase of Ohio hospital system” (Summa, AG approval)

Healthcare Dive, “IRS revokes hospital nonprofit status for the first time” (2017)

Vivek for Ohio, “Plan to Crush Medicaid Waste, Fraud and Abuse”